PDF Attached

US

CPI (M/M) Apr: 0.3% (est 0.2%; prev 1.2%)

US

CPI Ex Food And Energy (M/M) Apr: 0.6% (est 0.4%; prev 0.3%)

US

CPI (Y/Y) Apr: 8.3% (est 8.1%; prev 8.5%)

US

CPI Ex Food And Energy (Y/Y) Apr: 6.2% (est 6.0%; prev 6.5%)

A

rally in WTI by more than $5 and follow through buying lifted soybeans, corn and wheat higher. Inflation concerns could have fueled fund buying. Ongoing weather concerns for the southern US winter wheat crop, China, western EU and India remain a large concern.

US weather remains favorable for US Midwest planting progress, and we are looking at big jump for this week’s corn and soybean planting progress.

![]()

WEATHER

EVENTS AND FEATURES TO WATCH

- U.S.

Texas Panhandle and portions of western and northern West Texas cotton areas received rain overnight with some of it significant - Amounts

varied from 0.40 to 1.40 inches most often with a few greater totals - The

high coverage and significance of this rain makes this event the best so far this season - A

beneficial boost in topsoil moisture has resulted, but without good follow up rain and in an environment of warmer than usual temperatures it will not take long for this precipitation event to be lost - Drought

conditions will prevail, despite the precipitation event - A

more substantial rain event is still needed to support dryland planting and crop development - Northern

U.S. Plains and Canada’s eastern Prairies will receive additional showers rain Thursday afternoon into Saturday - The

moisture will be greatest from northeastern Montana and far northwestern North Dakota to eastern Saskatchewan where 0.75 to 2.00 inches will result - Rain

reported in northeastern Saskatchewan Tuesday already ranged up over 1.00 inch and the additional rain will saturate the topsoil

- Manitoba

and North Dakota along with northern Minnesota have been too wet so far this spring to get much fieldwork done and the Thursday/Friday rain event will ensure further delays while expanding saturated soil from those areas into eastern Saskatchewan - Saturday

through Tuesday will be dry or mostly dry in the northern U.S. Plains and eastern Canada’s Prairies, but showers during mid-week next week and a few days later will limit the drying trend and maintain concern about spring planting - Canada’s

southwestern Prairies will continue too dry, despite a few showers over the next ten days to two weeks - Western

and some northern Alberta, Canada crop areas are too wet and need to dry down for spring planting - Cool

weather will evolve in Canada’s Prairies and the northern U.S. Plains next week and especially in the following weekend resulting in the return to frost and freeze conditions for some areas, although the weather may trend a little drier for a while - Rain

chances may improve in the southwestern Canada Prairies after next week’s cold weather abates - Eastern

U.S. Midwest planting progress will be most aggressive over the balance of this workweek - Recent

drying has firmed the soil favorably for more aggressive fieldwork, although additional drying is needed in low-lying areas and in regions of heavy clay soil - U.S.

southeastern states are drying down and may soon become a little too dry - A

few showers are expected in the coming ten days, but resulting rainfall may not counter evaporation very well - A

tropical disturbance may evolve next week in the Caribbean Sea, although confidence on where the system will go and how significant it may or may not become is very low - Today’s

GFS model develops a tropical cyclone and brings it to the southeastern United States, but this will not likely verify - The

Texas Blacklands, South Texas and Coastal Bend crop areas will be dry through the next ten days and then there may be some rain potential

- Crop

moisture stress will remain high in dryland production areas of South Texas and the Texas Coastal Bend where dryness has been a long term issue this spring - U.S.

temperatures will remain warm over the next several days from the southern Plains and mid-south regions into the Midwest

- Cooling

is expected next week bringing temperatures down to a more seasonable range - Extreme

highs in the 80s and lower 90s are expected over the next few days and that will accelerate drying and stimulate greater crop development rates - No

general changes were noted in South America overnight - Brazil

will receive rain this weekend from Paraguay through western and southern Mato Grosso do Sul to northern Rio Grande do Sul, Santa Catarina, Parana and Sao Paulo - The

moisture will be great for late season crops - Crop

moisture stress and dryness will prevail over the next couple of weeks in Mato Grosso and Goias as well as northeastern parts of the nation - Some

showers will develop in the northeast next week, but resulting rainfall should not be enough to seriously impact harvest progress or crop conditions - Argentina

will continue in a net drying mode except in Formosa, far northern Chaco and northernmost Corrientes over the next couple of weeks - Drying

is of little concern for now, but rain will be needed in western Argentina late this month and in June to support winter wheat, barley and canola planting

