PDF Attached

USDA

released their January reports and unlike other years, there were no major fireworks. Positioning commenced post USDA report with selling in wheat and buying in soybeans, which left corn stick in the middle.

Over

the next several business days we will be updating tables and graphs. The evening comment highlights major changes, found after the text.

Private

exporters reported the following activity:

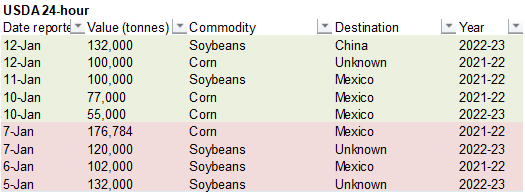

-132,000

metric tons of soybeans for delivery to China during the 2022/2023 marketing year

-100,000

metric tons of corn for delivery to unknown destinations during the 2021/2022 marketing year

US

CPI data confirmed rising inflation.

US

Dollar as of 12:45 pm CT

![]()

USDA

released their January reports

Reaction:

Bearish

grains and neutral soybean complex. Going forward we could see soybeans and corn prices trade sideways over the short term, and wheat medium term to appreciate led by HRW if US drought conditions across the central and southern Great Plains persist.

USDA

OCE Secretary’s Briefing

https://www.usda.gov/oce/commodity-markets/wasde/secretary-briefing

US

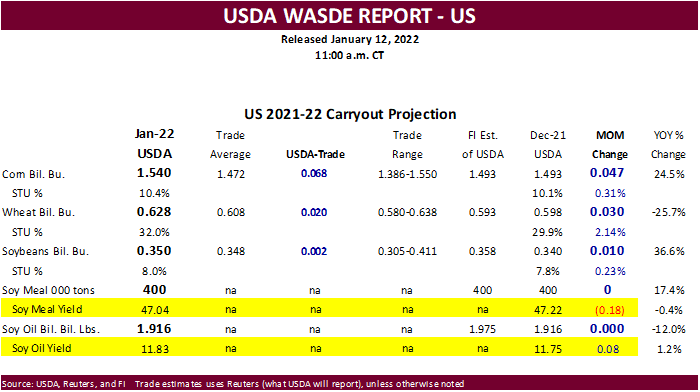

corn stocks as of December 1 were 11.647 billion bushels, in large part to an upward revision in corn production by 53 million bushels. Dec 1 stocks came in 45 million above trade expectations and perhaps the most bearish number found in these reports today,

for corn. Soybean stocks as of December 1 of 3.149 billion were 20 million above trade expectations, and all-wheat December 1 stocks were 31 million below trade expectations.

US

winter wheat seeds were only 142,000 acres above trade expectations at 34.397 million, 749,000 above 2021. HRW acres of 23.8 million were 234,000 below trade expectations, SRW of 7.07 million were a half million above the average trade guess and winter white

of 3.560 million near trade expectations. We see no major price reaction from the seedings report, although it does favor HRW over SRW type wheat.

There

was an aggressive move by USDA in response to the dryness in South America. Brazil soybean production was taken down 5 million tons and Argentina soybeans by 3 million. Paraguay soybeans were lowered 1.5 million tons. The combined 9.5 million ton decrease

to those three countries contributed to the 6.8-million-ton reduction for USDA’s 2021-22 world ending stocks. Global soybean production was lowered 9.2 million tons (US upward revised 0.3MMT). One of the largest upsets for this report was an unchanged US

soybean export projection. With export commitments running well more than 20 percent below last year’s level for this time of year, USDA left its 2.050 billion bushel estimate unchanged, which is down only 9.5 percent from 2020-21. The US crush was also left

unchanged at 2.190 billion bushels. With production upward revised 10 million bushels, the carryout increased 10 million to 350 million, up from 257 million year ago.

USDA

upward revised the US corn carryout by 47 million bushels to 1.540 billion, above 1.235 billion at the end of 2020-21. USDA upward revised their US corn production by 53 million to 15.115 billion after realizing a higher harvested area. Corn for ethanol was

taken up 75 million bushels to 5.325 billion, same as our estimate, and above 5.028 billion used last season. Exports were lowered 75 million bushels to 2.425 billion. World corn production was lowered 1.8 million tons to 1.207 billion, 7.5% above 2020-21.

