PDF Attached

Private

exporters reported the following activity:

-136,000

metric tons of soybeans for delivery to China during the 2022/2023 marketing year

-120,000

metric tons of soybeans for delivery to unknown destinations during the 2021/2022 marketing year

No

expanded limits in CBOT contracts

https://www.cmegroup.com/trading/price-limits.html

We

last heard May corn synthetic was $6.9175.

May

corn closed limit up but since the other months failed to close limit, CME will leave its 35 cent threshold unchanged for Tuesday. Black Sea shipping concerns and higher outside related commodity markets supported US agriculture futures.

We

understand the peace talks did not go well today.

Weather

– rain

to develop back end of 7-day outlook

WEATHER

EVENTS AND FEATURES TO WATCH

- U.S.

hard red winter wheat areas will turn much warmer this week with high temperatures rising well above normal

- Extremes

in the upper 60s and 70s Fahrenheit will be common with a number of lower 80-degree highs expected in time - Nighttime

low temperatures will stay above freezing for a few days, but cooling should come around late this and during the weekend to slow the warming trend in the north - Wheat

is dormant today, but it will lose winter hardiness this week with some greening in the south - There

is some moisture in the fields and at least some greening will occur - Greening

may help farmers determine to what extent winterkill occurred this year, although the full extent of crop damage will not be discovered for many weeks - Cooling

is expected next week and that should be sufficient to shut down any greening that begins this week in northern production areas - Not

much precipitation will occur over the next week in the central or southwestern U.S. Plains leaving concern over the health of hard red winter wheat and the prospects for spring planting in some areas - Rain

is needed, but not likely in large quantities for a while - A

couple of weather systems next week will attempt to bring some moisture to the region and one more will bring a little moisture to northern parts of the region late this week and into the weekend - West

Texas, South Texas and the Texas Coastal Bend areas will experience net drying and warmer weather this week, but some rain “may” evolve next week in a few of these areas – mostly in the Coastal Bend - Southeastern

U.S. corn, cotton and peanut production areas of southern Georgia, southern South Carolina, southeastern Alabama and northern Florida will be drying out additionally during the next few weeks raising worry over the success of spring planting - U.S.

weekend precipitation was greatest from eastern Texas through the heart of the Delta top the Tennessee River Basin the southern Appalachian Mountains

- Moisture

totals varied from 0.40 to 1.50 inches through Sunday morning with Houston, Mississippi reporting 2.15 inches and Cleveland, MS reported 2.32 inches - Much

lighter precipitation fell in other areas in the mid-south region while the Midwest, Great Plains and far west were left dry - Some

rain fell in western Washington and northwestern Oregon - Temperatures

were mild to cool in much of the nation Friday and Saturday, but warming in the Plains Sunday sent afternoon readings into the 50s and 60s Fahrenheit with some of that warmth getting into southern South Dakota where some 50s were noted - Snow

free conditions continued in the U.S. central Plains, but lowest temperatures Saturday and Sunday were only in the positive single digits which should not have been cold enough to induce damage - Low

temperatures late last week in Kansas, Colorado and Nebraska’s snow free areas were in the negative and positive single digits possibly damaging some crops. - U.S.

temperatures will be non-threatening over the next two weeks to wheat and other winter crops - Readings

this week will be above normal from the central and southern Plains to the southern Atlantic Coast states - Warm

weather will also occur in the southwestern desert region and northward into the Rocky Mountain region - Cool

weather will be limited to the northern Plains and northeastern states - Cold

air will return to the Canadian Prairies and the northern central U.S. Plains next week with the greatest anomalies in the Prairies and northern Plains - Warm

weather will impact most of the eastern states - U.S.

