PDF Attached does not have daily estimate of funds.

Risk

off trading today in commodities, with energy markets sharply lower. The soybean complex closed mixed and grains lower. We remain bullish agriculture commodities based on ongoing Black Sea concerns and improving soybean and corn export demand. US wheat export

demand has yet to improve as fob cash prices are above the world market.

EARLY

MORNING WEATHER UPDATE

For

Tuesday, April 19, 2022

WEATHER

EVENTS AND FEATURES TO WATCH

- Net

drying continues to be advertised in much of Mato Grosso, northern Mato Grosso do Sul and areas east to southern Bahia, Minas Gerais and Sao Paulo - Topsoil

moisture is already rated short in Mato Grosso and central Bahia while short to very short in northern Minas Gerais.

- Subsoil

moisture is rated marginally adequate in Mato Grosso and short to very short from northeastern Goias to southern Bahia and northern Minas Gerais - Ten

days of drying will result in crop moisture stress for Mato Grosso and a few neighboring areas and that could harm production potentials for Safrinha corn and cotton - Some

negative impact is also possible for minor grain and oilseed production areas in Bahia and northern Minas Gerais, although some of these areas received rain during the weekend - Rain

must develop soon to prevent dryness during reproduction from cutting into yield potentials.

- Southern

Brazil will get periods of rain from late this week through next week - Resulting

precipitation will be sufficient to maintain moisture abundance in the region which may slow some farming activity at times - Argentina

experienced net drying over the past several days and similar conditions are expected today - Argentina

will get rain Wednesday and Thursday and again early next week in the eastern most parts of the nation.

- Western

most crop areas are unlikely to receive much rain for a while - Frequent

rain will fall from the Amazon River Basin through Ecuador, Colombia and western Venezuela maintaining moisture abundance in those areas - Some

heavy rain and flooding will be possible - West

Texas rain potentials may slowly improve over the next ten days to two weeks.

- Multiple

frontal passages are expected and some of them will be over the region long enough to stimulate a few showers and a couple of thunderstorms eventually - Initial

rainfall cannot be very great because of low humidity and dry air, but over time the potential for rain might improve - No

general soaking is presently anticipated - South

Texas rainfall will be restricted as well, but 0.20 to 0.75 inch of moisture will be possible next week which is not enough to adequately moisten the soil in dryland areas - U.S.

High Plains region from Nebraska to Western Texas will not be absolutely dry during the next ten days, but resulting rainfall is unlikely to counter evaporation and ne - U.S.

Northern Plains and eastern Canada’s Prairies will be facing additional storm systems maintaining a wet bias and further raising the potential for planting delays - Snow

and rain will return briefly tonight and Wednesday in the eastern Dakotas to Minnesota as well as in Manitoba, Canada - Moisture

totals will vary from 0.05 to 0.35 inch with local amounts of 0.50 to 1.00 inch in Minnesota

- Several

inches of snow will fall in Manitoba - Other

areas in Canada’s Prairies will get precipitation today and Wednesday favoring the central and northern areas with accumulations of 3 to 10 inches - A

much larger storm system is expected in the northern Plains and eastern parts of the Canadian Prairies Thursday into Sunday producing 0.20 to 0.75 inch with local totals of 1.00 to 1.50 inches

- Interior

eastern South Dakota will be an exception with less than 0.20 inch of moisture likely - Some

very heavy snow is expected in western North Dakota, eastern Montana, southeastern Saskatchewan and Manitoba with accumulations of 5 to 16 inches possible - There

is of time for change on this event and it will be closely monitored - There

may be a couple of additional storm systems in the northern Plains at the end of this month - If

all of these disturbances occur in the northern Plains and southeastern Canada’s Prairies will result in some serious delays to farming activity. The flood potential for North Dakota, northern Minnesota and Manitoba Canada will be high as well. A drier and

warmer weather pattern must develop soon. The Red River in Manitoba is already in flood.

- U.S.