Global ending stocks fell 2.5 million tons to 303.1 million. USDA lowered Argentina corn production by 0.5 million tons to 54.0 million tons and Brazil output by 3.0 million to 115 million. EU and Mexico corn production was lowered 400,000 tons each.

US

all-wheat ending stocks were upward revised 30 million bushels to 628 million, below 845 million year ago. Imports were lowered 10 million, feed taken down 25 million and exports were downward revised 15 million. World wheat production was lifted higher by

700,000 tons and global ending stocks are up 1.8 million tons from the previous month. USDA lifted Argentina wheat production by 0.5 million tons to 20.5 million, a record. EU wheat was taken up 200,000 tons to 138.9 million. There were no changes to Russia

or Ukraine production.

US

soybean meal and soybean oil product yields were revised from the previous month. Meal was lowered to 47.04 from 47.22 previous month and soybean oil taken up to a large 11.83 pounds per bushel from 11.75, needed and wanted as biofuel expansion will demand

more of the product second half 2022.

Weather

WEATHER

EVENTS AND FEATURES TO WATCH

- Argentina

planting as of last Thursday as reported by the Ag Minister - Cotton

95% - Corn

84% - Peanuts

99% - Soybeans

93% - Sorghum

68% - Wheat

and barley harvesting were 99% done - Argentina’s

early season corn and sunseed are reproducing - Argentina

temperatures Tuesday afternoon reached 100-110 degrees Fahrenheit (38-41C) - No

rain fell and soil moisture was depleted from the topsoil and very limited in the subsoil

- Crop

stress was serious in most of the nation - No

changes in Argentina’s general outlook have occurred overnight - Dry

and hot conditions will prevail through Saturday morning - Daily

high temperatures of 100 to110 will occur daily with extremes of 110 to 115

- Most

of the nation will receive rain from late Saturday of this week into Sunday, January 23, although rain does not fall in all areas every days - Amounts

will be sufficient for notable relief from this week’s extreme conditions - Rain

totals in some northeastern crop areas will vary from 2.00 to 4.00 inches and locally to 6.00 inches

- Central

and Southwestern Argentina rainfall will vary from 0.75 to 2.00 inches with some potential for locally more

- Weak

ridge building suggested by GFS model for Jan. 23-24 does not last and breaks down Jan. 25-27 - European

and GFS Ensemble forecast models suggest zonal flow pattern aloft across Argentina Jan. 23-27, but higher heights than usual suggesting some rain and warm temperatures - World

Weather, Inc. does not see weather in Argentina as harsh as this week again for an extended period of time, although a ridge of high pressure is expected again in either late January or early February - Argentina’s

bottom line will remain extremely stressful through Saturday for all crops. Some recently planted grain and oilseed crops may have to be replanted or will be lost because of too much dryness and recent heat. Other crops with favorable root systems have a good

chance of recovering from this week’s stress if rain falls as significantly and generally as advertised during the late weekend and next week. Cooler temperatures Sunday through the end of next week will be a huge boon to the nation’s crops reducing stress

for all areas – even those that have to wait longer for significant rain to fall. Follow up rain will be critically important and a close watch on the situation is warranted. Some late season planting and replanting will occur immediately after rain falls

next week. - Brazil

weather already improved in the North Tuesday and early today with lighter rainfall in the water-logged areas of the north - Brazil

weather is expected to be much improved for Mato Grosso, Tocantins, Bahia, Minas Gerais and Goias over the next two weeks with net drying for many areas initially and then a good mix of showers and sunshine in the second week of the forecast - Southern

Brazil rainfall will continue lighter than usual over the next ten days and possibly for two weeks, but there will be some periodic shower activity - Crop

conditions should stay mostly good, but there will be some concern about less than usual precipitation as time moves along - Southern

Rio Grande do Sul will get rain briefly next week that will improve topsoil moisture for rice and corn

