PDF Attached

USDA

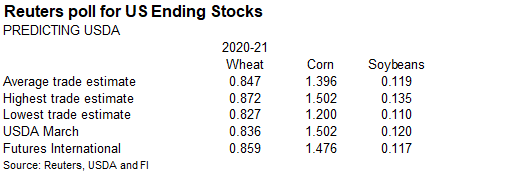

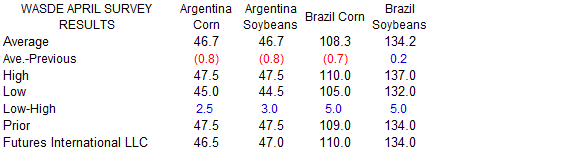

S&D is this Friday

Attached

is our convenience table & updated US soybean product tables

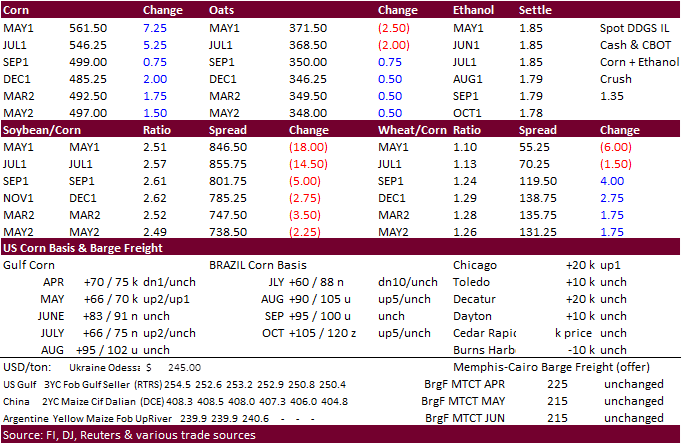

Changes

to US soybean complex:

-

Meal

exports 14.150 mil short tons to 14.100 -

Soybean

imports 33 mil bu to 29 -

Meal

imports 602,000 short tons to 589,000

![]()

No

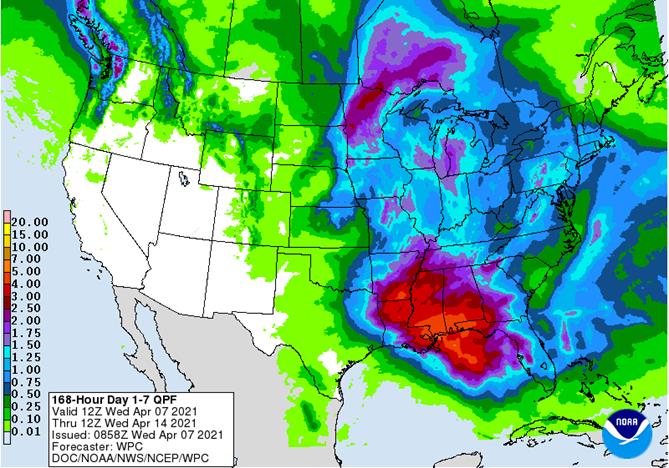

major changes to weather conditions across the world. U.S. hard red winter wheat area precipitation prospects are improving. The northern Plains could see precipitation in the last ten days of this month. Ongoing dry conditions in interior southern Brazil

is of concern for second crop corn. Europe will turn colder but there is no threat to crops.

World

Weather Inc.

CHANGES

OVERNIGHT

- Tropical

Cyclone Seroja (26S) has will move inland through Western Australia Sunday near Geraldton and will bring some welcome moisture to wheat, barley and canola areas for use later this month when planting begins - The

European Model increased precipitation in the west-central and southwestern U.S. Plains next week like the GFS model run was suggesting Tuesday and overnight - The

moisture boost will improve wheat in the high Plains region after recent very warm to hot temperatures and net drying conditions - World

Weather, Inc. sees improving rain potentials in the northern Plains and southwestern Canada’s Prairies after April 20

MOST

IMPORTANT WEATHER IN THE WORLD

- Frost

and freezes in Europe and anticipated colder biased weather for a while will not harm winter wheat, barley, rye or rapeseed, but warming is needed to get crop development to occur more aggressively - Rain

and snow across the continent will increase soil moisture for use by crops during the warmer days of late April and May - CIS

grain and oilseed areas will continue plenty moist except in Russia’s Southern Region and Kazakhstan where there is need for more moisture this spring and summer - Winter

crops are still dormant or semi-dormant, although a little greening may be occurring in the far south - Northwestern

U.S. Plains and Canada’s Prairies will continue dry biased and in need of significant moisture; not much relief is expected for a while, but possibly after April 20 for some areas - Light

rain and snow will impact Manitoba and eastern Saskatchewan briefly this weekend into early next week - U.S.