Midwest drying conditions will be poor between storm systems through early next week because of a high frequency in precipitation - A

minor amount of field progress is expected, but warmer and drier weather is needed to induce the best possible field progress - Some

warming is expected in the U.S. Midwest during the second half of this week - Temperatures

will rise into the upper 60s and 70s Fahrenheit Thursday and into the 70s and some 80s Friday and Saturday - The

warmer air will be ideal for stimulating faster drying rates between storm systems, but the succession of storm systems will be relatively high into early next week which may still limit fieldwork and drying time. - The

best planting conditions in the U.S. Midwest will likely occur next week, although temperatures will be trending cooler by that time. - U.S.

Delta and southeastern states will experience some improved weather this week and next week with less frequent precipitation and warmer temperatures

- Planting

progress is expected to slowly improve - Southwestern

U.S. weather will remain dry biased through the next two weeks - Texas

Blacklands precipitation will vary from 0.50 to 1.50 inches and locally more Sunday into Monday; otherwise rainfall is not likely to be very great - Southwestern

Canada’s Prairies will not receive much “significant” precipitation during the next ten days, but a few bouts of very light moisture will occur - Ontario

and Quebec, Canada will see alternating periods of rain and sunshine over the next two weeks supporting abundant soil moisture. - Central

and southern Europe will experience wetter than usual conditions over the next ten days and temperatures may be a little cooler than usual as well - The

environment may slow some spring fieldwork, but some progress is expected - Early

season winter and spring crop development will advance, albeit slowly due to milder than usual conditions - Waves

of rain and some snow in the western CIS will maintain moist field conditions in most of the crop areas west of the Ural Mountains and for some areas to the east as well - Spring

fieldwork will be slower advancing than usual because of the precipitation, wet fields and milder than usual temperatures in many areas - China’s

Yangtze River Basin will see rain develop again late this week and during the weekend before easing a little during the first part of next week.

- The

moisture abundance will be good for long term crop development, but fieldwork could be delayed at times

- Net

drying is expected in China’s Yellow River Basin and North China Plain - Xinjiang,

China precipitation is expected to continue mostly in the mountains, but the precipitation will improve spring runoff potentials in support of better irrigation water supply - Some

rain and snow may impact the far northeast of Xinjiang briefly this weekend through most of next week - India’s

rainfall will be greatest in the far Eastern States this week, although some pre-monsoonal showers and thunderstorms are expected briefly in the south - Good

harvest weather will continue in winter crop areas - Temperatures

will remain warm - Turkey,

Iran and Afghanistan will be the wettest Middle East countries over the next ten days - Rain

is still needed in Syria, Iraq and neighboring areas to the south - Southeast

Asia rainfall is expected to be abundant in Indonesia, Malaysia and Philippines while a little erratic in the mainland crop areas - Overall,

crop conditions will remain favorable - Southern

New South Wales cotton and sorghum areas started to receive rain Monday, and more is expected today into early Wednesday.

- The

moisture may disrupt farming activity and raise some cotton fiber quality concerns - Otherwise,

good crop maturation and harvest weather is expected in summer crop areas during the next week

- South

Africa continues in need of drier weather to protect summer crop conditions and to promote faster crop maturation and harvest progress - Topo

much moisture could harm crop quality - Central

Africa showers and thunderstorms will occur periodically during the next two weeks to support fieldwork and crop development - North

Africa precipitation over the next two weeks will be a little more sporadic and light leading to some net drying - Crop

conditions have remained favorable and are not likely to change much in the next ten days, despite some drying - Mexico’s

winter dryness and drought have been expanding due to poor precipitation resulting from persistent La Nina - Northern

parts of the nation will continue lacking precipitation for an extended period of time - Eastern

and southern Mexico will experience some periodic rainfall over the next two weeks and some soil moisture boosting is expected in eastern parts of the nation - Central

America precipitation will slowly expand northward in the next few weeks - the

moisture will be good for most crops - Today’s

Southern Oscillation Index was +14.53 and it should drift a little higher before leveling off

Source:

World Weather Inc.

