PDF Attached

Reminder,

Friday is position day for March

Private

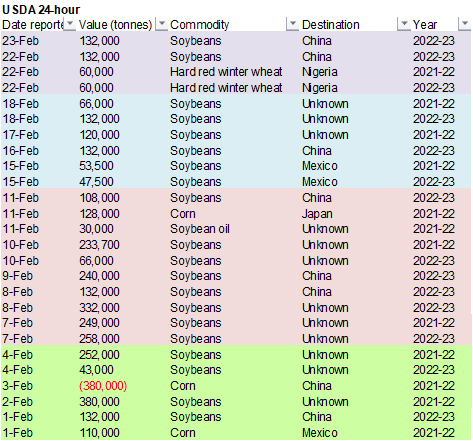

exporters reported sales of 132,000 metric tons of soybeans for delivery to China during the 2022/2023 marketing year.

US

major agriculture markets were up sharply on Ukraine/Russia concerns, global money inflow from equities, higher outside commodity markets and fund buying. Some contracts made multi year highs today, such as Chicago wheat (9-year high).

![]()

The

USDA Agriculture Forum will be held Thursday and Friday and the trade will get a glimpse of 2022 US supplies on Thursday, followed by full S&D’s Friday morning.

https://www.usda.gov/oce/ag-outlook-forum

WEATHER

EVENTS AND FEATURES TO WATCH

- Bitter

cold air settled over the central and northern U.S. Plains and a part of the upper Midwest this morning raising some concern over the health of hard red winter wheat in many areas from the Texas Panhandle to Nebraska.

- Minimal

snow cover was present in hard red winter wheat areas - Temperatures

were cold enough to induce some winterkill in the north, although it is unclear how much of an impact the recent warm weather had on crops - Most

of the wheat lost winter hardiness, but very little crop development has likely occurred in the coldest areas of the north limiting the potential for widespread damage - However,

temperatures were cold enough to raise concern and the region has seen other bouts of bitter cold this year without snow on the ground and there is some concern over the state of crops

- Temperatures

in the Texas Panhandle and northwestern Oklahoma fell to the positive single digits after being in the 60s and 70s earlier this week and during the late weekend - Heaving

soil and crop moisture stress are still big issues in the southwestern Plains, but no clear assessment of damage can be determined until new crop development becomes aggressive and there is some potential that the crop will look like it is developing, but

in may produce empty heads of rain - Hard

red winter wheat needs a cool, wet, spring to set new tillers and repair other plant damage before reproduction, but there is no such pattern change coming for the high plains region.

- Cold

weather in the U.S. Plains will prevail through the end of this week and it will expand a little farther into the western and northern Midwest, but soft wheat in the Midwest is not likely to be seriously impacted.

- More

rain will fall in the lower eastern U.S. Midwest, the Delta and Tennessee River Basin through the next couple of weeks maintaining concern over wet field conditions, possible flooding and early season planting delays - Far

southeastern U.S. will experience very warm temperatures and limited rainfall over the next few days accelerating the region’s drying trend and raising concern over future planting moisture - Some

cooling and a chance for rain will develop briefly late this week and into the weekend, but it will be followed by more dry and warm weather next week - Argentina’s

weather outlook is still wet looking for the coming week to ten days with all areas in the nation getting rain at one time or another by mid-week next week

- The

change occurred during the weekend suggesting greater rainfall than that advertised late last week – the change should verify - World

Weather, Inc. has been expecting this change and it is being advertised at about the same time our Trend Model suggested which adds confidence that this change will verify - Argentina

will experience restricted rainfall into Wednesday morning, but rain will develop late Wednesday and Thursday in much of the central and south (including the drier areas noted above) - Follow

up rainfall is expected Friday into the weekend impacting east-central and northern crop areas