Delta will be too wet for cotton, corn and early soybean planting today into Saturday, but there will be time for improvement - Some

flooding is expected - U.S.

Southeastern States will experience a good mix of weather over the next two weeks supporting early-planted crop development and future planting as well - U.S.

west-central and southwestern Plains are drying down and this process will continue until mid- to late-week next week when some computer forecast model runs have been suggesting improved rain potential - World

Weather, Inc. believes the advertised rain may be overdone - Central

Washington into Central Oregon is too dry and needs rain for unirrigated crops - California

and the southwestern desert region will remain dry and in need of significant moisture, but irrigation is sufficient to carry on most agricultural needs - No

relief is expected in the coming week, but some showers may occur in a part of the region in the April 12-19 period - Brazil’s

Mato Grosso and Goias will experience well-timed rainfall and seasonable temperatures to support Safrinha corn and cotton during the next two weeks - Brazil’s

interior south and center south will dry down for another week to ten days - Many

areas have short to very short topsoil moisture, but subsoil moisture will carry on normal crop developing for a while longer, although it is rated marginally adequate to slightly short - A

boost in precipitation will be very important during the second week of the outlook and into the second half of this month - Some

of that moisture boost is expected, but a close watch is warranted for fear that the rain fails to develop - Argentina

will get generalized rainfall the remainder of this week and into the weekend bolstering topsoil moisture once again and supporting great late season corn, sorghum, peanut and soybean development - Mainland

areas of Southeast Asia will experience a net boost in precipitation soon that will further improve corn planting conditions and maintain an improving trend in sugarcane, rice and coffee production areas - Some

beneficial rain fell across parts of this region recently, but southern areas are still dry - Philippines

weather is good for most crops, but a boost in rainfall would be welcome - Indonesia

and Malaysia crop weather is expected to be mostly good for the next ten days to two weeks with most areas getting rain - Flooding

in Timor and Flores is abating after serious crop and property damage occurred during the weekend from a developing tropical cyclone - At

0900 GMT, Tropical Cyclone Seroja was located 510 miles north northeast of Learmonth, Western Australia at 14.55 south, 116.3 east moving southwesterly at 17 mph and producing maximum sustained wind speeds of 52 mph - The

storm will move inland near Geraldton, Western Australia Sunday producing heavy rain and strong wind speeds along the coast - Beneficial

moisture will fall in wheat, barley and canola production areas of Western Australia where planting will begin late this month - India

weather will continue good for this time of year with restricted rainfall and warm temperatures supporting winter crop maturation and harvest progress - Rain

may fall heavily in Bangladesh and neighboring areas of India briefly next week - China

weather remains mostly very good, although portions of the Yangtze River Basin are too wet and need to dry down - Northern

crop areas in China are favorably moist and poised to support aggressive winter and spring crop development this year once additional warming takes place - Western

Europe will continue to dry down through Thursday raising the need for rain - Temperatures

will be very warm early this week and then cool later this week and during the weekend as precipitation begins to evolve - Precipitation

will be erratic and somewhat light late this week and into the weekend, but all of it will be welcome - Next

week trends drier once again and some warming is expected - Cold

weather in Europe is of little concern, despite slowing winter crop development and further delaying the planting of some spring crops - CIS

precipitation over the next two weeks will be frequent - Sufficient

amounts will occur while snow is melting in northern and central Russia to maintain muddy fields in snow free areas and high river and stream flows - Drier

and warmer weather is needed for most winter crops and for advancing early spring planting - Greening

winter crops is occurring mostly in southern Ukraine and southern parts of Russia’s Southern Region - Most

interior crop areas of Australia will not be bothered by significant rain this week - Rain

in Western Australia late this weekend and early next week will be dependent upon the tropical cyclones noted above

- Good

drying conditions are likely in key summer grain, oilseed and cotton areas in Eastern Australia this week favoring summer crop maturation and good harvest progress. - North

Africa will experience a favorable mix of weather over the next ten days, although resulting rainfall is not likely to be very great - All

of the moisture will be welcome, but resulting amounts may be a little erratic and light leaving need for more moisture - Northwestern

Algeria and southwestern Morocco need rain - Temperatures

will be near to above average - West-central

Africa coffee and cocoa weather has been very good recently and that is not likely to change much for a while; some rice and sugarcane has benefited from the pattern as well - Rainfall

will be a little lighter and less frequent than usual over the next ten days, but crop conditions should remain favorable - Temperatures

have been and will continue to be very warm keeping evaporation rates very warm - East-central

Africa rainfall has been erratic recently and a boost in precipitation should come to Ethiopia this month while Tanzania slowly begins to dry down - South

Africa weather will continue favorably for early maturing summer crops and the development of late season crops - Net

drying is expected for a while which will support faster crop maturation and will eventually support early season harvest progress - Temperatures

will be warmer than usual and that will dry out the soil relatively quickly - New

Zealand weather has been drier than usual and precipitation will slowly improve during the next ten days in both North Island and western parts of South Island - Temperatures

will be seasonable - Canada’s

Prairies will receive restricted amounts of precipitation for the next ten days - Temperatures

will trend cooler than usual for a while this weekend and early next week.

