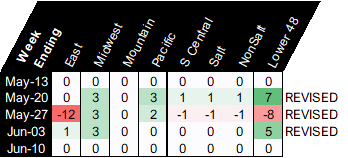

The EIA reported a +92 Bcf injection for the week ending June 10th, which came in slightly higher than the market consensus. Yesterday’s report included some of the impact from the Freeport outage and also came with a number of revision for the previous three week – May 20th, May 27th, and June 3rd. Here is a table the summarizes the weekly changes.

With the latest revision, we get a triple-digit injection this quarter with the help of the long weekend demand dip and exceptional wind. All the revisions make sense to us except the for the big hit to the East storage region for week ending May 27th. This one data point doesn’t line up with what the pipeline scrape data shows. The scrape data shows >30 Bcf injection for the East, while the revised data now shows only 20 Bcf. This makes us believe there was some technical reassessment done to a storage field.

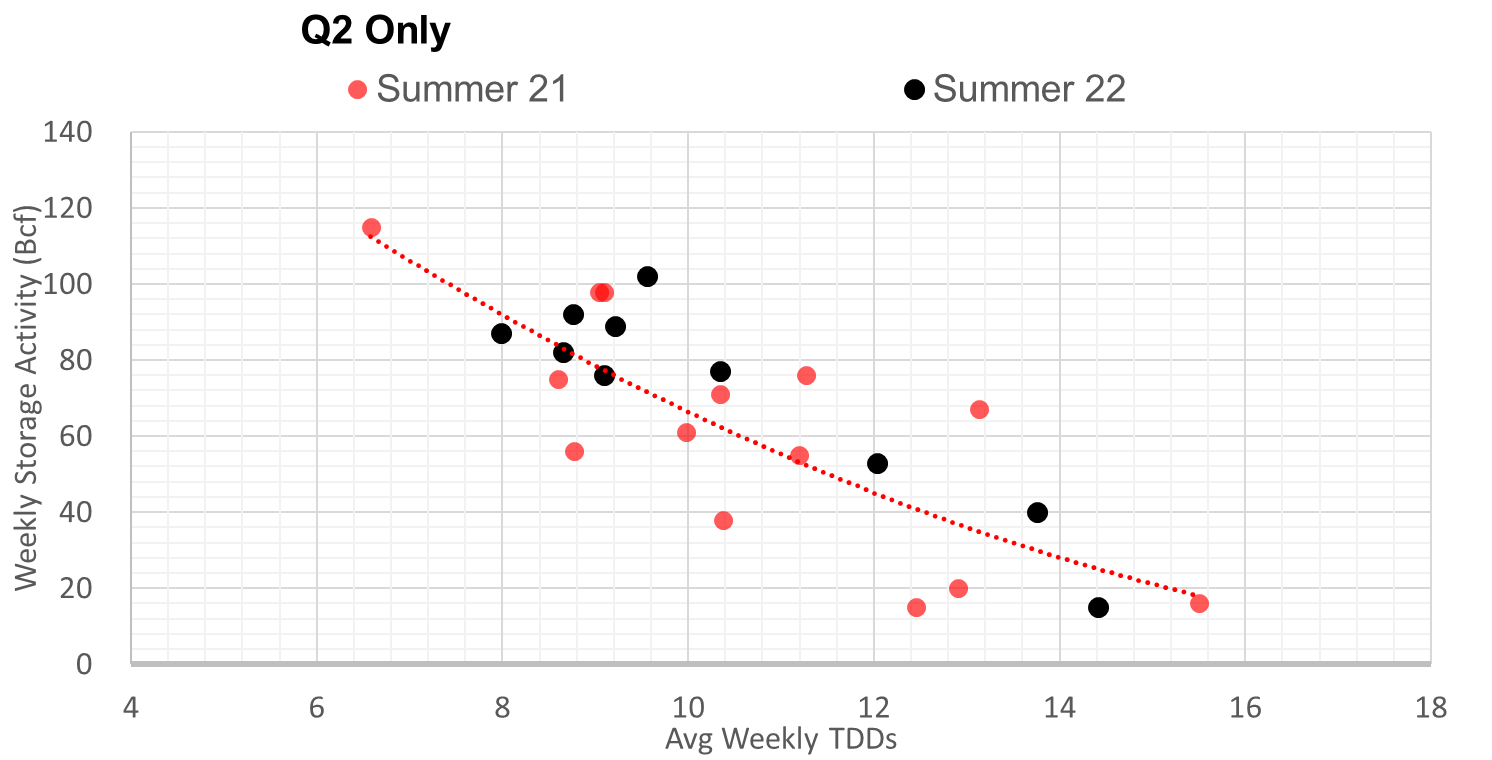

This storage report takes the total level to 2095 Bcf, which is 330 Bcf less than last year at this time and 323 Bcf below the five-year average of 2,418 Bcf. Overall, we estimate this +92 Bcf injection is ~1.9 Bcf/d loose vs last summer (wx adjusted). If we were to focus solely on the injection and weather relationship in Q2 2021 then this number was 1.5 Bcf/d looser (wx adjusted). See the chart below.

Today’s Fundamentals

Daily US natural gas production is estimated to be 95.6 Bcf/d this morning. Today’s estimated production is -0.66 Bcf/d to yesterday, and -0.46 Bcf/d to the 7D average.

Natural gas consumption is modelled to be 45.5 Bcf today, -34.61 Bcf/d to yesterday, and -31.81 Bcf/d to the 7D average. US power burns are expected to be 40.3 Bcf today, and US ResComm usage is expected to be 0 Bcf.

Net LNG deliveries are expected to be 11 Bcf today.

Mexican exports are expected to be 6.9 Bcf today, and net Canadian imports are expected to be 5.8 Bcf today.

The storage outlook for the upcoming report is +59 Bcf today.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.