- Northern

Argentina may continue getting some showers early next week - The

precipitation will see to it that all of the nation gets relief from dryness at one time or another. Some of the amounts advertised are a little too aggressive, but there will be sufficient amounts to stop the decline in late summer crop conditions and production

potentials – at least for a while - Seasonal

weather changes expected in March will make it very difficult for there to be a return of dryness to the levels seen in recent weeks, but there will be some breaks in the precipitation periodically - Rain

totals will vary from 1.00 to 2.00 inches in the central and south with a few areas getting 2.00 to more than 3.00 inches - Northern

Argentina’s rainfall is supposed to be significant in the interior north, but there may still be a little drier bias in parts of the region after next week - Future

model runs may back off of some of the predicted rain, but the coverage will remain sufficient to improve cop and field conditions in central parts of the nation while maintaining good soil moisture in the south - Brazil

rainfall is still advertised to be a little lighter than usual in the interior south, but Rio Grande do Sul and immediate neighboring areas should get sufficient rain to improve topsoil moisture like that of Argentina - Mato

Grosso do Sul will be most closely monitored for less than usual rainfall along with a few areas in neighboring northern and western Parana - These

areas will continue drying out for another week and then get some needed rain - Northern

Brazil weather is still expected to see improving conditions later this week with less frequent and less significant precipitation that would help to mature late season soybeans and other crops faster after a prolonged period of wet weather - Coffee,

citrus and sugarcane production areas in Brazil are still rated favorably with little change likely over the next ten days - West

Texas rainfall will continue restricted over the next ten days to two weeks resulting in rising concern over short soil moisture for the planting season which occur in May for cotton and a little sooner for corn and some other crops - California

precipitation is expected to be lighter than usual during the next ten days leaving some concern over mountain snowpack and snow water equivalency for runoff when the snow melts this spring and summer - Ecuador,

Peru and Colombia crop areas will continue to see frequent rain over the next week maintaining moisture abundance for some areas and raising soil moisture in other areas - Southern

China will get a break from recent wet weather this week with much less rain and less frequent precipitation.

- Temperatures

should trend a little warmer, but they will be cooler biased for a while this week. - Most

other areas in China are experiencing mostly good crop and field conditions - Wheat

and rapeseed are mostly dormant or semi-dormant, but poised to perform well this spring if temperatures warm up normally in March and April - Some

rapeseed areas in the Yangtze River Basin have been too wet recently and this week’s drier weather will be welcome - Northern

Vietnam and northern Laos received a general soaking rain during the weekend, but are dying down now - The

precipitation was a part of the same system that also impacted southern China.

- Some

flooding resulted when rain totals reached up over 5.00 inches - The

precipitation was great enough to possibly induce some premature coffee flowering, although cool temperatures might have helped to curtail that event - Some

winter rice crop quality decline might have occurred - Drier

weather is expected over the next week to ten days - Indonesia,

Malaysia and Philippines weather will remain mixed over the next ten days with most crops staying in good condition. - Spain

and Portugal need greater rainfall for their unirrigated winter and spring crops.

- Some

showers are expected late this week into early next week, but the distribution of rain may prove disappointing and much more rain will still be needed for unirrigated crops - Northwestern

Africa continues too dry, but some showers will develop this weekend into next week and continue next week and any precipitation that occurs will be welcome - Morocco

is driest with a cut in area planted in the southwest because of a multi-year drought and no irrigation water - North-central

Morocco crops were favorably established in the autumn, but are dry now and need significant moisture soon to support aggressive crop development ahead of spring reproduction - Northeastern

Morocco and northwestern Algeria are also quite dry and poised to suffer a production cut without significant rain soon - Northeastern

Algeria and Tunisia winter wheat and barley are best established and have the greatest potential for high yields as long as timely rain falls over the next few weeks

- Greater

rain will still be needed, but any moisture in the coming week to ten days will be helpful giving the driest crops more time to avoid worsening stress until greater rain evolves - Most

of Europe outside of the Iberian Peninsula and parts of Romania are favorably moist with routinely occurring precipitation in the next ten days supporting status quo winter crop conditions.