Lower Midwest, Delta and Tennessee River Basin will experience net drying through Saturday of this week - Each

of these areas will get rain Sunday and Monday of next week maintaining saturated or nearly saturated soil - Another

round of significant rain may impact the region during the second half of next week and into the following Saturday, March 12. - Northern

U.S. Midwest is unlikely to see much precipitation through Friday of this week - A

new storm during the weekend may impact the northern Midwest and northern Plains and northern Midwest with snow and rain - Colder

and drier air should follow close behind - U.S.

bottom line has not changed much. Concern over excessive spring moisture from the lower Midwest into the northern Delta and Tennessee River Basin is expected this year because of a mostly unchanging weather pattern brought on by La Nina and negative PDO along

with the 22-year solar cycle. Similarly, the high Plains of the U.S. central and southwestern Plains will remain dry including West Texas cotton, corn, sorghum and wheat production areas. California precipitation will also remain restricted while the northwestern

Plains and southwestern Canada Prairies get only light amounts of precipitation. The southeastern U.S. will steadily dry out and concern over planting moisture will develop there in March just as the concern over too much moisture and planting delays impacts

the lower Midwest, northern Delta and Tennessee River Basin. Cooling and rain are needed in hard red winter wheat production areas, but that is not very likely.

- Argentina

rainfall during the weekend was greatest from southern Santa Fe, southern Cordoba and northeastern La Pampa to Uruguay and parts of Buenos Aires - Rainfall

varied widely from 0.20 to 1.65 inches most often, but 3.00 to more than 6.20 inches occurred in a band across far northern Buenos Aires to central Uruguay and southeastern Entre Rios - Some

flooding resulted - Net

drying occurred in southwestern Buenos Aires, southern La Pampa, eastern portions of Buenos Aires’ south coast and in much of the region from central Cordoba through central Santa Fe to northern Entre Rios to Bolivia and Paraguay - The

weekend precipitation was great for late season summer crops especially after significant rain fell in these same areas late last week - Rain

is still needed in northern Argentina where the weekend was dry and very warm - Some

of the needed relief will occur this week, although the region will need more rain - All

of Argentina will get rain at one time or another during the next ten days and sufficient amounts will occur to either improve crops in the drier areas or maintain favorable crop conditions in others - Temperatures

will be very warm in northern Argentina early this week until rain begins to fall and then some cooling is expected - Near

to above average temperatures are expected in the central and south - Argentina’s

bottom line is still one of improvement. Northern Santa Fe, Chaco, Corrientes and immediate neighboring areas still need more generalized rain of significance and it should come over the next week to ten days improving crop and field conditions for late season

crops. The best soil and crop conditions remain in Buenos Aires, southern Cordoba, southwestern Santa Fe, northeastern La Pampa and San Luis which represents a large part of the nation’s summer crop region. Crop yield declines in the rest of Argentina should

stop with additional rain later this week and into next week. - Brazil

rainfall during the weekend was erratic and often light resulting in net drying for many areas - Temperatures

were warm to hot - Western

areas were warmest with highs in the middle and upper 90s Fahrenheit - Rainfall

was greatest in central Mato Grosso and from southern Parana into Misiones and western Santa Catarina - Brazil

rainfall will be restricted this week in center south and northeastern parts of the nation where resulting rainfall of 0.20 to 0.75 inch and a few greater amounts will not likely counter evaporation and net drying will result - The

environment will be great for early season crop maturation and harvest progress - Brazil

rain is expected in far southern parts of the nation this week with 1.50 to more than 4.00 inches resulting by Saturday

- Areas

from Rio Grande do Sul to Parana will be most impacted and a few amounts will reach up over 5.00 inches

- Mato

Grosso also see daily rainfall benefiting cotton and corn production areas - A

few Tocantins, Goias and western Bahia will get rain routinely during the weekend - Temperatures

will be warm in the southwest and near to below average elsewhere - Brazil’s

bottom line is still one of improvement in the far south because of expected rain and in the far north because of less rain. Mato Grosso will stay plenty wet for Safrinha crops while better harvest weather is expected in Minas Gerais, Goias and immediate neighboring

areas because of less rain. Dryness in center south crop areas will prevail into the end of this week and then begin to get some rain. Crops in the Mato Grosso do Sul and western and northern Parana will be most stressed until rain evolves late this week into

next week. Not much new production cut is expected. - More

abundant rain is expected this week in Colombia, Ecuador, northern Peru and western Venezuela this week.