- Northern

Rio Grande do Sul and areas north and west into Parana, Paraguay and Mato Grosso do Sul will likely see a more erratic and light rainfall pattern that might eventually return the need for greater rain - Brazil

temperatures are expected to be near to slight above normal this weekend and all of next week - Much

of Paraguay is unlikely to see “significant” relief to its dry bias - The

bottom line for Brazil is mostly good for its crops, although there will be some watchful eyes on interior southern parts of the nation where the ground may dry out more significantly during the coming ten days in response to some ridge building limiting rainfall

and keeping temperatures a little warm biased. Similar conditions farther north in Brazil will translate into a much improved early soybean and corn maturation and harvest environment. Safrinha corn and cotton planting should occur quickly as soybean harvesting

advances. Rainfall should resume in center west, center south and northeastern Brazil after Jan. 20, but it will not be nearly as great as it has been. - U.S.

weather is expected to continue dry biased in the Great Plains and much of the western states during the next ten days with less rain in the interior Pacific Northwest as well - California

weather will include some showers to the far north periodically, but most of the precipitation will be lighter than usual - A

succession of cool air masses will impact the central and eastern parts of North America beginning this weekend and continuing through the following weekend bringing down average temperatures - A

cooler than usual bias will return to the northern Plains and upper Midwest - Precipitation

may be more limited in the eastern U.S. for a few days and the break will be welcome - Another

storm is expected late this weekend into early next week followed by some lighter and more infrequent precipitation for a while - A

snow event expected from North Dakota to Missouri and parts of Illinois, Kentucky and Indiana late Thursday into Saturday will leave behind a swath of significant snowfall - Accumulations

of 2 to 6 inches and local totals to 10 inches or more will be possible - A

nor’easter of sorts is expected to impact the Atlantic Coast states this Sunday and Monday, but the system is advertised warmer today and farther to the northwest reducing snow potentials along the coast, but increasing it in interior parts of the northeastern

states and in the lower and eastern Midwest - Some

areas in the lower and eastern Midwest into New York, New England and southeastern Canada may get 6 to 14 inches of snow - New

South Wales, Australia will receive periodic showers and thunderstorms this week into early next week supporting cotton, sorghum and other summer crops - Rainfall

of 0.25 to 1.00 and a few 1.00 to 2.00-inch amounts are expected - Queensland,

Australia is unlikely to get much “meaningful” moisture this week, although a few showers will evolve - Greater

rain is needed for dryland production areas - Queensland

rainfall may begin to increase in the middle to latter part of next week while rain continues in New South Wales - The

moisture boost will be a boon to summer crops - Australia

temperatures will be warmer than usual in western Queensland, western New South Wales and neighboring areas where rainfall may not be as great as needed to protect livestock grazing areas from further deterioration. - Rain

is needed on these areas - Australia’s

bottom line is one of needed rain in Queensland’s unirrigated grain, oilseed and cotton areas as well as all of eastern Australia’s livestock country, but especially in the west. No serious changes to dryness in western parts of Queensland or New South Wales

will occur in the coming week, but some relief is expected in the January 20-26 period.

- South

Africa rainfall will be well distributed during the next two weeks with all crop areas impacted at one time or another - Yield

potentials remain high and “some” of the worry over wet weather diseases has been reduced with less rainfall recently - India

weather the remainder of this week will support more rain in east-central and southeastern parts of the nation expanding the area benefiting from recent significant moisture - The

precipitation will be greatest from southeastern Madhya Pradesh through Chhattisgarh into Odisha and northeastern Andhra Pradesh where rainfall will range from 0.75 inch to 2.00 inches with local totals over 3.00 inches

- Net

drying is expected elsewhere, but especially in the western half of the nation - Canada’s

Prairies will be warmer than usual over the coming week and then a little colder especially in the east

- Canada’s

southwestern Prairies are still drier than usual with moisture totals less than 0.25 inch over the next two weeks

- Snow

cover is still limited in east-central and southern Alberta and central, west-central and southwestern parts of Canada’s Prairies - This

is the most seriously drought stricken part of the Prairies and not much relief is likely prior to spring - Europe

precipitation during the next two weeks will be restricted especially in the western half to two-thirds of the continent in this first week of the outlook - Spain

and perhaps a part of Romania are the only areas that would benefit greatly from more significant precipitation, but restricted amounts are expected for a while - Soil

moisture is likely to be favorable across the continent during the next two weeks, despite limited precipitation - There

will be no threatening cold weather - Western

Russia, Belarus, Ukraine and Baltic States will get light and sporadic precipitation during the coming week with a boost in snow and a little rain next week - There

will be no threatening cold temperatures, but cooling is expected next week and the snow will be sufficient protection for the coldest areas to protect wheat - North

