PDF Attached

Soybeans saw technical buying after holding key moving averages the last 24 hours. Wheat was higher on US and Germany helping arm Ukraine with armored vehicles. Corn ignored wheat and soybeans and fell on profit-taking after yesterday’s gains.

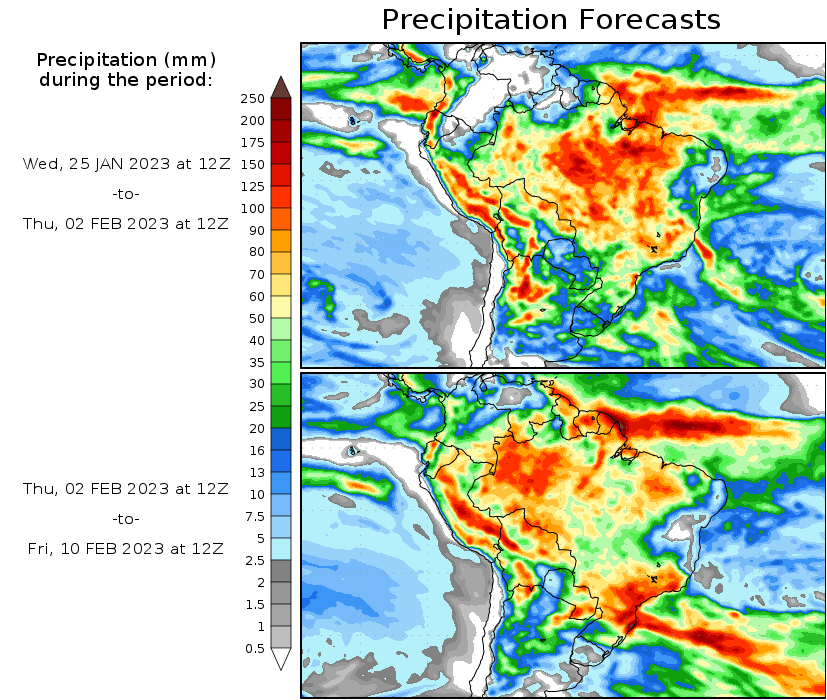

MOST IMPORTANT WEATHER FOR THE COMING WEEK

- Argentina rainfall Tuesday was most significant in northern Cordoba and in a few Santiago del Estero locations where some 0.50 to 1.50-inch amounts occurred

- Cordoba City, Cordoba reported 1.81 inches of rain

- Net drying occurred elsewhere in the nation

- Temperatures were very warm to hot again in northern Argentina

- Most of Argentina will get rain at one time or another in the next ten days, though the precipitation will be most frequent and significant in west-central and northwestern crop areas

- World Weather, Inc. is still expecting some net drying to occur for a while in February which makes some of the rain falling now all the more important

- Relief from drought is occurring, but the nation may not be done with challenging weather

- Conditions will not be as extreme as they have been though

- Brazil’s net drying in the south will be ongoing for the coming week and the impact will be mixed

- Early season soybean maturation and harvest progress should advance better in this environment and some increase in Safrinha corn and cotton planting will be possible as well

- Rain is expected to resume in the second week of the forecast and that should be in sufficient time to maintain a good outlook for immature crops

- As of today the only area in Brazil that has seen ongoing dryness issues is central and southern Rio Grande do Sul and that may continue for a while

- Center west and center south Brazil weather will continue wet enough to maintain some concern over the progress of soybean maturation and harvest rates

- Drier weather would be welcome for a while, but unlikely in the coming ten days

- Some areas of excessive moisture will prevail in Minas Gerais, northeastern Sao Paulo, Espirito Santo and a few areas in Goias and Tocantins

- Some harvest progress is expected and some Safrinha planting will occur as well, but a little less rain and a little less frequency would be best for a brief week or two

- Heavy rain and some severe thunderstorms occurred from areas near the upper Texas coast into the Delta Tuesday

- Rainfall varied from 1.00 to 2.50 inches in the Delta while areas in the northwest part of Houston, Texas reported 2.00 to more than 5.00 inches of rain and some damaging tornadoes and hail

- Rain and snow were widespread in the southern U.S. Plains Tuesday and from there into the lower and eastern Midwest and northern Delta