- Southeastern

Canada will see below average precipitation and warmer than usual temperatures over the next ten days - Southern

Oscillation Index this morning was +0.47 and the index is expected to move in a narrow range the rest of this week

Source:

World Weather inc.

Bloomberg

Ag Calendar

Wednesday,

April 7:

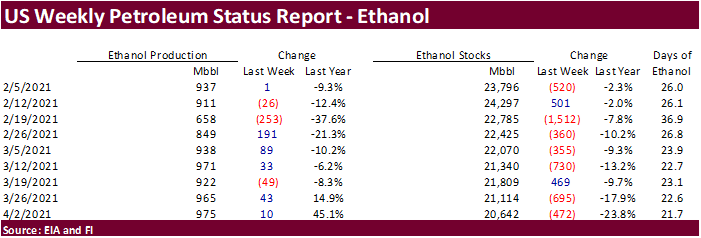

- EIA

weekly U.S. ethanol inventories, production - ANZ

Commodity Price

Thursday,

April 8:

- FAO

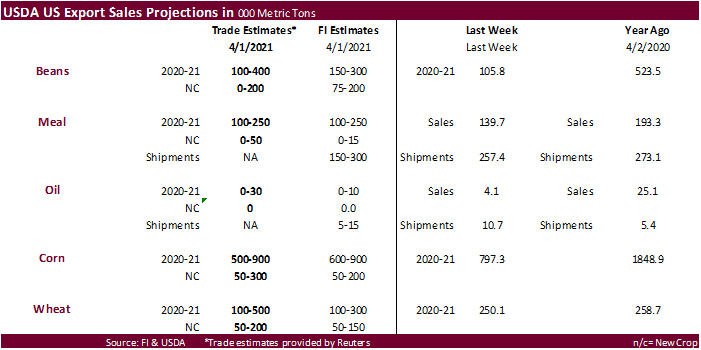

World Food Price Index - USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - China’s

CNGOIC to publish soybean and corn reports - Conab’s

data on yield, area and output of corn and soybeans in Brazil - Port

of Rouen data on French grain exports

Friday,

April 9:

- USDA’s

monthly World Agricultural Supply and Demand (WASDE) report, noon - ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions

Source:

Bloomberg and FI

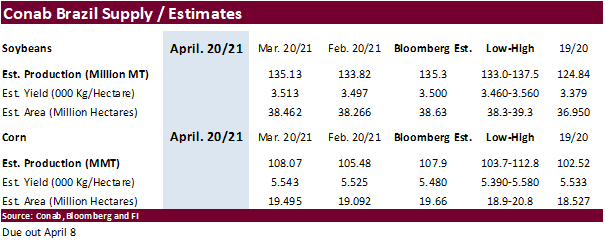

Conab

is due out with April Brazil supply on April 8

Macro

US

DoE Crude Oil Inventories (W/W) 02-Apr: -3522K (est -2000K; prev -876K)

–

Distillate Inventories: 1452K (est 1000K; prev 2542K)

–

Cushing OK Crude Inventories: -735K (prev 782K)

–

Gasoline Inventories: 4044K (est -600K; prev -1735K)

–

Refinery Utilization: 0.10% (est 0.75%; prev 2.30%)

Corn

- Corn

ended higher on bull spreading

and fund positioning. Weekly US ethanol data was positive. Good US shipment demand prospects for this summer and second crop Brazil corn crop concerns underpinned prices. Traders are banking on a roughly 125 million bushel decrease to US 2020-21 corn ending

stocks on Friday. This would be bullish if realized, IMO, as we expect USDA to reduce feed and ethanol that could offset a large increase in exports.

- The

USDA Attaché sees 2021-22 Brazil corn production at 114 million tons. They are at 105 million tons for 2021-21. USDA official is at 109 million tons for the 2020-21 Brazil corn crop, versus 102 million for 2019-20.

- Funds

on Wednesday bought an estimated net 12,000 corn contracts.