- Northern

parts of the Amazon River Basin will also be we - Flooding

rain fell along the lower Queensland and upper New South Wales coast of Australia Friday into Sunday morning - Rain

totals of 4.00 to more than 14.00 inches was common with local totals to more than 39 inches occurring in Gympie - Brisbane

International airport reported 25.00 inches of rain - Flooding

resulted and damage to infrastructure and personal property was greatest from south of the Hervey Bay area along the Sunshine Coast, Brisbane and Gold coast areas extending to the west a short distance - Some

sugarcane, cotton and sorghum areas were impacted much of the serious flooding occurred in the urban areas near the coast - Most

of the heaviest rain is over, but follow up showers are expected later this week and into next week slowing the drying rates - Some

additional rain of significance fell between 0001 GMT and 1200 GMT today - Flooding

rain also fell in the lower Malay Peninsula from northeastern portions of peninsular Malaysia into lower portions of the Malay Peninsula in Thailand during the weekend - Rain

totals through 0001 GMT Today (Sunday) varied from 6.85 to 8.19 inches - Some

crop and property damage may have resulted - The

greatest rainfall has since abated - Timor,

Indonesia reported heavy rain during the weekend with over 7.00 inches resulting near Kupang - Tropical

cyclone Anika moved across the north coast of Northern Territory, Australia during the weekend producing some heavy rain and the storm will continue to produce additional heavy rain in the region early this week - A

tropical disturbance near the northwest coast of Sumatra will become better organized this week as it moves toward Sri Lanka and the lower east coast of India

- Landfall

is possible near the Tamil Nadu/Andhra Pradesh border late this week producing some heavy rainfall

- Eastern

parts of Sri Lanka and the lower Andhra Pradesh coast into northeastern Tamil Nadu will receive 3.00 to more than 8.00 inches of rain - Other

areas of India are not likely to get much precipitation in the next ten days except in the far Eastern States and in the extreme north where some significant moisture is possible - Southeast

Asia rainfall will occur frequently and abundantly this week - Flooding

may impact southern and east-central parts of the Philippines, northwestern Sumatra, parts of peninsula Malaysia and in a few western Java locations - Mainland

areas of Southeast Asia will see abundant showers and thunderstorms later this week and next week as pre-monsoonal moisture begins early and aggressively - The

moisture will be good for immature winter crops and for prepping the soil for spring planting of corn, rice and other crops - Interior

eastern Australia will not be bothered by much precipitation during the next five days, but rain may evolve in eastern Queensland and northeastern New south Wales this weekend into next week - The

moisture will be good for late season dryland crops while briefly disrupting early season summer crop maturation and harvesting - Ghana

and Ivory Coast will receive greater amounts of rain this week easing recent dryness and improving the soil for coffee, and cocoa flowering - Greater

rain will still be needed in interior Nigeria and interior Cameroon as well as some Benin locations - North

Africa rainfall this week will be greatest in north-central and northeastern Algeria and parts of Tunisia, although a few showers will occur in Morocco and northwestern Algeria as well - Some

rain was noted Sunday and early today in Algeria and immediate neighboring areas of Morocco and Tunisia - Amounts

varied from 0.20 to 1.14 inches in Algeria; including the drier areas in the northwest while Morocco and Tunisia rainfall was lighter - No

drought busting rain is expected in the driest areas of Morocco - The

moisture will be welcome to wheat and barley and it should stimulate new growth in northeastern and north-central Algeria and northern Tunisia where 0.50 to more than 2.00 inches will result - Morocco

and northwestern Algeria rainfall will not be more than 0.75 inch through the first half of next week - A

big part of Europe will not be bothered by significant precipitation this week - Rain

is expected from northern and eastern Spain through western and far southern France to the U.S. and in a few southern Balkan country locations - Central

and eastern Turkey will become wettest this week with additional rain and mountain snow expected

- Some

of the moisture will also impact northern Iraq and northern and western Iran wheat and cotton areas - Russia’s

Southern Region, northwestern Kazakhstan and the southern and eastern Russia New Lands will get moisture this week from snow and rain

- The

precipitation will help improve spring planting conditions when seasonal warming arrives in April and May - More

moisture will be needed - Xinjiang,

China precipitation will continue restricted over the next ten days, although a few showers of rain and snow are expected - The

mountainous areas in the west will be wettest - China’s

most frequent and significant precipitation in the next ten days will be near and south of the Yangtze River where the ground will continue saturated or nearly saturated with moisture - Waves

of light snow will fall across China’s Northeast Provinces - Winter

wheat and rapeseed will remain dormant or semi-dormant and in mostly good condition - Additional

warming is needed in the south to improve planting conditions for rice and corn and to stimulate sugarcane development - Not

much moisture occurred during the weekend - Winter

crops are still dormant or semi-dormant and poised to perform well in the early spring - South

Africa will experience a good mix of rain and sunshine for late season crop development - Summer

crop conditions are still rated quite favorably. - East-central

Africa precipitation has been and will continue to be most significant in Tanzania which is normal for this time of year.

