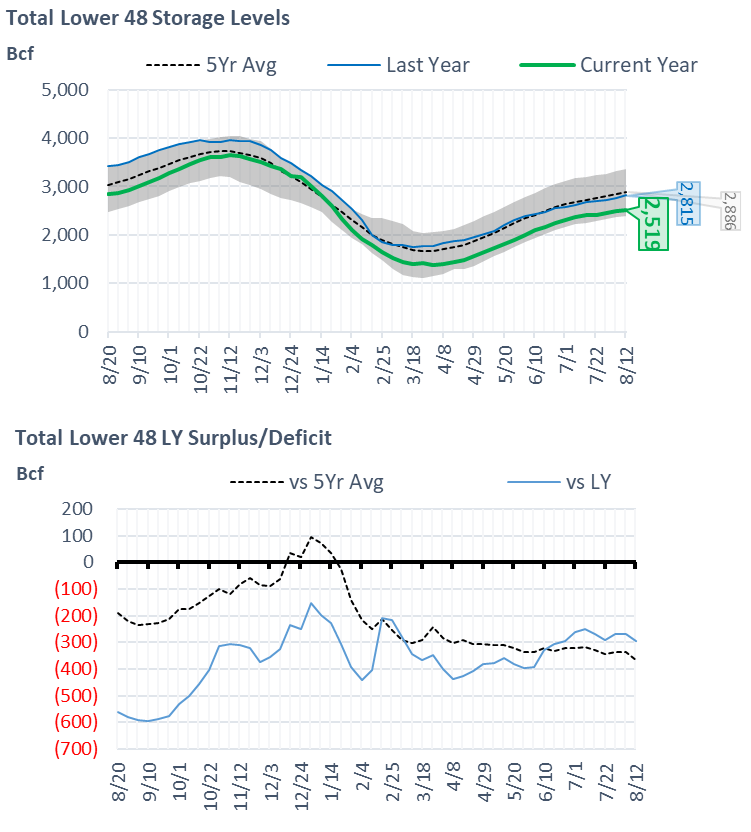

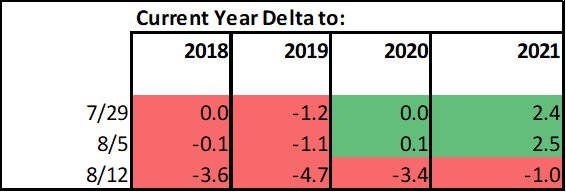

The EIA reported a +18 Bcf injection for the week ending Aug 12th, which came as a complete surprise to the market. 95% of estimates were atleast over +20 Bcf; hence this one is tough to explain. This storage report takes the total level to 2519 Bcf, which is 296 Bcf less than last year at this time and 367 Bcf below the five-year average of 2,794 Bcf.

Here are the few factors that help us understand the push behind the low weekly injection:

1) +0.8F more CDDs on average over the week leading to 1.3 Bcf/d of strong burns

2) lower Canadian imports with FM/maintenance on the Northern Borders pipeline, T-South, and GTN

3) weak wind levels average 32 aGWh over the week

So after back-to-back loose number, this once again sends us back to confusion land. We calculate the +18 Bcf injection being -1.0 Bcf/d loose vs LY’s rolling 5-week period (wx adjusted). See the weekend report on Sunday for details behind this calculation.

For this reporting period, the wind came in much below expected levels for this time of the year and at this level of installed capacity. For week ending Aug 12th, wind generators produced 32.7 GWh of power and we should have expected 35-36 GWh according to our math; hence the partial reason for this week’s tight number was the low wind generation. The change in wind week on week, added approximately 0.9 Bcf/d of additional power burns on average.

Today’s Fundamentals

Daily US natural gas production is estimated to be 98.8 Bcf/d this morning. Today’s estimated production is +0.36 Bcf/d to yesterday, and +0.54 Bcf/d to the 7D average. The completion of maintenance in the SC is helping boost production to record levels in that region. Meanwhile, Northeast production remains weak.

Natural gas consumption is modelled to be 78.8 Bcf today, -0.28 Bcf/d to yesterday, and +1.9 Bcf/d to the 7D average. US power burns are expected to be 40.2 Bcf today, and US ResComm usage is expected to be 8.1 Bcf.

Net LNG deliveries are expected to be 11.2 Bcf today.

Mexican exports are expected to be 7 Bcf today, and net Canadian imports are expected to be 5.5 Bcf today.

The storage outlook for the upcoming report is +58 Bcf today.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.