- Greater

rain must occur soon for Spain and Portugal and at some time in the next few weeks in Romania to prevent dryness from threatening early season crop development - Weather

in the coming ten days will produce light and somewhat erratic precipitation, but soil moisture is good except as noted above leaving the outlook relatively benign on agriculture.

- Western

Russia, northwestern Ukraine, Belarus and Baltic States have abundant soil moisture underneath a significant accumulation of snow - Flood

potentials may be high for the spring this year if the region heats up too fast and all of the snow melts over a short period of time - There

is no threatening cold temperatures expected in Europe or any part of Europe during the next ten days to two weeks - Temperatures

will be above normal especially in Russia, Ukraine and eastern Europe - Kazakhstan

and southern Russia’s New Lands will receive only light amounts of precipitation in the next ten days, but any moisture would be welcome for improved topsoil conditions in the spring - Recent

snowfall has changed the early spring moisture outlook at least a little, but the region still has moisture deficits left over from drought last summer and greater precipitation will be needed in the spring.

- Middle

East winter crop conditions have improved in recent weeks because of a short-term boost in precipitation, but more rain is needed to ensure the best possible production - Some

precipitation is expected in the coming ten days, but it will be greatest in Turkey - Other

areas may need greater precipitation soon - India

precipitation will be limited to a few sporadic very light showers during the next ten days except in the far north and extreme east where some moderate rain may impact a few areas - The

bulk of winter crops in the nation are poised to perform well barring no excessive heat in the next few weeks - At

least one more timely rain event would help push yields high than usual - Xinjiang,

China precipitation is expected to be restricted during the next week to ten days - The

province need moisture to support spring planting in a few weeks - Eastern

Australia’s summer crop areas will receive isolated to scattered showers and thunderstorms this week - The

resulting precipitation will be ideal for reducing moisture stress in unirrigated crops, although greater volumes of rain might still be needed for the late maturing crop - The

precipitation might not be as well distributed as desired, but the majority of most important cotton and sorghum areas will get at least a little moisture - Irrigated

crops will remain in mostly favorable condition - South

Africa will receive rain in the east from eastern Limpopo through Mpumalanga to Natal and Eastern Cape while other areas experience net drying - Precipitation

may continue in this manner into early next week before there is much chance for rain in western production areas - Summer

crop conditions are still rated quite favorably. - West-central

Africa coffee and cocoa production areas will experience additional showers in the coming week, but the precipitation will stay confined to coastal areas - There

is some potential for greater rain in Ivory Coast and Ghana next week - East-central

Africa precipitation has been and will continue to be most significant in Tanzania which is normal for this time of year.

- Ethiopia

is dry biased along with northern Uganda and that is also normal - Tuesday’s

Southern Oscillation Index is +10.11 - The

index will move erratically for a while this week - Mexico

will experience seasonable temperatures and a limited amount of rainfall during the coming week - Central

America precipitation will be greatest along the Caribbean Coast during the next seven to ten days - Guatemala

will also get some showers periodically - Tropical

Cyclone Emnati was impacting Madagascar today with torrential rain and flooding along with some strong wind speeds.

- Damage

assessments will begin Thursday.

Source:

World Weather Inc.

Bloomberg

Ag Calendar

- USDA

total milk production, 3pm - EARNINGS:

IOI Corp. - HOLIDAY:

Japan, Russia

Thursday,

Feb. 24:

- USDA

corn, cotton, soybean and wheat acreage outlook, 8:30am - EIA

weekly U.S. ethanol inventories, production, 11am - U.S.

red meat production, 3pm

Friday,

Feb. 25:

- USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am

- ICE

Futures Europe weekly commitments of traders report, ~1:30pm - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - USDA

corn, cotton, soybean and wheat end-stockpile outlook, 8:30am - FranceAgriMer

weekly update on crop conditions - Malaysia’s

Feb. 1-25 palm oil exports - U.S.