- Moisture totals varied up to 0.60 inch outside of the Delta and snow totals from Monday night through early this morning reached up to 10 inches in the southeastern Texas Panhandle

- West Texas cotton areas received several inches of snow and moisture totals varied up over 0.40 inch in a few northern areas

- Northwestern U.S. Plains, southern Alberta, Canada and southwestern Saskatchewan Canada continue snow free today, but will receive waves of snow in the next few days and by the end of the weekend snow cover will be sufficient to protect winter wheat from the bitter cold expected this weekend into next week

- Central U.S. temperatures and Canada’s Prairies as well as a part of the U.S. Pacific Northwest will turn bitterly cold this weekend through early next week

- The Pacific Northwest will trend warmer during the second half of next week

- Waves of bitter cold are likely in the northern and central Plains next week and through the first half of February

- Cold air in the eastern U.S. will be limited during the next couple of weeks, although the northeast is expecting some bitter cold briefly during the first weekend of February with warming shortly thereafter

- There is no risk of damaging cold in Europe or Asia during the next two weeks

- California precipitation will be restricted through Saturday and then a succession of weak weather systems will bring some light snow and rain to the state and nearby areas starting Sunday and going into the first week of February

- Snowfall and rain totals will be light, but still beneficial

- Canada’s Prairies will see waves of snowfall during the next two weeks, although moisture content in the snow is expected to be light

- Europe weather is expected to be tranquil during the coming week, but there may be a boost in precipitation during the second week of the forecast

- CIS weather is expected to be relatively tranquil for a while with precipitation most likely from the Baltic States to the Volga Vyatsk where several inches of snow will accumulate

- Other areas in the western CIS are unlikely to experience much precipitation for a while

- Temperatures will be warmer than usual through the next two weeks

- Northern and eastern India will experience a couple of weak weather disturbances this week and during the weekend that will lift topsoil moisture briefly in support of some short term improvements in crop and field conditions ahead of reproduction

- Moisture totals of 1.00 to 3.00 inches and locally more will occur from Uttarakhand to Jammu and Kashmir

- Rainfall in Punjab, Haryana and northern Uttar Pradesh will vary from 0.05 to 0.65 inch with a few totals to nearly 0.80 inch

- A trace to 0.60 inch of moisture is expected from eastern Rajasthan to central and southeastern Uttar Pradesh; including northern Madhya Pradesh

- Drier weather will resume next week

- The moisture will be good for improved pre-reproductive wheat, pulse crops and a few other winter grain and oilseed crops, but more rain will be needed to induce the best yields for unirrigated crops

- China’s precipitation in the coming week will be limited with net drying most likely

- Some rain will develop in early February

- Temperatures will be warmer than usual except for early this week in the northeast when readings will be colder than usual

- Western Turkey will receive frequent rain and mountain snow over the next ten days

- Eastern Turkey will receive more limited precipitation until late this weekend and next week when a boost in precipitation is expected

- Other areas in the Middle East will not receive significant precipitation this week, but see greater precipitation in the second week of the two week outlook

- South Africa rainfall through the weekend will be greatest in Eastern Cape and Natal while net drying occurs in other areas

- The moisture will be welcome, but there will be a slowly rising bout of moisture stress in some of the drier areas from Northern Cape through Free State and North West to Limpopo and Mpumalanga

- A timely boost in rainfall should evolve next week to reduce concerns of moisture stress

- Eastern Australia precipitation will be limited over the coming five days with only a few showers expected and net drying likely

- Showers and thunderstorms will begin to develop daily this week, but the greatest rainfall will hold until next week

- The moisture will bring some relief to dryness and benefiting unirrigated sorghum and cotton

- West-central Africa will receive some coastal showers this week and the precipitation may increase and reach a little farther inland next week

- Some rain developed Tuesday in a few southern Ivory Coast locations benefiting coffee, cocoa and sugarcane production areas

- Some of the advertised precipitation may be overdone, but it could be beneficial for a few coffee and cocoa production areas as long as there is follow up moisture once it begins to rain periodically

- Dry weather occurred during the weekend

- Southeast Asia rainfall will be most significant in Indonesia and Malaysia as well as eastern portions central and southern Philippines over the next ten days

- The moisture will be good for ongoing crop development, although a few areas may become a little too wet

- East-central Africa rainfall will remain most significant in Tanzania and southern Uganda while more limited in areas north into Ethiopia which is not unusual for this time of year

- Today’s Southern Oscillation Index was +14.81 today and the index is expected to level off for a while.