Bloomberg

Ag Calendar

- EU

weekly grain, oilseed import and export data - New

Zealand global dairy trade auction - HOLIDAY:

Malaysia

Wednesday,

April 20:

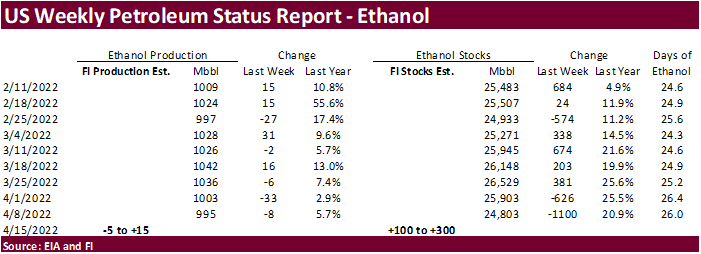

- EIA

weekly U.S. ethanol inventories, production, 10:30am - China’s

third batch of March trade data, including soy, corn and pork imports by country - China

Agricultural Outlook Conference, Beijing - USDA

monthly milk production, 3pm - Malaysia’s

April 1-20 palm oil export data

Thursday,

April 21:

- USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - International

Grains Council monthly report - USDA

red meat production, 3pm - HOLIDAY:

Brazil

Friday,

April 22:

- ICE

Futures Europe weekly commitments of traders report - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - First

quarter cocoa grinding data from Cocoa Association of Asia - Brazil’s

Unica may release cane crush and sugar output data (tentative) - U.S.

cattle on feed; cold storage data for pork, beef and poultry, 3pm - FranceAgriMer

weekly update on crop conditions

Source:

Bloomberg and FI

80

Counterparties Take $1.817 Tln At Fed Reverse Repo Op (prev $1.738 Tln, 82 Bids)

US

Housing Starts Mar: 1793K (est 1740K; prev 1769K)

US

Housing Starts (M/M) Mar: 0.3% (est 1.6%; prev 6.8%)

US

Building Permits Mar: 1873K (est 1820K; prev 1859K; prevR 1865K)

US

Building Permits (M/M) Mar: 0.4% (est -2.4%; prev -1.9%; prevR -1.6%)

·

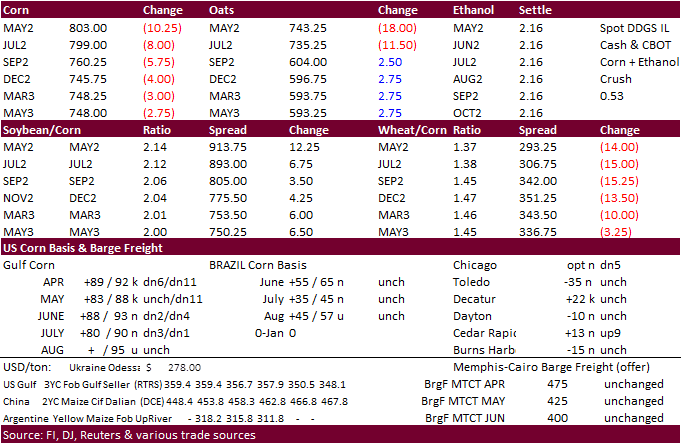

CBOT corn turned lower early in a risk off session as traders took in little fundamental news. Nearby corn hit its highest level since 2012. Weaker energy prices kicked off the selling after the IMF slashed their world growth

outlook. WTI was down around $5.40 as of 12:20 pm CT. Note May WTI crude oil goes off tomorrow and June is front month.

·

July corn traded back below $8.00 today as we saw some consolidation after prices reached multi-decade highs yesterday.

·

Yesterday USDA reported a slower than expected US corn planting progress, but we see fieldwork activity picking up by the end of the workweek with warmer temperatures forecast for the Midwest.

·

Reuters correction: The Baltic Dry index fell 1 percent to 2,115 points, not increase 7 percent as previously reported.

·

Anec: Brazil corn exports for April are seen at only 850,000 tons, unchanged from the previous week.

EIA

expects summer U.S. real gasoline and diesel prices to be the highest since 2014

https://www.eia.gov/todayinenergy/detail.php?id=52098&src=email

Export

developments.

