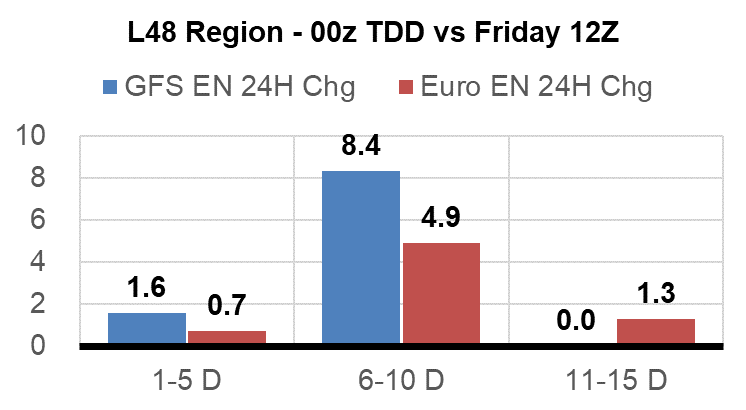

This long weekend runs warmed significantly compared to Friday, especially in the 6-10 day period. The Midwest and Northeast regions warmed the most for those timeframes leading to a big shift in overall power demand estimates. This translated into prices opening up on Sunday much higher that Friday. The gain over the weekend more than made up the big drop seen after the storage report on Thursday.

Today’s Fundamentals

Daily US natural gas production is estimated to be 89.6 Bcf/d this morning. Today’s estimated production is -1.74 Bcf/d to yesterday, and -1.94 Bcf/d to the 7D average. We typically see a big drop on the 1st of the month. The nomination data is usually revised a few days into the month.

Natural gas consumption is modelled to be 61.7 Bcf today, +0.67 Bcf/d to yesterday, and -4.24 Bcf/d to the 7D average. US power burns are expected to be 29.64 Bcf today, and US ResComm usage is expected to be 8.7 Bcf.

Net LNG deliveries are expected to be 11.1 Bcf today.

Mexican exports are expected to be 6.9 Bcf today, and net Canadian imports are expected to be 3.5 Bcf today.

The storage outlook for the upcoming report is +101 Bcf today.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.