- Northern

South America will experience frequent rain and thunderstorms over the next ten days resulting in some local flooding

- Colombia

and Venezuela as well as Ecuador and the northern Amazon River Basin will be most vulnerable to the heavy rainfall and flooding - Tropical

Cyclone Asani moved a portion of the central Andhra Pradesh coast overnight and was producing 45 mph wind speeds southeast of Repalle - The

storm produced rain in much of Andhra Pradesh, India Tuesday and early today with amounts through 0300 GMT varying from 0.30 to more than 2.75 inches - Additional

rain will fall over the next few days while the storm center moves through a part of the upper Andhra Pradesh coast - Damage

to crops and property has been low - Europe

is expected to continue drying down due to limited rainfall and mild to warm temperatures - France,

Germany, southern parts of the U.K. and Spain will become driest as time moves along, although drying is also expected in Poland and Czech Republic - Any

rain that occurs after May 20 will be light and not well distributed, but a little relief is expected - Western

and northern Russia will receive waves of rain in the coming week to ten days maintaining or inducing wet field conditions and delaying spring fieldwork - Rain

in western and northern Kazakhstan earlier this week as well as that in the southeastern Russia New Lands was ideal in lifting topsoil moisture for improved spring wheat and sunseed planting and establishment conditions - North

Africa is drying out, but mostly to the benefit of winter crop filling, maturation and early harvesting - The

region will be dry for a while - India’s

far Eastern States may get too much rain in the coming week resulting in some flooding - Most

of India will continue to experience warm to hot temperatures and sporadic rainfall during the next ten days

- The

exception will be along the lower west Coast of the nation where monsoonal rainfall is expected to begin early and be greater than usual - South

Africa will experience net drying over the week in many areas and that will prove ideal for summer crop maturation and harvest progress.

- Some

winter crop planting is also expected during this period of drier weather - Rain

will return to the west during the middle and latter part of next week just in time to support autumn wheat, barley and canola planting - Ontario

and Quebec, Canada weather will be dry biased into the weekend and the temperatures will trend warmer - This

will result in better field working opportunity for corn and other crops - Wheat

development will be accelerated as well - Next

week’s weather will trend a little wetter and a little cooler - Mexico

rainfall is expected to support isolated to scattered showers and thunderstorms in southern and eastern parts of the nation this week - Most

of the rain is not expected to be enough to counter evaporation and more rain will be needed in time - Central

America will see periodic rain in the coming ten days with some of it to become heavy this weekend and next week from Costa Rica into Panama.

- Xinjiang,

China rainfall will be greatest in the mountains where a boost in water supply for irrigation is expected

- Planting

of cotton and corn as well as other crops is well under way and the outlook is favorable for most irrigated areas - Mainland

areas of China will be wettest south of the Yangtze River during the next two weeks, although there will be some other bouts of rain periodically in other areas in the nation and all of it will be welcome - Net

drying is possible in east-central parts of the nation and in Liaoning which may raise a little concern about dryness in time - Rain

is expected in the Yellow River Basin where an improvement in winter and spring crop conditions are expected after recent drying

- South

Korea rice production areas are too dry and little change is expected over the next ten days - Some

of this dryness will expand northward into North Korea - Southeast

Asia rainfall will be abundant to excessive in the next ten days from Myanmar into Thailand, Laos and Cambodia as well as from eastern parts of Borneo into the southern Philippines and Papua New Guinea - Some

flooding is expected in many areas - Southwest

monsoon rainfall in Myanmar could become excessive later this week with 10.00 to 20.00 inches of rain possible over the southern most parts of the nation and into the northern Malay Peninsula - Tropical

Cyclone Karim poses no threat of land from a position in the central Indian Ocean - Eastern