Africa precipitation will be limited during the next ten days with only a few showers likely in northeastern Algeria and Tunisia

- Southwestern

Morocco continues to be in a notable multi-year drought while dryness is also a concern in northwestern Algeria - Crops

elsewhere are doing relatively well - China’s

weather will continue mostly uneventful for a while, although periods of rain and a little snow will impact the Yangtze River Basin and interior southeastern provinces during the next couple of weeks.

- The

moisture will preserve the integrity of the 2022 rapeseed and southern wheat crops - Snow

will fall periodically in the far northeast while the Yellow River Basin and southern coastal provinces receive little to no precipitation - The

southern coastal provinces will eventually become too dry and this may lead to some concern about early rice planting in March, but there is plenty of time for change - Temperatures

will be near to slightly warmer than usual - Southeast

Asia oil palm, citrus, sugarcane, coffee, cocoa, rice and other crop areas of Indonesia, Malaysia and Philippines will receive frequent bouts of rain over the next two weeks - Some

heavy rain is possible, but no serious widespread flood problem is expected - Local

flooding will be possible, though - Eastern

Malaysia and southern Philippines will be wettest in the next ten days - Mainland

areas of Southeast Asia will be mostly dry during the next ten days except Vietnam coastal areas where some moderate rain will be possible late this week and into the weekend - Northernmost

Laos and northern Vietnam coffee, rice and other crop areas will get some rain late this week and especially Saturday through Monday, Jan. 17. - West-central

Africa precipitation will be limited to coastal areas and temperatures will be a little warmer than usual - East-central

Africa will be erratic, but it is expected daily through the next ten days supporting coffee, cocoa, rice sugarcane and other crops - Greater

rain is expected in Uganda and southwestern Kenya over the next ten days and the change will be welcome - Middle

East precipitation has been increasing with improved soil moisture likely over the next ten days - Some

beneficial moisture has already occurred in Pakistan, Afghanistan, Iraq and Iran - Winter

crops will benefit from whatever rain falls, but it is not expected to be evenly distributed for a while - Mexico

weather will trend wetter in southern parts of the nation for a little while this week

- Most

other areas will be dry for the next week - Northern

Mexico “may” get some rain after January 20. - Central

America precipitation will be greatest along the Caribbean Coast , but including a fair amount of Panama and Costa Rica during the next ten days - A

few showers will occur in Guatemala periodically as well, although rainfall will be light - Western

Colombia and western Venezuela precipitation is expected to occur periodically in coffee, corn, rice and sugarcane production areas during the next ten days, but no excessive rain is expected - Interior

Colombia and many areas in Venezuela have received less than usual precipitation in the past 30 days, but the greatest dryness may be outside of key crop areas - Today’s

Southern Oscillation Index was +6.01 and it was expected to continue falling for a while this week. The index peaked at +13.07 December 31. - New

Zealand rainfall is expected to continue getting less than usual precipitation this week with temperatures near to above normal

- Some

forecast models have suggested Tropical Cyclone Cody may come close enough to eastern parts of North Island to produce some heavy rainfall this weekend, but confidence is low.

Source:

World Weather, inc.

Wednesday,

Jan. 12:

- China

farm ministry’s CASDE outlook report - USDA’s

monthly World Agricultural Supply and Demand Estimates (WASDE) report, noon - USDA’s

NASS 2021 summary of crop acreages and yields, noon - USDA’s

quarterly stockpiles data for commodities, including wheat, barley, corn, soybeans and sorghum, noon - EIA

weekly U.S. ethanol inventories, production - USDA’s

Farm Service Agency issues 2021 crop size data gathered from producers, 1pm - New

Zealand Commodity Price

Thursday,

Jan. 13:

- USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - Suedzucker

quarterly earnings - Agrana

nine- month earnings - International

Grains Council monthly report - Port

of Rouen data on French grain exports

Friday,

Jan. 14:

- China’s

December trade data - ICE

Futures Europe weekly commitments of traders report, ~1:30pm - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