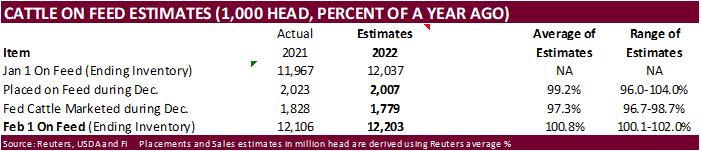

cattle on feed, 3pm

Source:

Bloomberg and FI

Macros

JPMorgan:

Oil Prices Seen Averaging $110 In Q2

Moscow

Will Give Strong Response To New US Sanctions – RIA Cites Russian Foreign Ministry

There

were reports Ukraine’s parliament will declare a state of emergency for 30 days. We don’t know if that will impact transportation.

U.S.

Eyes Release From Oil Reserves as Prices Rise on Ukraine

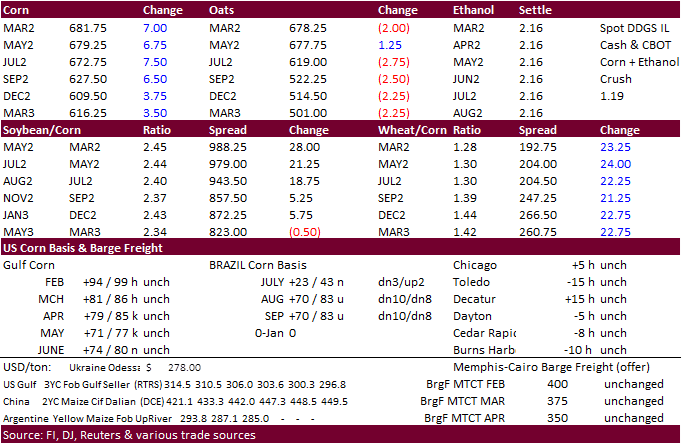

Corn

·

Two-sided trade. CBOT corn was lower this morning only to rally after wheat and soybean prices surged. But sink again just after USDA announced bird flu outbreak in Delaware. Then rallied again to close 8.75 cents higher basis

May.

·

The USDA reported a bird flu outbreak in a commercial poultry flock in Delaware. This comes after of the highly pathogenic avian flu was reported in several states this year. Variants of bird flu have been detected in New York,

Maine, North Carolina, South Carolina, Virginia, Indiana (at least three farms) and Kentucky. China and Mexico has already placed trade restrictions.

·

World Weather noted most of Argentina, Uruguay, far southern Paraguay and far southern Brazil will get rain in this first week of the outlook. Interior southern Brazil will be dry until the second half of next week. Northern Brazil

is still expected to improve with less rain, allowing for soybean harvest to advance followed by second corn plantings.

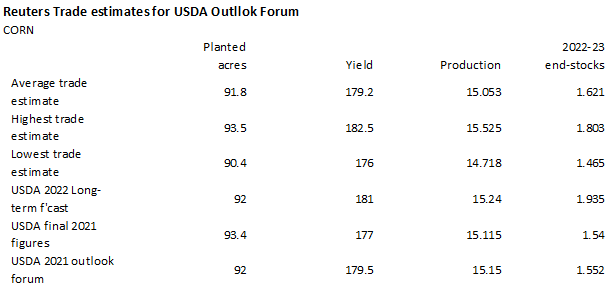

·

A Reuters trade guess calls for 91.8 million acres for 2022 corn (90.4-93.5 range),

down from 93.4 million for 2021. USDA baseline for 2022 was 92.0. Stocks are expected to rise to 1.621 billion bushels from 1.540 billion for 2021-22.

·

Brazil consultancy Datagro estimated the 2021-22 corn crop at 117.82 MMT versus 115.22 million tons previously.

·

The USDA weekly Broiler Report showed eggs set in the United States up 4 percent and chicks placed up 1 percent. Cumulative placements from the week ending January 8, 2022, through February 19, 2022 for the United States were

1.30 billion. Cumulative placements were down 1 percent from the same period a year earlier.