Australia will receive additional rain over the next few days - Total

amounts of 1.50 to 4.00 inches will occur in central and northern New South Wales and southern Queensland by Friday while 3.00 to 8.00 inches are expected along the lower Queensland coast

- Crop

quality declines are possible in sugarcane areas and some unharvested cotton quality will decline - Sorghum

should not be harmed, although harvest delays are likely - Canola,

wheat and barley planting potentials will increase greatly following this period of rainy weather - Western

Australia will get some beneficial rain the southwest over the next few days

- The

moisture will help improve planting for some areas, but more rain will be needed - Some

follow up rain is expected next week - South

Australia and Victoria rainfall will be most limited over the next two weeks - West-central

Africa will experience frequent rainfall over the next ten days supporting coffee, cocoa, sugarcane and rice development - Some

northern cotton areas need greater rain - East-central

Africa rainfall will be most significant in southwestern Ethiopia, southwestern Kenya and Uganda during the next ten days while Tanzania begins to dry down seasonably - Today’s

Southern Oscillation Index was +20.07 and it has likely peaked or is peaking, but will remain strongly positive for a while

- New

Zealand weather will be drier than usual during the coming week. Some rain will fall in western portions of South Island

Source:

World Weather Inc.

Bloomberg

Ag Calendar

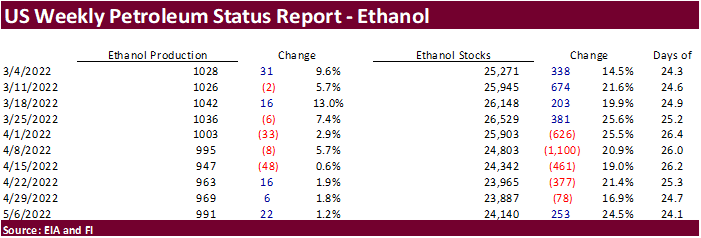

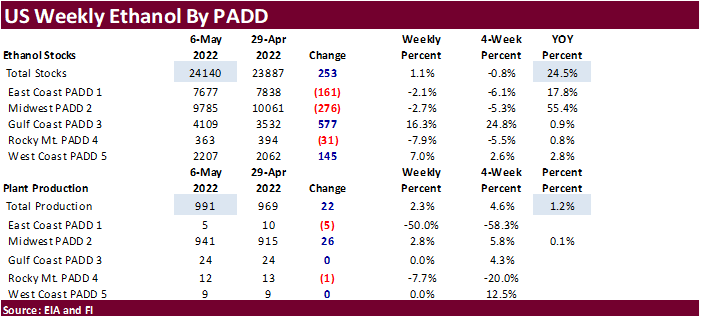

- EIA

weekly U.S. ethanol inventories, production, 10:30am - Globoil

International 2022 in Dubai, day 3 - France

AgriMer monthly grains outlook - Annual

New York Sugar Conference, hosted by Datagro and International Sugar Organization

Thursday,

May 12:

- USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - USDA’s

monthly World Agricultural Supply and Demand (WASDE) report, 12pm - China’s

agriculture ministry (CASDE) releases monthly report on supply and demand for corn and soybeans - Brazil’s

Conab releases data on area, yield and output of corn and soybeans - New

Zealand food prices

Friday,

May 13:

- ICE

Futures Europe weekly commitments of traders report - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions

US

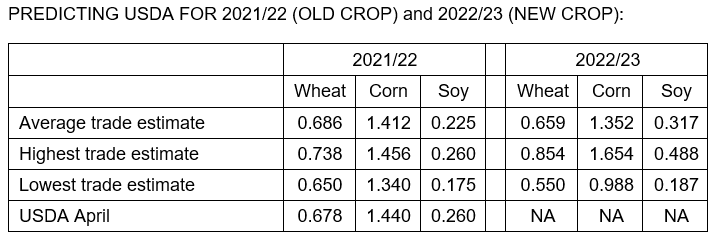

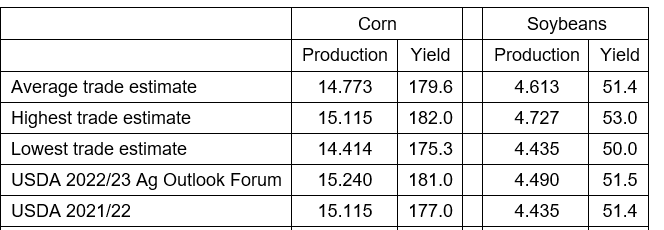

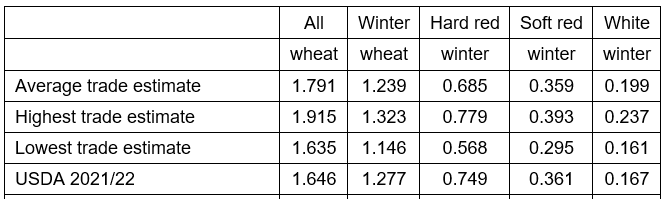

production

US

wheat production

Global

stocks

SA

production 2021-22

Macros

US

CPI (M/M) Apr: 0.3% (est 0.2%; prev 1.2%)

US

CPI Ex Food And Energy (M/M) Apr: 0.6% (est 0.4%; prev 0.3%)

US

CPI (Y/Y) Apr: 8.3% (est 8.1%; prev 8.5%)

US

CPI Ex Food And Energy (Y/Y) Apr: 6.2% (est 6.0%; prev 6.5%)

US

Real Average Hourly Earnings (Y/Y) Apr: -2.6% (prev 2.7%; prevR -2.6%)

US

Real Average Weekly Earnings (Y/Y) Apr: -3.4% (prev -3.6%; prevR -3.5%)

US

DoE Crude Oil Inventories Change (W/W) 06-May: 8487K (est -1450K; prev 1303K)

–

Distillate Inventories: -913K (est -1000K; prev -2344K)

–

Cushing Inventories: -587K (prev 1379K)

–

Gasoline Inventories: -3607K (est -1600K; prev -2230K)

–

Refinery Utilization: 1.60% (est 0.50%; prev -1.90%)

·

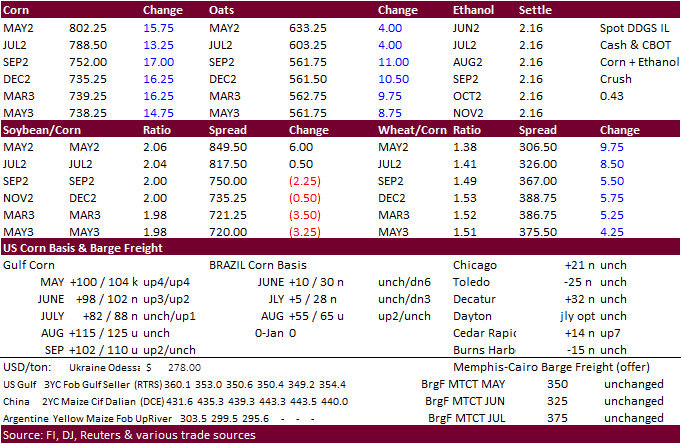

Corn futures traded higher on technical buying, higher WTI crude oil and inflation concerns.

·

Funds bought an estimated net 10,000 corn contracts.

·

Rosario Grains Exchange: 2021-22 Argentina corn production estimated at 49.2 million tons.

·

The Baltic Dry Index gained for the eighth consecutive session, by 113 points or 3.8% to 3,052 points.

·

China suspended goats, sheep and other animal units from Mongolia after detecting a viral disease.

·

The weekly USDA Broiler Report showed eggs set in the United States up slightly and chicks placed down slightly. Cumulative placements from the week ending January 8, 2022, through May 7, 2022, for the United States were 3.35

billion. Cumulative placements were down slightly from the same period a year earlier.

Export

developments.

·

(New 5/10) South Korea’s KFA bought 65,000 tons of corn at an estimated $379.95 a ton c&f for arrival in South Korea around Aug. 20.

·

China plans to buy 40,000 tons of pork for reserves on May 13.

Updated

4/22/22

July

corn is seen in a $7.25 and $8.65 range

December

corn is seen in a wide $5.50-$8.50 range