- Ethiopia

is dry biased along with northern Uganda and that is also normal - Today’s

Southern Oscillation Index is +8.61 - The

index will move erratically this week - NOAA’s

ENSO model is still predicting La Nina through spring and possibly all summer in the Northern Hemisphere - Confidence

in the longer range outlook is low except in the statistical studies showing La Nina events in other 22-year solar cycle years like this persist longer than any other time

- Mexico

will experience seasonable temperatures and a limited amount of rainfall during the coming week - Central

America precipitation will be greatest along the Caribbean Coast during the next seven to ten days and in both Panama and Costa Rica - Guatemala

will also get some showers periodically

Source:

World Weather Inc.

Bloomberg

Ag Calendar

- USDA

export inspections – corn, soybeans, wheat, 11am - Ivory

Coast cocoa arrivals - Malaysia’s

Feb. 1-20 palm oil export data - Vietnam

General Statistics office releases Feb. coffee, rice, rubber export data - U.S.

agricultural prices paid, received, 3pm - EARNINGS:

Olam, FGV - HOLIDAY:

Brazil, Indonesia

Tuesday,

March 1:

- EU

weekly grain, oilseed import and export data - USDA

soybean crush, corn for ethanol, DDGS output, 3pm - U.S.

Purdue Agriculture Sentiment - Australia

Commodity Index - New

Zealand dairy trade auction - EARNINGS:

Golden Agri Resources - HOLIDAY:

Brazil, Argentina, India, South Korea

Wednesday,

March 2:

- EIA

weekly U.S. ethanol inventories, production, 11am - Winter

Grain conference in Siberia

Thursday,

March 3:

- FAO

Food Price Index - USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - New

Zealand Commodity Price - HOLIDAY:

Indonesia

Friday,

March 4:

- ICE

Futures Europe weekly commitments of traders report, ~1:30pm - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions

Source:

Bloomberg and FI

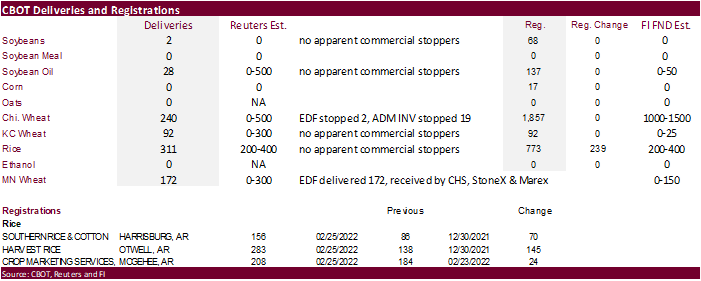

First

Notice Day Deliveries

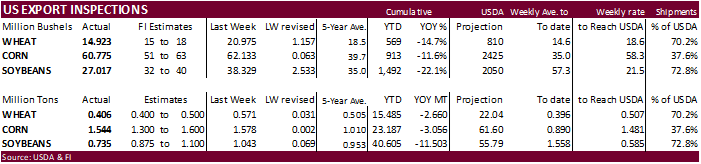

USDA

inspections versus Reuters trade range

Wheat

406,138 versus 300000-625000 range

Corn

1,543,751 versus 1000000-1700000 range

Soybeans

735,278 versus 500000-1100000 range

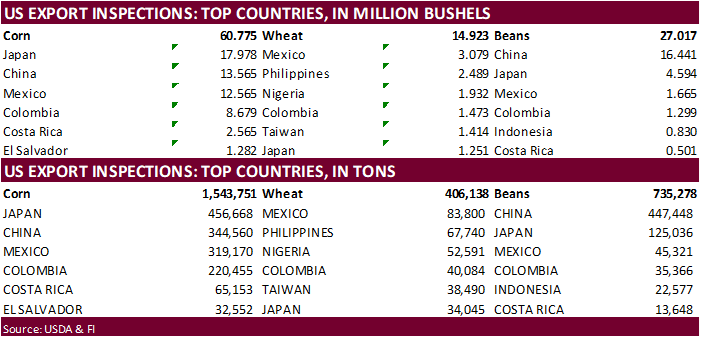

GRAINS

INSPECTED AND/OR WEIGHED FOR EXPORT

REPORTED IN WEEK ENDING FEB 24, 2022

— METRIC TONS —

————————————————————————-

CURRENT PREVIOUS

———–

WEEK ENDING ———- MARKET YEAR MARKET YEAR

GRAIN 02/24/2022 02/17/2022 02/25/2021 TO DATE TO DATE

BARLEY

0 0 2,395 10,010 31,023

CORN

1,543,751 1,578,256 2,046,712 23,186,788 26,243,105

FLAXSEED

0 0 0 324 509

MIXED

0 0 0 0 0

OATS

0 0 224 400 3,017

RYE

0 0 0 0 0

SORGHUM

146,516 258,590 121,151 3,021,080 3,586,096

SOYBEANS

735,278 1,043,138 1,005,915 40,605,038 52,108,537

SUNFLOWER

0 0 0 432 0

WHEAT

406,138 570,859 343,005 15,484,880 18,144,764

Total

2,831,683 3,450,843 3,519,402 82,308,952 100,117,051

————————————————————————–

CROP

MARKETING YEARS BEGIN JUNE 1 FOR WHEAT, RYE, OATS, BARLEY AND

FLAXSEED;

SEPTEMBER 1 FOR CORN, SORGHUM, SOYBEANS AND SUNFLOWER SEEDS.

INCLUDES

WATERWAY SHIPMENTS TO CANADA.

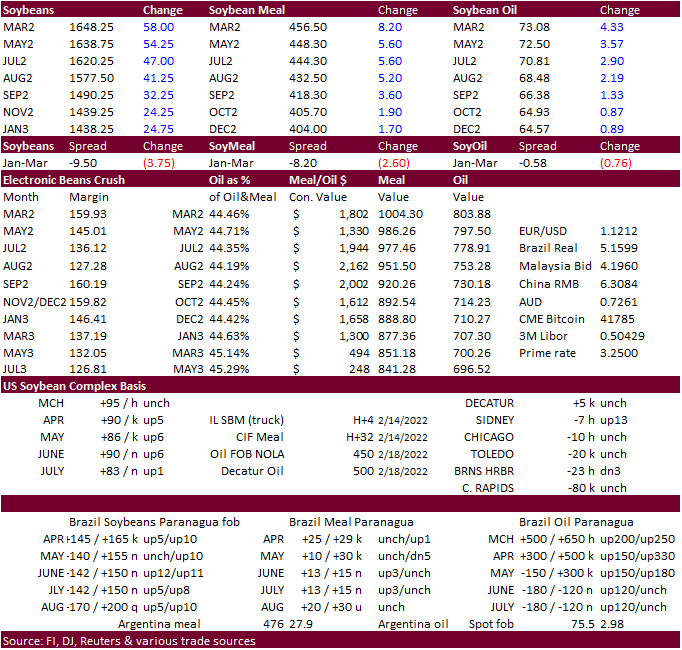

Soybean

and Corn Advisory

2021/22

Brazil Soybean Estimate Unchanged at 124.0 Million Tons

2021/22

Argentina Soybean Estimate Unchanged at 39.0 Million Tons

2021/22

Paraguay Soybean Estimate Unchanged at 5.0 Million Tons

2021/22

Brazil Corn Estimate Unchanged at 112.0 Million Tons

2021/22

Argentina Corn Estimate Unchanged at 49.0 Million Tons

Macros

US

Wholesale Inventories (M/M) Jan P: 0.8% (est 1.2%; prev 2.2%)

US

Advance Goods Trade Balance Jan: -$107.6Bln (est -$99.3Bln; prev -$101.0Bln; prevR -$100.5Bln)

US

Retail Inventories (M/M) Jan:1.9 % (prev 4.4%)

Canadian

Industrial Product Price (M/M) Jan: 3.0% (est 1.0%; prev 0.7%)

82

Counterparties Take $1.596 Tln At Fed Reverse Repo Op (prev $1.603 Tln, 77 Bids)

Corn

·

CBOT corn futures

reached limit higher on renewed bullish sentiment from Black Sea shipping concerns. We understand peace talks today did not go well. Strength in wheat and higher outside related commodity markets also underpinned the market. WTI crude oil was up around $4/barrel

higher at the time this was written.