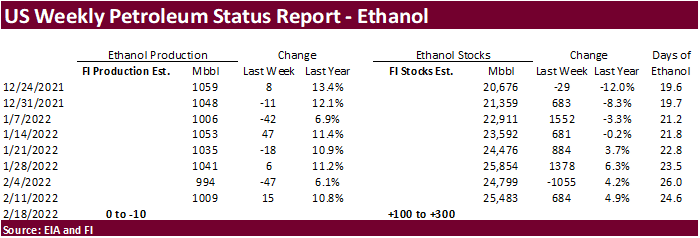

·

A Bloomberg poll looks for weekly US ethanol production to be up 1,000 barrels to 1.010 million (1000-1022 range) from the previous week and stocks up 135,000 barrels to 25.618 million.

Export

developments.

- Taiwan’s

MFIG seeks up to 65,000 tons of corn which from the United States, Brazil, Argentina or South Africa, on Friday, Feb. 25, for shipment between May 1 and early June shipment, depending on origin.

Updated

2/22/22

March

corn is seen in a $6.35 and $7.10 range

December

corn is seen in a wide $5.50-$7.25 range

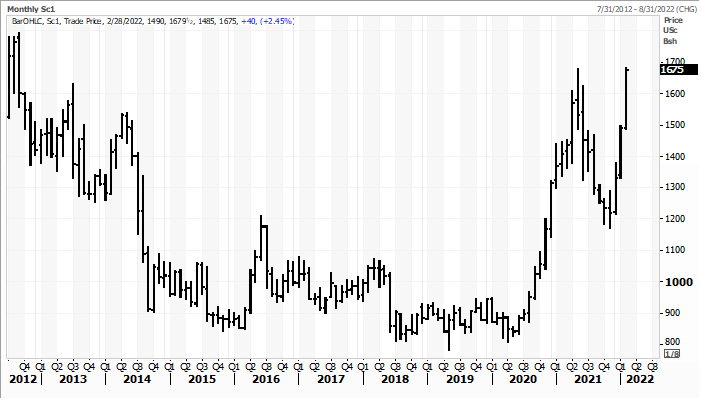

·

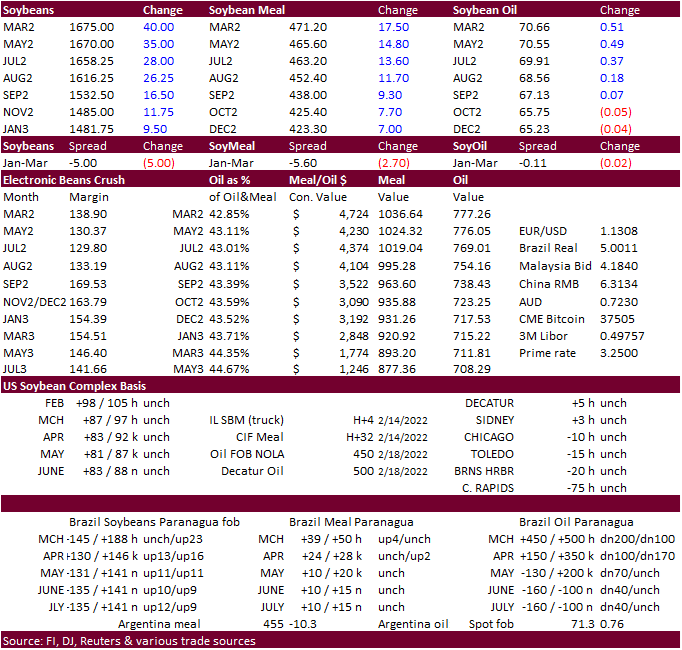

CBOT soybeans reached their highest level since September 2012 (9-year high) on a rolling basis and climbed the last 5 consecutive sessions. The nearby rolling contract to (high $16.7950 took out the previous high made on May

14, 2021 high of $16.7725. Dry weather for SA is still a big factor behind soybeans. Brazil soybean premiums jumped yesterday.