Source: World Weather, Inc and FI

Macros

US MBA Mortgage Applications Jan 20: 7.0% (prev 27.9%)

US 30-Yr MBA Mortgage Rate Jan 20: 6.20% (prev 6.23%)

Bank Of Canada Increases Policy Interest Rate By 25 Basis Points, Continues Quantitative Tightening

US Cold Storage Stocks – USDA

– U.S. frozen beef stocks 543.955 mln lbs as of Dec 31

– U.S. frozen pork belly stocks 63.060 mln lbs as of Dec 31

– U.S. frozen orange juice stocks 0.290 bln lbs as of Dec 31

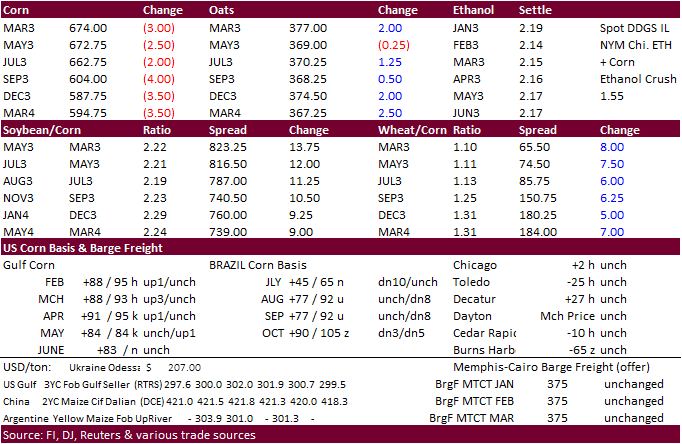

· CBOT corn futures closed lower on South American moisture, helping stabilize the corn and soy crop.

· Mexico’s Deputy AgMin Suarez said they will not be able to replace its imported corn with internal production by 2024, but it hopes to reduce imports by 30-40%.

· There are rumors China is in for US corn. US Gulf basis was up yesterday (about 5 cents) while Brazil was unchanged to 8 cents lower.

· Bulgaria reported a bird flu outbreak at an industrial farm near the capital Sofia resulting in the culling of 25,000 quails and discard quail eggs.

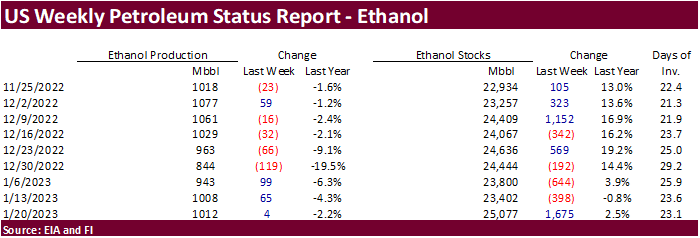

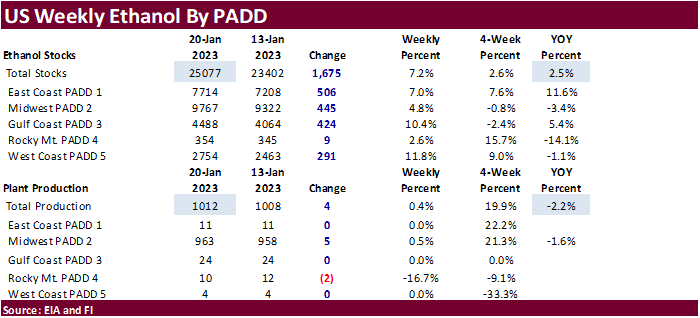

· US ethanol. We advise to look at the 4-week averages for production and stocks (attached). US EIA reported weekly ethanol production up 4,000 barrels per day and stocks up 1.675 million. For comparison, a Bloomberg poll looked for weekly US ethanol production to be up 6,000 thousand barrels and stocks up 235,000 barrels.