·

Funds bought an estimated net 33,000 corn contracts.

·

May corn was the only contract to close up 35 cents so no expanded limits for Tuesday.

·

We last heard May corn synthetic was $6.9175.

·

Look for $7+ corn soon. Our top end of a range for the May contract is $7.50, up 25 cents from previous.

·

China plans to buy 40,000 tons of pork for state reserves this week to help support falling prices. 19,400 tons will be bought Thursday and another 20,600 tons Friday. Late last week China reported end of January sow herd fell

0.9% from the previous month to 42.9 million head and is 2% above year ago. Pigs slaughtered were 28.47 million heads, down 1.7% from the previous month and up 45.9% from year ago.

·

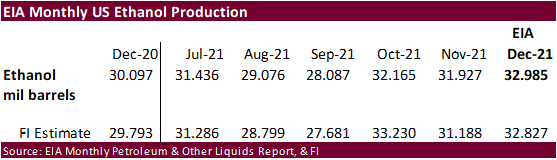

US December ethanol production came in near our expectations.

Export

developments.

- None

reported

Updated

2/28/22

May

corn is seen in a $6.50 and $7.50 range

December

corn is seen in a wide $5.50-$7.25 range

·

CBOT May soybeans ended

sharply higher in part to strength in soybean oil. CBOT crush started higher but closed 4 cents lower basis the May contract. Black Sea shipping is still closed. Funds bought an estimated net 22,000 soybean contracts, bought 4,000 meal and bought 14,000 soybean

oil.

·

Soybean oil was 359 points higher basis the May and July up 288 points. Strong December US domestic soybean oil use and sharply higher WTI crude oil along with a rally in palm oil