·

Meal turned sharply higher following Brazil meal premiums (heard they were up sharply) and Iran seeking additional soybean meal. May meal settled $15.20 higher at $466. The contract high is $$474.90.

·

CBOT soybean oil hit its highest level since June 2021, on a nearby monthly rolling basis.

·

USDA announced another 132,000 tons of soybeans to China. The lack of soybean oil sales after talk last week India bought US SBO is a little disappointing, but something to monitor in the upcoming export sales report.

·

Sunflower oil, still discounted to other major vegetable oils, has been rallying. Black Sea cash prices were up sharply today. Traders are concerned about Ukraine supplies, which account to around 75 percent sunoil global export

market share.

·

Palm oil futures hit a record high. The Malaysian Palm Oil Association estimated palm production during Feb. 1-20 fell 1.79% from the month before. (Reuters)

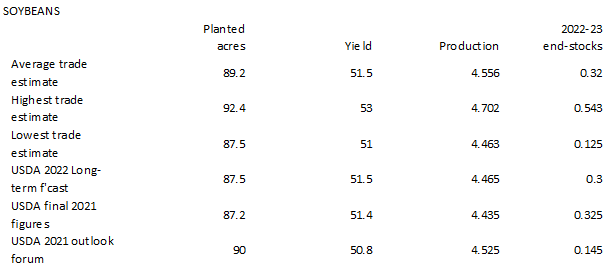

·

For USDA’s outlook forum, a Reuters trade guess calls for 89.2 million acres for 2022 soybeans (87.5-92.4 range),

up from 87.2 million for 2021. USDA baseline for 2022 was 87.5. Stocks are expected to decrease to 320 million bushels from 325 million for 2021-22.

·

Argentine producers sold 39.2 million tons of soybeans from the 2020-21 season, up 368,200 tons from previous week and down from 40.7 million year ago.

·

China’s AgMin again announced they intend to expand soybean plantings by utilizing “every patch of land.” No figures were provided.

·

Brazil consultancy Datagro estimated the 2021-22 soybean crop at 130.25 MMT versus 130 million tons previously.

Soybeans

– weekly continuation Today’s high of $16.7950 took out previous high of $16.7725 on May 14, 2021

Source:

Reuters and FI

- Iran’s

SLAL seeks up to 60,000 tons of soybean meal and 60,000 tons of feed barley on Feb. 23 for an unknow shipment period.

- Exporters

sold 132,000 tons of soybeans for delivery to China during the 2022/2023 marketing year, according to the USDA. - Turkey

bought 6,000 tons of sunflower oil at an estimated $1,474.90/ton c&f for March 2-25 shipment.

Updated

2/22/22

Soybeans

– May $15.00-$17.50

Soybeans

– November is seen in a wide $12.50-$16.00 range

Soybean

meal – May $425-$500

·

US wheat was the leader today in ags. They started mixed but ended sharply higher. Uncertainty over Russia/Ukraine situation should continue to create a volatile trade environment.

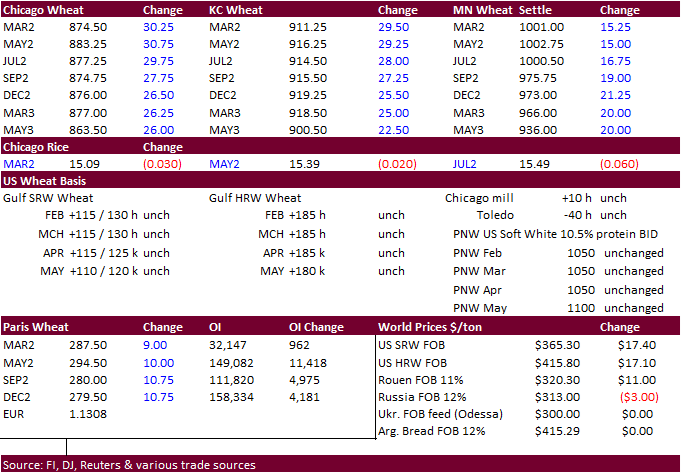

·

May Chicago wheat took out its previous contract high of $8.79 made on November 24, 2021. Nearby Chicago reached highest level since November 2012. KC is also at highest since November 2012. MN May wheat is at a December 29,

2021 high.