·

China plans to buy pork for state reserves on April 22. 40,000 tons is sought and this would be the 5th state reserve tender.

·

None reported

Updated

4/18/22

May

corn is seen in a $7.75 and $8.55 range

December

corn is seen in a wide $5.50-$8.00 range

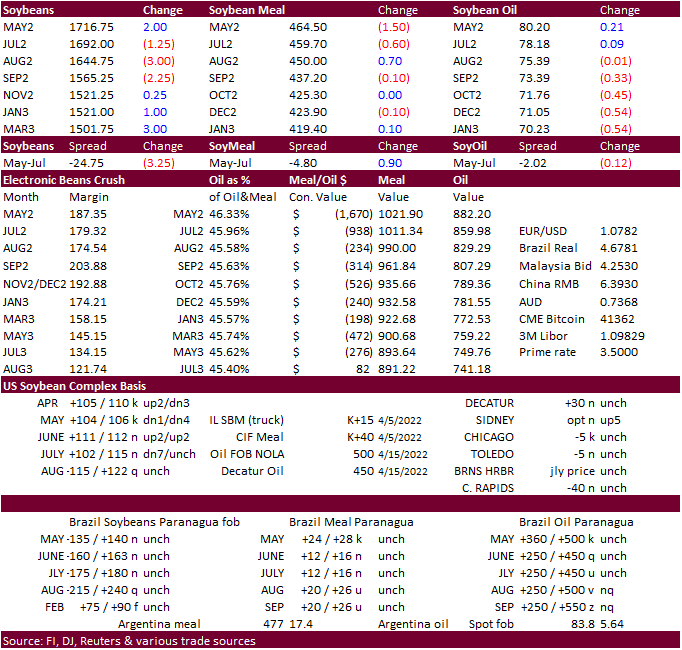

Soybeans

·

July soybeans traded two-sided, eventually seeing support from higher products only to sell off late to close mixed. Soybean meal took charge during the morning day session but a reversal in nearby soybean oil pressured meal/oil

spreads. Sharply lower corn paired some of the gains made earlier in soybean meal. Both products closed mixed withy bear spreading a feature in meal and bull spreading in soybean oil.

·

WTI was down more than $5.40 as of 12:20 pm CT. It appears we saw risk off trading across the commodity space. News was light.

Malaysia

was on holiday, returning Wednesday.

·

Argentina maritime workers plan to strike Thursday for 24 hours over the way the government has been awarding agriculture tenders, stating they see delays. We see no market impact unless it gets extended.

·

Anec: Brazil soybean exports during April could end up near 11.980 million tons, down from 12.023 seen last week. Soybean meal exports were seen at 1.956 million tons, down from 2.070 million previous.

·

Brazil collected 87 percent of their soybean crop as of April 16, according to Conab, 2.8 points below this time last year.

·

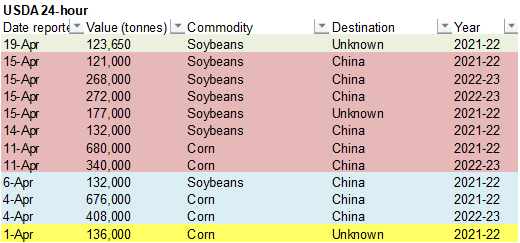

The latest 24-hour sales reported today, and Friday, are leading us to think USDA will increase their 2021-22 US export forecast next month. Since April 1, USDA announced 685,650 tons of 2021-22 soybeans were sold to unknown and

China. That is just over 25 million bushels. Based on monthly inspections, we see March soybean exports near 115 million bushels, less than what we originally projected. Inspections have picked up in April and we estimate 119 million bushels will be exported

for the month, up from 50.9 million a year ago. Our 2021-22 US soybean export estimate is 2.150 billion bushels, above USDA’s 2.115 billion estimate. We look for USDA to bump up soybean exports next month by 20-25 million bushels and reduce the carryout to

around 235 million bushels from current 260 million.