·

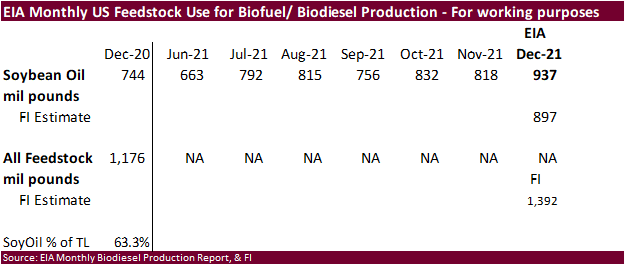

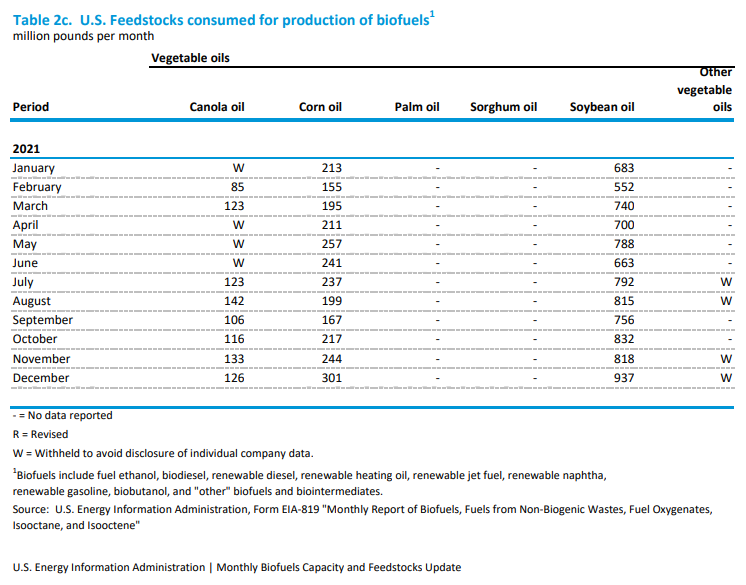

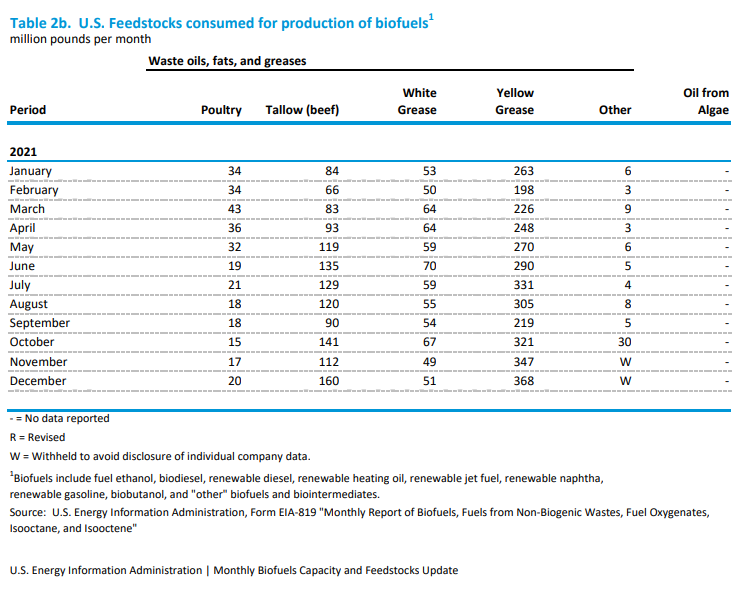

EIA reported an exceptionally large soybean oil for biofuel use for the month of December of 937 million pounds, well up from 818 million during November and 744 million December 2020. Corn oil and grease use was also high during

December (tables below).

·

We raised our soybean oil for US biofuel use from 11.000 billion pounds to 11.025 billion for 2021-22.

·

On Wednesday we will issue updated S&D’s for the US soybean complex, incorporating SBO use and updated NASS crush.

·

News was light outside geological/Black Sea developments.

·

Rain is still needed in northern Argentina and relief will occur this week. Brazil rainfall will be restricted this week in center south and northeastern parts of the nation of 0.20 to 0.75 inch. Brazil rain is expected in far

southern parts of the nation this week with 1.50 to more than 4.00 inches by Saturday.

·

Many South American countries will be on holiday over the next couple of days.

·

Agrual: 44 percent soybeans harvested, up 11 points from previous week.

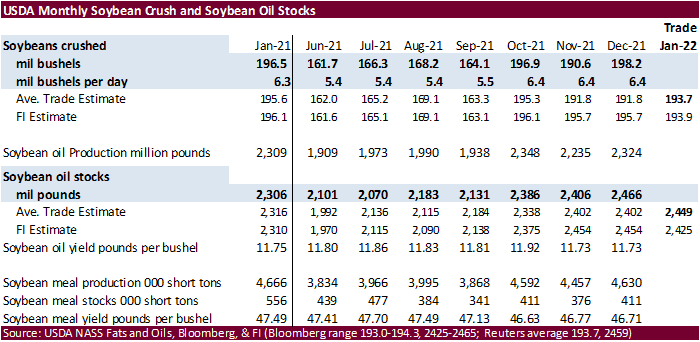

·

USDA NASS will release US January crush Tuesday. A Reuters poll looks for 193.7 million bushels (193.0-194.3 range), down from 198.2 for December and 196.5 million January 2021. End of January stocks are projected at 2.459 billion

pounds (2.425-2.498 billion range), down from 2.466 billion at the end of December and up from 2.306 billion at the end of January 2021.

·

AmSpec reported February Malaysian palm exports at 1.211 million tons.

·

ICE canola was up 3 percent or $31.50 to $1,032.70/ton.