- Weekly

ethanol production increased 10,000 barrels per day to 975,000 (trade looking for 3,000 decrease) and stocks were off 472,000 barrels (trade looking for up 55,000) to 20.642 million. This is the lowest stocks figure since November 13 and highest weekly ethanol

production since December 18. September 2020 year to date ethanol production is still running 9.2% below the same period a year ago. Gasoline demand fell 110,000 barrels from the previous week. We are using 4.940 billion for corn for ethanol use, 10 million

below USDA.

Export

developments.

- None

reported

May

corn is seen in a $5.40 and $6.00 range

July

is seen in a $5.25 and $6.00 range

December

corn is seen in a $3.85-$5.50 range.

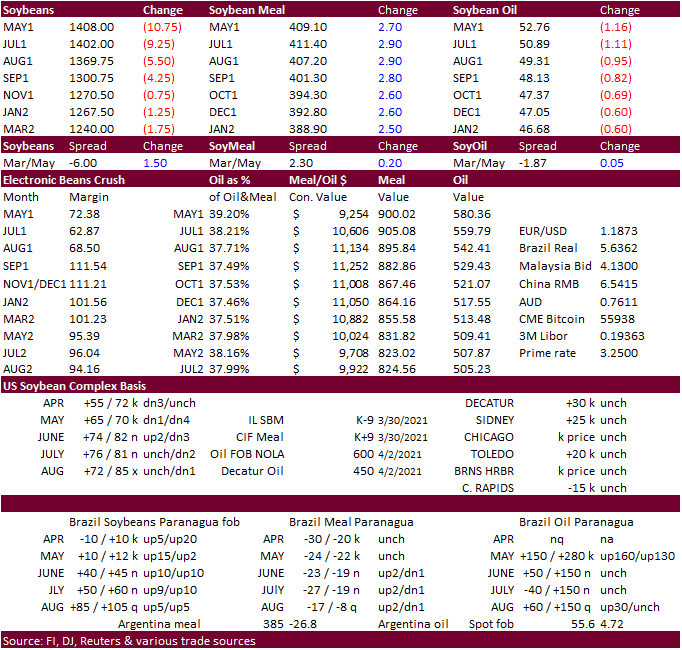

- CBOT

soybeans started higher with light bull spreading but turned lower as soybean oil prices declined more than 100 points. Positioning ahead of USDA’s S&D was noted. Reversal in soybean / corn spreading added to the bearish undertone.

- USDA’s

Attaché projected bearish Brazil corn and soybean production prospects for new crop. Soybean meal was higher on a reversal in product spreading.

- Early

during the trade, we heard that Brazil may lower its biodiesel blending mandate, for around a couple months, and later a Brazil biodiesel tender might be cancelled. The short term mandate adjustment will likely have little impact on global soybean oil trade

flows. - The

USDA Attaché released an initial 2021-22 Brazil soybean production estimate of 141 million tons due in part to a 1.5 million hectare increase in area. 2021-22 exports were projected at 87 MMT vs. 85MMT for the current year. They are at 134 million tons output

for 2021-21, same as USDA official. https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Oilseeds%20and%20Products%20Annual_Brasilia_Brazil_04-01-2021

- Funds

on Wednesday sold an estimated net 5,000 soybean contracts, bought 2,000 soybean meal and sold an estimated 5,000 soybean oil.

- Russia

approved their formula-based sunflower oil export tax. - Expect

US soybean shipments to China to continue to slow. Brazil exported a record 13.5 million tons of soybeans during the month of March, up nearly 25 percent from the same month year ago. April shipments were seen increasing to 16.3 million tons (ANEC). Range

of (most) estimates for Brazil’s 2020-21 soybean crop are from 133 to 138 million tons.

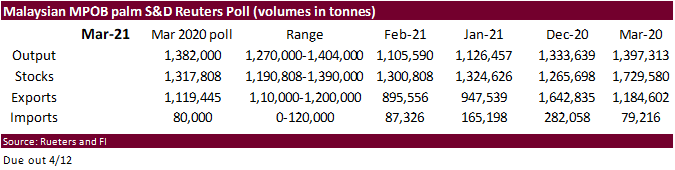

- Delayed

March Malaysian palm shipment data by SGS showed March palm shipments up 18.3% to 1.25MMT from February.

India:

Oilseeds and Products Annual

Pakistan:

Oilseeds and Products Annual

- None

reported

A

Reuters poll for Malaysia’s palm oil inventories shows March stocks expected to rise 1.3% from February to 1.32 million tons, production to slightly decline, and exports to be up 25% to 1.12 million tons. The Malaysian Palm Oil Board will release the official

data on April 12.