Macros

78

Counterparties Take $1.537 Tln At Fed Reverse Repo Op. (prev $1.527 Tln, 77 Bids)

US

CPI (M/M) Dec: 0.5% (est 0.4%; prev 0.8%)

–

CPI (Y/Y) Dec: 7.0% (est 7.0%; prev 6.8%)

–

US Core CPI (M/M) Dec: 0.6% (est 0.5%; prev 0.8%)

–

Core CPI (Y/Y) Dec: 5.5% (est 0.5%; prev 0.8%)

US

Avg. Real Weekly Earnings (Y/Y) Dec: -2.3% (prev -1.9%)

–

Real Avg. Hourly Earnings (Y/Y) Dec: -2.4% (prev -1.9%)

US

MBA Mortgage Applications Jan 7 1.4% (prev -5.6%)

–

30-Year Mortgage Rate Jan 7 3.52% (prev 3.33%)

U.S.

Crude Stocks Fell To Lowest Since Oct 2018 Last Week – EIA

US

DoE Crude Oil Inventories (W/W) 07-Jan: -4553K (est -1850K; prev -2144K)

–

Distillate Inventories: +2537K (est +1700K; prev +4418K)

–

Cushing OK Crude Inventories: -2468K (prev +2577K)

–

Gasoline Inventories: +7961K (est +2750K; prev +10128K)

–

Refinery Utilization: -1.40% (est -0.10%; prev 0.10%)

·

CBOT corn traded two-sided, ending lower in the front three months and slightly higher in the back months. Higher soybeans limited losses after USDA reported the US carryout 47 million bushels above December and 62 million above

an average trade guess. The January reports were not that eventful. Inflation, sharply lower USD, SA weather and slowing US industrial demand was on traders minds today.

·

US CPI confirmed rising inflation. “U.S. inflation hit 7%, highest in 40 years. Food at home index rose 6.5 percent over the last 12 months and this compares to a 1.5-percent annual increase over the last 10 years. The index for

food away from home rose 6.0 percent over the last year, the largest increase since January 1982,” noted one trader.

·

Funds sold an estimated net 3,000 corn contracts.

·

US ethanol production and stocks were well off expectations and bearish for US corn industrial demand. Yet production to date suggests corn use is on track to reach USDA’s projection that was upward revised 75 million bushels

today.

·

US Crude Oil Futures Settle At $82.64/Bbl, Up $1.42 Or 1.75%

·

USD was 71 points lower as of 1:54 pm CT and WTI crude up $1.22.

·

US natural gas surged today and that brought back the US acreage debate over rising fertilizer costs. It’s too early to tell is some corn acres will be trimmed from current private estimates but something to monitor. The November

2022 soybean / December 2022 corn ratio is sitting near 2.33

·

In its monthly CASDE update, China lowered 2021-22 corn consumption by 3 million tons to 287.7 million tons, above 282.16 million tons for the 2020-21 season. Industrial was down 2 million tons to 80MMT and feed was cut 1 million

to 286 million. China noted weak hog margins curbing demand. China left its 2021-22 soybean balance unchanged with imports standing at 102 million tons, up from 99.78 million in 2020-21.

·

Bulgaria reported a bird flu outbreak at a duck farm in the southern village of Zalti Bryag.

·

The weekly USDA Broiler Report showed eggs set in the US up 1 percent from a year ago and chicks placed down 2 percent.

·

(Reuters) – U.S. renewable fuel credit prices fell nearly 6% on Wednesday after a Reuters report said the Biden administration is considering lowering the 2022 ethanol blending mandate below the proposed 15 billion gallons, citing

sources. Renewable fuel (D6) credits RIN-D6-US traded at $1.20 cents each on Wednesday, down from $1.27 each on Tuesday.