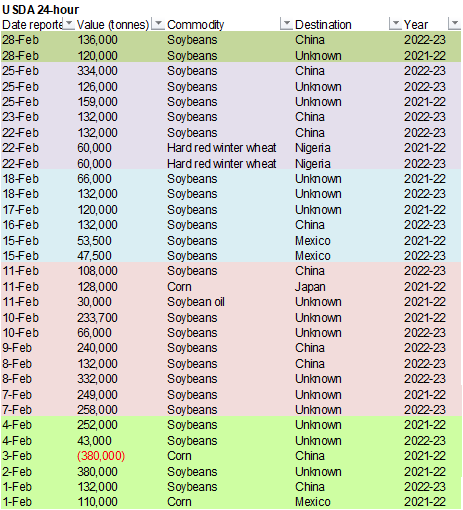

- Private

exporters reported the following activity:

-136,000

metric tons of soybeans for delivery to China during the 2022/2023 marketing year

-120,000

metric tons of soybeans for delivery to unknown destinations during the 2021/2022 marketing year

- Results

awaited: Iran’s SLAL seeks up to 60,000 tons of soybean meal and 60,000 tons of feed barley for an unknown shipment period.

Updated

2/24/22

Soybeans

– May $15.00-$18.00

Soybeans

– November is seen in a wide $12.50-$16.00 range

Soybean

meal – May $425-$520

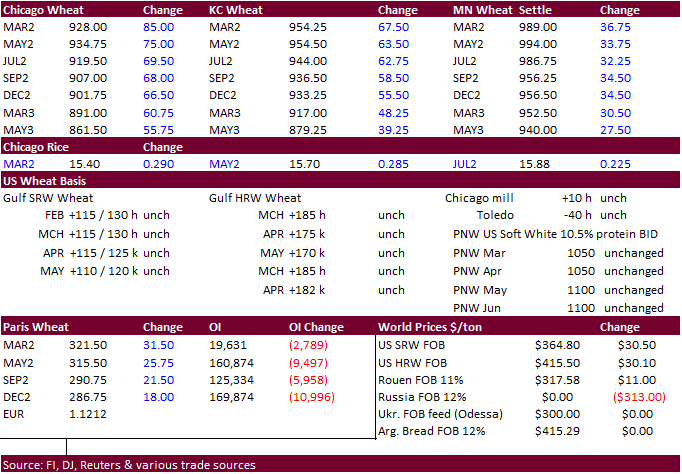

·

Black Sea concerns again supported US wheat futures, up more than 70 and 60 cents for the May Chicago and KC wheat contracts, respectively. MN wheat lagged HRW and SRW type wheat, ending up 33.75 cents for the May position. May

Chicago is still below its absolute contract high made during the overnight session Thursday into Friday. But new highs are not out of the question this week if Russia/Ukraine conditions fail to improve.

·

Funds bought an estimated net 28,000 contracts.

·

Egypt passed on wheat. Only three offers were presented. Normally you see about 15-20. Mid-February they bought wheat at $338.55/ton c&f. Today

lowest

offer was $389.92/ton.

·

Egypt can afford to sit back and wait. They have enough wheat to last 4 months. There are 14 approved countries Egypt could import wheat from, some of which are outside Europe, according to Reuters.

·

The Russian Ruble plunged today after many countries imposed sanctions.

·

US hard red winter wheat areas will turn warmer this week. Little precipitation will occur over the next week in the central or southwestern Plains.

·

While the Black Sea remains closed, CME Black Sea wheat is still trading. Today 1,010 lots turned over.

·

Paris May wheat closed up 25.75 euros, or 8.8%, at 315.50 euros ($353.61) a ton. 341.75 euros was the all-time high.

·

China sold 522,037 tons of wheat out of auction at an average price of 2,753 yuan per ton.

·

Egypt passed on wheat. Only three offers were presented,

for

April 13-26 shipment for payment at sight. Normally

you see about 15-20 offers. Mid-February they bought wheat at $338.55/ton c&f. Today

lowest

offer was $389.92/ton. One offer from the US was presented.

·

Algeria seeks 50,000 tons of durum wheat on Wednesday, open until Thursday, for April shipment.

·

Jordan seeks 120,000 tons of feed barley on March 1.

·

Turkey seeks 435,000 tons of milling wheat on March 2 for March-April shipment.

·

Jordan seeks 120,000 tons of wheat on March 2.

Rice/Other

·

Results awaited: South Korea seeks 72,200 tons rice from U.S. and Vietnam on Feb. 25.

Updated

2/24/22

Chicago

May $8.00 to $10.50 range

KC

May $8.25 to $10.75 range

MN

May $9.25‐$11.50

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.