May

soybeans are seen in a $13.75 and $15.75 range.

November $10.50-$14.50

May

soymeal is seen in a $395 and $425 range.

December $325-$5.00

May

soybean oil is seen in a 50 and 55 cent range

December 40-60 cent wide range

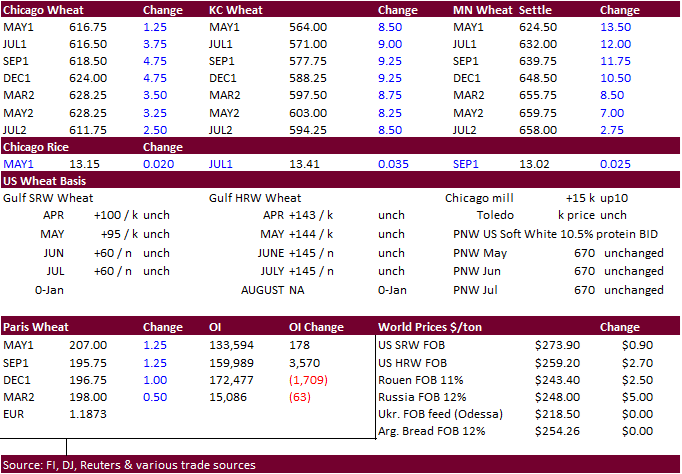

- Chicago

wheat ended

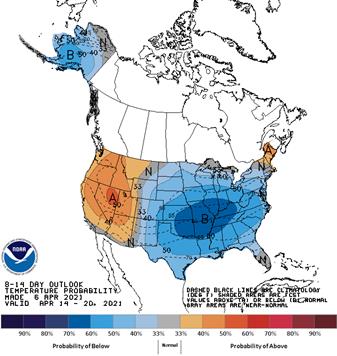

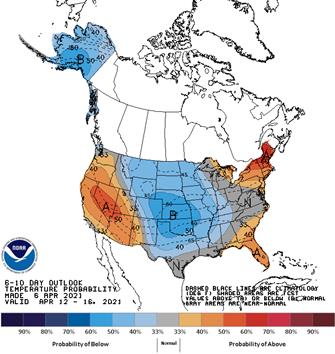

higher in part to talk of delayed US spring wheat planting progress, lower USD earlier, and increase in global import demand. Dry weather across the northern Great Plains and cold weather forecast during the 6-10 day and 8-14 day weather maps may hinder seeding

progress over the next two weeks. Japan and Tunisia announced import tenders. Thailand passed on a half million tons of wheat and Algeria bought a small amount of wheat.

- Funds

on Wednesday bought and estimated net 2,000 CBOT SRW wheat contracts. - May

milling wheat settled 1.50 euros higher, or 0.7%, at 207.25 euros ($246.23) a ton.

- Algeria’s

OAIC bought between 30,000 and 48,000 tons of optional milling wheat at around $280 a ton c&f, up $1.00 from what they paid last week.

- Tunisia

seeks 75,000 tons of optional origin soft wheat on April 8 for May 15 and June 25 shipment.

- Thailand’s

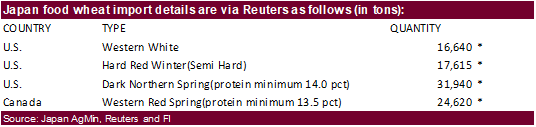

TFMA group passed on 504,000 tons of animal feed wheat due to high prices for shipment between May and December. Offers were said to range from just below $268 to $290 a ton c&f. - Japan

seeks 90,815 tons of food wheat this week from the US and Canada for June loading.

- Taiwan

seeks 96,485 tons of US wheat on April 8. - Ethiopia

seeks 30,000 tons of wheat on April 16. - Jordan

postponed their 120,000 ton import tender of animal feed barley from April 6 to April 13.

- Ethiopia

seeks 400,000 tons of optional origin milling wheat, on April 20, valid for 30 days. In January Ethiopia cancelled 600,000 tons of wheat from a November import tender because of contractual disagreements.

Rice/Other

·

Mauritius seeks 4,000 tons of optional origin long grain white rice on April 16 for delivery between June 1 and July 31.

·

Syria seeks 39,400 tons of white rice on April 19. Origin and type might be White Chinese rice or Egyptian short grain rice.

·

Ethiopia seeks 170,000 tons of parboiled rice on April 20.

Updated

4/7/21

May Chicago wheat is seen in a $6.00‐$6.65 range

May KC wheat is seen in a $5.50‐$6.00 range

May MN wheat is seen in a $6.00‐$6.50 range (up 10, up 10)

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.