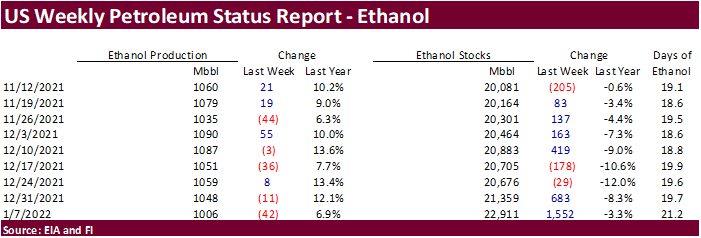

Weekly

US ethanol production

was reported at 1.006 million barrels, down 42,000 barrels from the previous week and well below expectations. Stocks ballooned 1.552 million barrels to 22.911 million. The trade was looking for stocks to increase 207,000 barrels.

U.S.

Crude Stocks Fell To Lowest Since Oct 2018 Last Week – EIA

US

DoE Crude Oil Inventories (W/W) 07-Jan: -4553K (est -1850K; prev -2144K)

–

Distillate Inventories: +2537K (est +1700K; prev +4418K)

–

Cushing OK Crude Inventories: -2468K (prev +2577K)

–

Gasoline Inventories: +7961K (est +2750K; prev +10128K)

–

Refinery Utilization: -1.40% (est -0.10%; prev 0.10%)

EIA

forecasts crude oil prices will fall in 2022 and 2023

https://www.eia.gov/todayinenergy/detail.php?id=50858&src=email

Export

developments.

·

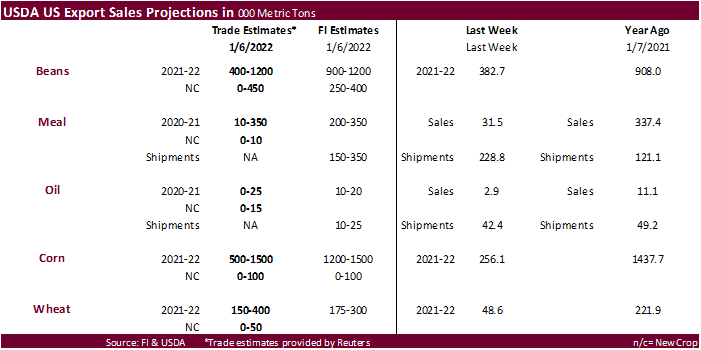

Under the USDA 24-hour reporting system, private exporters reported 100,000 tons of corn for delivery to unknown destinations during the 2021-22 marketing year.

Updated

1/10/22

March

corn is seen in a $5.70 to $6.20 range

·

Funds bought an estimated net 6,000 soybeans, bought 2,000 soybean meal, and bought 2,000 soybean oil.

·

Argentina producers sold 37.3MMT of 2020-21 soybeans through Jan 5, behind 38MMT year earlier.

·

USDA lowered Argentina soybean production to 46.5 million tons. Several private estimates are between 42 and 45 million tons, bias 42. Argentina corn is around 51-54 million tons (USDA is at 54.50 million.

·

Buenos Aires Grains Exchange warned of significant losses. They have yet to revise their crops. Last they were at 44MMY for soybeans and 57MMT for corn.

·

Abiove estimated the Brazil soybean production at 140 million tons, down 4.8 million form their previous estimate, and lowered export by 2.3 million tons to 91.1 million. They left crush unchanged at 48 million tons and sees the

carryout at 3.9 million tons. USDA is at 139MMT for production.

·

China left its 2021-22 soybean balance unchanged with imports standing at 102 million tons, up from 99.78 million in 2020-21.

·

India palm oil imports during December 2021 were 565,943 tons, down 27% from a year earlier (770,392 tons December 2020). This comes as India imported 392,471 tons of soybean oil, up 22% from year ago. Sunflower imports were

258,449 tons, up 10%. India generally buys most of its palm oil from Indonesia and Malaysia, soybean oil from Argentina and Brazil, and sunflower oil from Russia and Ukraine.

·

Winnipeg-based Mercantile Consulting Venture Inc. estimated Canada canola production in 2022 at 21 million tons, about 67 percent higher than 2021 of 12.6 million tons.

Export

Developments

·

Under the USDA 24-hour reporting system, private exporters reported 132,000 tons of soybeans for delivery to China during the 2022-23 marketing year.

·

The USDA seeks 7,540 tons of vegetable oil in 4-liter cans for Feb 16-Mar 15 shipment on January 19.