·

Two concerns hang over the soybean market. Inflation in March was 8.5 percent, in large part to higher oil and food prices, leading some to think global meat consumption could contract (not US). Second is Covid lockdowns in China,

which are still going on. This slowed soybean imports that may last through at least the end of April.

·

The IMF on Tuesday lowered its global economic growth by nearly a full percentage point, citing the Russia/Ukraine conflict. They also warned that inflation is now a “clear and present danger” for many countries.

·

Rail Chicago meal basis was down $5/short ton to 14 over the May, Decatur (IL) down $5 to 15 over the May, and Fostoria (OH) off $5 to 15 over the May.

·

European Union soybean imports in the 2021-22 (July-June) season reached 11.24 million tons by April 17, compared with 11.90 million tons by the same week in 2020-21.

·

USDA reported 123,650 tons of soybeans sold to unknown for the 2021-22 marketing year.

·

China looks for sell another 500,000 tons of soybeans during the April 18-23 workweek.

Soybeans

– May $16.00-$17.75

Soybeans

– November is seen in a wide $12.75-$15.50 range

Soybean

meal – May $440-$490

Soybean

oil – May 77-82

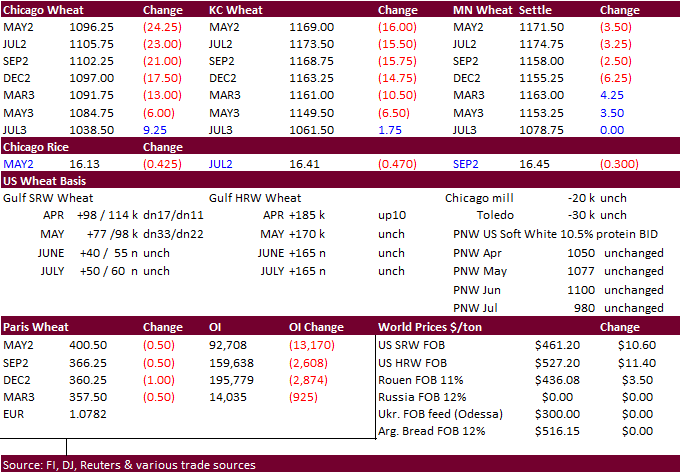

·

US wheat was

lower for much of the session led by Chicago from fund selling. We thought US wheat would trade higher after US winter wheat ratings were surprisingly well below (3 points) expectations. Back month MN wheat was higher. Next week we will pass our initial winter

wheat by class production estimates as the winter wheat is established.

·

Some analysts are calling a high in the wheat market but we caution strong global export developments and strength in cash wheat could allow for the US markets to make another leg higher. It will be important to watch the slow

US export pace.

·

Traders are still assessing the impact on Egypt and Indonesia opening their doors to potential India wheat imports. AgriCensus reported India 11.5% wheat export prices at around $340-$350/ton, up about $7/ton from the previous

week. For comparison, Gulf 11% protein wheat was just over $500/ton.

·

A large snowpack across southeastern Canada and the upper US Great Plains is preventing spring wheat plantings and other summer grain fieldwork preparations. Temperature will warm up as the workweek goes on.

·

September EU wheat futures settled 1.75 euros lower at 365 euros.

·

EU soft wheat exports for the week ending April 17 from July 1, 2021, reached 21.26 million tons, down from 22.08 million tons by the same week in 2020-21.

·

Jordan passed on 120,000 tons of feed barley.

·

Japan seeks 27,320 tons of wheat on Thursday.

·

Jordan seeks 120,000 tons of feed wheat on April 20.

·

Japan seeks 70,000 tons of feed wheat and 40,000 tons of feed barley on April 20 for arrival by September 29.

·

Taiwan seeks 47,120 tons of US wheat on April 21 for June 2 through June 21 if shipped off the PNW.

Rice/Other

·

None reported

Updated

4/13/22

Chicago May $9.75 to $12.00 range, December $8.50-$12.00

KC May $10.50 to $12.00 range, December $8.75-$13.50

MN May $10.75‐$12.00, December $9.00-$14.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Suite 1450

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.