·

US winter wheat conditions, already at low levels for the combined good/excellent categories, declined for selected key states from a month ago (Texas declined from previous week). See attachment.

·

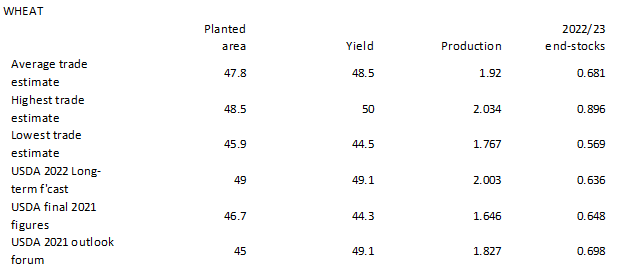

For USDA’s outlook forum, a Reuters trade guess calls for

47.8 million acres for 2022 all-wheat (45.9-48.5 range), up from 46.7 million for 2021. USDA baseline for 2022 was 49.0. Stocks are expected to rise to 681 million bushels from 648 million for 2021-22.

·

May wheat settled up 9.50 euros, or 3.3%, at 294.00 euros ($332.48) a ton.

·

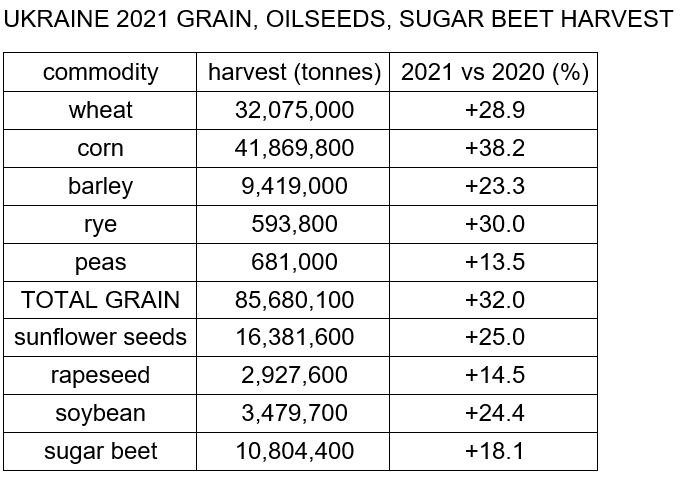

Ukraine’s grain harvest increased 32 percent in 2021 to 85.68 million tons, according to state statistics.

·

12 percent of Ukraine’s winter wheat crop area is in poor condition, according to the state weather forecaster. That’s about 900,000 hectares. 90-95% of the winter crop survived so far.

Bloomberg

noted the following winter wheat conditions (table attached)

- Kansas

winter wheat rated good or excellent fell by 4 percentage points from last month - Oklahoma

conditions fell by 7 points to 9% good/excellent from last month - Texas

conditions fell by 11 points from the previous week

Reuters

table for Ukraine below.

·

Egypt seeks wheat for April 11-21 shipment.

·

Turkey seeks 435,000 tons of milling wheat on March 2 for March-April shipment.

·

Bangladesh bought 50,000 tons of wheat on February 14 at $390.92/ton CIF.

·

Jordan’s state grain buyer passed on 120,000 tons of milling wheat, optional origins. Shipment as follows: 60,000 ton consignments, for July 16-31, Aug. 1-15, Aug. 16-31 and Sept. 1-15.

·

Jordan seeks 120,000 tons of feed barley on March 1.

Rice/Other

·

South Korea seeks 72,200 tons rice from U.S. and Vietnam on Feb. 25.

Updated

2/22/22

Chicago

May $7.85 to $9.00 range

KC

May $7.80 to $9.25 range

MN

May $9.00‐$10.50

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.