Updated

1/10/22

Soybeans

– March $13.00-$14.25

Soybean

meal – March $370-$435

Soybean

oil – March 54.50-61.00

·

US wheat ended lower after USDA reported winter wheat seedings higher than trade expectations and increased the global carryout by 1.8 million tons.

·

Funds sold an estimated net 9,000 SRW wheat contracts.

·

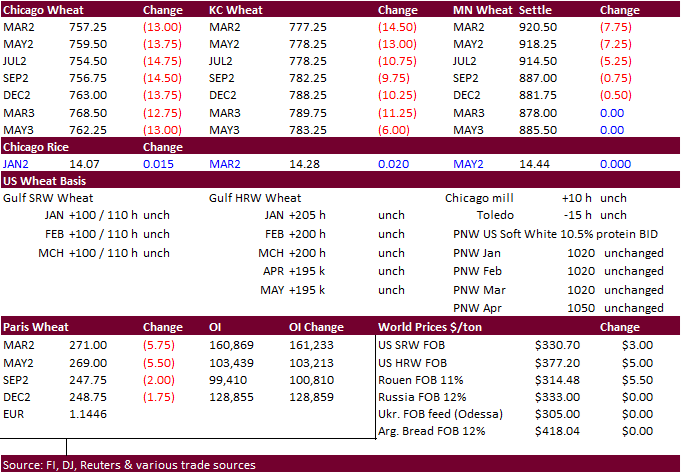

Paris March milling wheat settled down 5.50 euros, or 2.0%, at 271.25 euros ($310.26) a ton. It took out last Friday’s 2-1/2 month low of 270.25 euros, but found chart support around that level. Technically it looks short term

bullish.

·

FranceAgriMer lowered its forecast of French soft wheat exports outside the European Union for the 2021-22 season to 9.0 million tons from 9.2 million estimated in December. French soft wheat exports within the 27-member bloc

was estimated at 7.7 million tons from 7.8 million. French soft wheat stocks at the end of the 2021-22 was seen at 3.6 million tons from 3.5 million previous.

·

Ukraine plans to limit trade margins on a number of key food products in effort to slow inflation. December Ukraine inflation was up 13.3% from the same period year earlier.

·

The Russian government increased the export duty on wheat as of today, lasting until January 18, to $98.20 per ton from $94.90 per ton the previous period. The export duty on barley has risen to $86.20 per ton from $83.50 per

ton, and the export duty on corn has decreased to $67.70 per ton from $69 per ton.

·

Turkey seeks 345,000 tons of feed barley on Jan 20 for Feb 15-Jan 10 shipment.

·

Results awaited: China plans to sell 500,000 tons of wheat from state reserves on January 12 to flour millers.

·

Results awaited: Iran’s GTC seeks at least 60,000 tons of milling wheat for Feb-Mar shipment.

·

Iraq extended their deadline for 50,000 tons of wheat, set to now close on January 13 instead of the 3rd, from the US, Canada, and Australia.

·

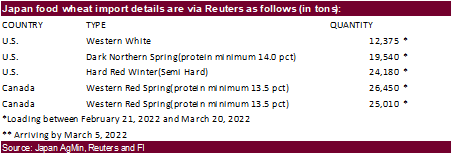

Japan in a SBS imported tender seeks 80,000 tons of feed wheat and 100,000 tons of feed barley on January 13 for arrival in Japan by March 17.

·

Algeria seeks milling wheat on January 13 for FH March shipment.

·

Japan seeks 107,555 tons of milling wheat this week.

·

Jordan seeks 120,000 tons of wheat on January 18. Possible shipment combinations are in 2022 between July 1-15, July 16-31, Aug. 1-15 and Aug. 16-31.

·

Turkey seeks 335,000 tons of milling wheat on January 18.

Rice/Other

·

(Bloomberg) — U.S. 2021-22 cotton ending stocks seen as 3.46m bales, slightly above USDA’s previous est., according to the avg in a Bloomberg survey of seven analysts. Estimates range from 3.0m to 3.85m bales. Global ending

stocks seen 125,000 bales lower at 85.61m bales.

·

Bangladesh seeks 50,000 tons of rice on January 16.

Updated

1/10/22

Chicago

March $7.20 to $8.40 range

KC

March $7.55 to $8.75 range

MN

March $8.75‐$10.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.