US DoE Crude Oil Inventories (W/W) 20-Jan: +533K (est +1.500M; prev +8.408M)

– Distillate: -507K (est -1.600M; prev -1.939M)

– Cushing: +4.267M (prev +3.646M)

– Gasoline: +1.763M (est +1.500M; prev +3.483M)

– Refinery Utilization: +0.8% (est +1.9%; prev +1.2%)

Export developments.

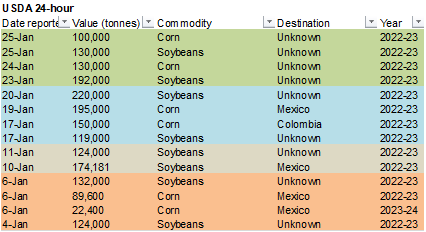

· Under the 24-hour reporting system, USDA reported private exporters sold 100,000 tons of corn to unknown destinations for 2022-23 delivery.

Updated 01/19/23

March corn $6.50-$7.25 range. May $6.25-$7.20

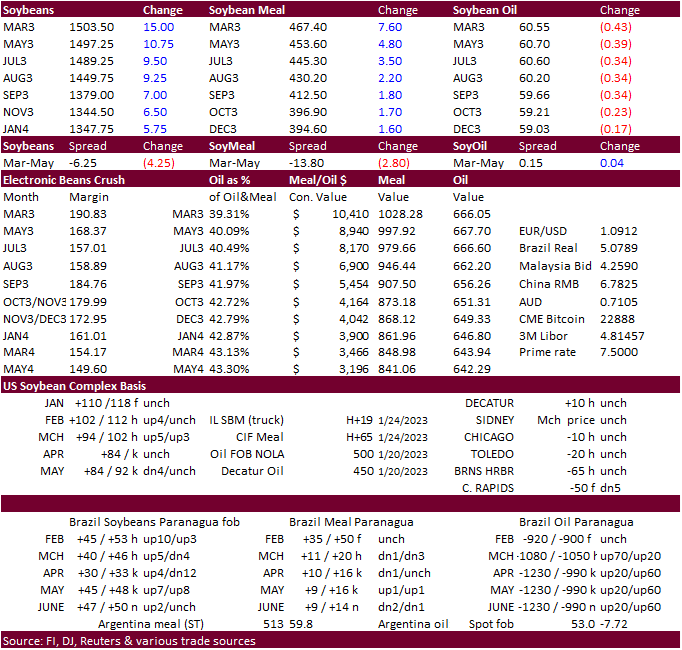

· US soybeans closed higher on short covering and value buying on the holding of technical levels overnight.

· The Rosario grains exchange said Argentina received more than expected rains but were “unevenly spread throughout the country.” In a Reuters note citing the exchange…”only 15% of the Pampas region received rainfall above the key level of 45 mm. The Buenos Aires area received 15%, La Pampa 10%, Santa Fe 5% and Cordoba 3%. Some areas got none at all.”

· Cargo surveyor ITS reported Malaysian palm oil January 1-25 exports fell 34.7% to 824,373 tons from 1.262 million tons during the December 1-25 period. AmSpec reported a 32.9% decline to 823,376 tons from 1.227MMT.

MPOA Jan 2023 CPO 1-20 day production (from Anil Bagani):

Peninsular Msia (-) 9.50%

Sabah (-) 11.74%

Sarawak (-) 18.61%

East Msia (-) 13.50%

Malaysia (-) 11.22%

· Northern Brazil should see additional soybean harvesting delays with more rain on the way over the next week.

· Brazil soybean export basis firmed the last 2 days.

· GAPKI reported 2022 Indonesia palm oil shipments declined 8.5 percent from the previous year to 30.8 million tons from 33.7 million during 2021. There was a short ban last April on palm oil which contributed to the decline. Indonesia plans to raise their biofuel blend to B35 from B30 this February. 2022 crude oil palm production was 46.7 MMT, down 0.4% from 2021. Stocks were ample at just over 3.6 million tons at the end of December. Production via Reuters…

· Indonesia set its February 1-15 palm oil reference price at $879.31/ton, down from $920.57/ton for the LF January period. CPO export tax resets at $52 per ton and levy at $90 per ton.

· Indonesia is planning to change the way exporters do business, or reverting back to a similar 2019 plan, by requiring them to hold their foreign exchange earnings offshore for at least three months, in a special account, held domestically. This should not change trade flows.

· There were 11 CBOT soybean registrations were cancelled (Chicago) Tuesday evening.

· Refinitiv Ag Research left Paraguay soybean production unchanged at 9.4 million tons. Despite dry conditions, the satellite imagery remains favorable.

· Russia plans to keep its sunflower oil export duty at zero percent during February. Sunflower meal will increase from 1,826.9 rubles ($26.47) per ton in January 2022 to 2,200.7 rubles ($31.9) per metric ton in this February.

· China is on holiday all week.

· Nearby Rotterdam vegetable oils were 10-25 euros lower from early yesterday morning. Rotterdam meal was mostly 2-5 euros lower.

· Offshore values were leading SBO higher by about 433 points this morning and meal $2.50 short ton lower.

· Under the 24-hour reporting system, USDA reported private exporters sold 130,000 tons of soybeans to unknown destinations for 2022-23 delivery.

· South Korea seeks up to 40,000 tons of rapeseed meal from India on Thursday for May 21-June 10 shipment.

· The CCC seeks 3,770 tons of vegetable oils on February 1 for last half March shipment.

Updated 01/19/23

Soybeans – March $14.75-$15.75, May $14.75-$16.00

Soybean meal – March $450-$520, May $425-$550

Soybean oil – March 60.00-68.00, May 58-70

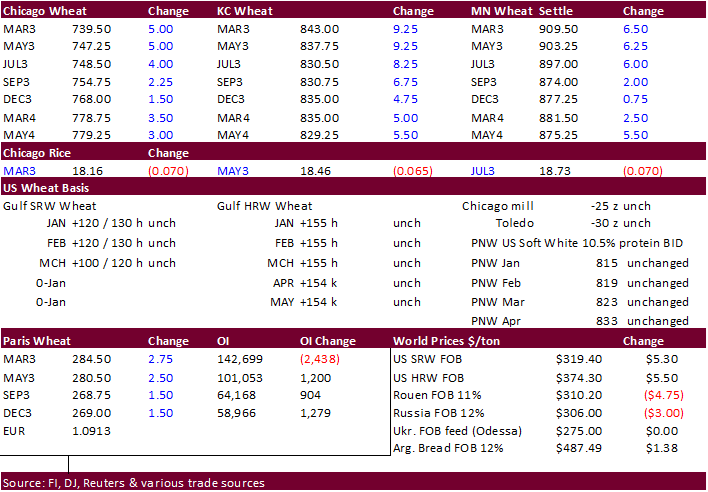

· Wheat continued higher with today’s bullishness caused by the escalating tensions between Ukraine and Russia following news that the US and Germany are providing advanced tanks and armored vehicles to Ukraine.

· India’s government plans to release 3 MMT of wheat reserves to bulk consumers to cool prices. Domestic wheat prices hit a record earlier this week. 2-3 MMT was expected for release. 3 million tons is just less than 3 weeks of total domestic consumption. https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=India%20Grain%20and%20Feed%20Update%20-%20December%202022_New%20Delhi_India_IN2022-0110

· Paris March wheat was 1.50 euros higher earlier at 284.50 per ton.

Export Developments.

· Jordan seeks 120,000 tons of wheat on Jan 31 for May and June shipment.

· Iraq bought 150,000 tons of Australian wheat at $445/ton c&f for April shipment.

· Japan seeks 70,000 tons of feed wheat and 40,000 tons of barley for arrival in Japan by March 16.

· Jordan seeks 120,000 tons of wheat and barley on January 31.

Rice/Other

· None reported.

Updated 01/19/23

Chicago – March $7.00 to $8.00, May $7.00-$8.25

KC – March $7.75-$9.00, $7.50-$9.25

MN – March $8.75 to $10.00, $8.00-$10.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18W140 Butterfield Rd.

Suite 1450

Oakbrook Terrace, Il. 60181

Work: 312.604.1366

ICE IM: treilly1

Skype IM: fi.treilly

DISCLAIMER:

The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. This communication may contain links to third party websites which are not under the control of FI and FI is not responsible for their content.

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.

#non-promo