PDF Attached

FOMC

Hikes By 75Bps; Target Range Stands At 2.25% – 2.50%

FOMC

Interest Rate On Reserves Balances Raised To 2.40% From 1.65%

Fed

Raises Main Rate In Unanimous Vote, Ongoing Hikes Likely To Be Appropriate

US

Interest Rate Futures See Fed Funds Rate 3.4% In December After 75Bps Hike

–

See 107Bps Of Tightening For Rest Of 2022

The

US morning and midday weather outlook appeared to be mostly unchanged. Ridging is still a strong possibility for the Midwest next week. The Midwest will see rain favoring the southern areas through Saturday and north central areas today. The Great Plains will

see rain across NE and northern KS through today and far western GP Thursday through Saturday.

US

equities rallied post FED rate announcement and short speech thereafter. US corn traded mixed, ending higher. Wheat sold off on technical selling while the soybean complex rallied on US weather concerns and ideas US meal export demand could increase due to

lack of global meal shortages.

![]()

World

Weather Inc.

WEATHER

TO WATCH AROUND THE WORLD

-

Northwestern

U.S. Corn and Soybean Belt already trending too dry -

The

latest soil assessment shows an expansion of dryness from Nebraska and South Dakota into southern Minnesota and western Iowa -

The

poorest soil conditions are in northeastern Nebraska, northwestern Iowa, southeastern South Dakota and southern Minnesota

-

Soil

conditions have improved from this week’s rain from eastern Kansas into southwestern Illinois and

-

Rain

is expected to continue into the weekend from southern Kansas, Oklahoma and the northern Texas Panhandle into the U.S. Delta and Kentucky with a few areas in the Ohio River Valley to be included -

Net

drying is advertised in other areas in the Midwest, but temperatures will be mild during much of this period of time keeping the drying rates slow. Crop conditions should remain favorable outside of the northwestern Corn and Soybean Belt -

Hotter

conditions will reach the Great Plains late this weekend before intensifying and advancing from west to east across the Midwest during the week next week -

The

heat will not be preceded by much significant rain suggesting the northwestern U.S. Corn and Soybean Belt will be facing some very stressful conditions next week unless greater rain evolves than advertised and that is not very likely -

Warming

across most of the U.S. Midwest along with restricted rainfall next week and into the following weekend will accelerate drying rates

-

Much

of the Midwest will have favorable soil moisture initially to help limit the impact of hotter and drier weather, but temperatures in the 90s Fahrenheit will be sufficient to accelerate drying rates -

Extreme

highs over 100 will impact the Plains next week with the northern and central Plains and western Corn Belt in the midst of the hottest conditions during mid- to late week next week

-

Crop

stress in the Midwest outside of the northwestern Corn and Soybean Belt will evolve in the week 2 period (August 3-9) period, but the most threatening period of potential stress would come in the August 10-17 period “IF” the drier and warmer weather pattern

prevails -

Northwestern

Corn and Soybean areas will see stress immediately since soil conditions are already quite dry -

The

bulk of Texas will continue in a dry and warm to hot mode for much of the coming week to nearly ten days -

There

is potential that rain may evolve in Texas while the high pressure ridge attempts to move into the eastern Midwest during the August 5-10 period -

Confidence

in this eastward shift in the ridge is low and therefore so is the rain potential in Texas; however, in August rainfall potential should improve for the Texas coast, South Texas and neighboring northeastern Mexico

-

Excessive

heat continues to improve the Pacific Northwest and this pattern will prevail through the weekend -

Extreme

highs reached 111 degrees at The Dalles, Oregon -

Other

highs in the Pacific Northwest were in the 90s to 106 Fahrenheit -

Southern

British Columbia reported extreme highs to 104 -

Some

relief is expected after the weekend, although warmer than usual conditions may continue for a little while longer -

Temperatures

should become more seasonable during the second week of the outlook -

Increased

monsoonal rainfall is possible in the southwestern United States next week and into the following weekend – especially if the North America high pressure ridge briefly shifts farther to the east -

World

Weather, Inc. believes the U.S. high pressure ridge may briefly reach into the heart of the Midwest late next week and into the following weekend, but the odds are high that the ridge will retrograde to the west in the following week allowing some cooling

in the eastern Midwest, but keeping the Plains and western Midwest quite warm and drier biased -

Much

of Europe rainfall will be restricted over the next ten days while temperatures are near to above normal

-

Net

drying is expected in the majority of the continent, but especially in France, the U.K., Belgium, Netherlands, Germany, Spain, Portugal and from the lower Danube River Basin to Hungary -

Eastern

Europe will receive rain this weekend into early next week from Czech Republic and Austria to Belarus and northwestern Ukraine with rainfall of 1.00 to 2.00 inches and locally more resulting -

Net

drying will persist for the next couple of weeks from Hungary into Greece resulting in more threatening crop heat and moisture stress -

A

mostly good mix of weather will occur in the Commonwealth of Independent States through the next two weeks

-

Concern

remains over erratic rainfall in Russia’s Southern Region, southeastern Ukraine and parts of Kazakhstan -

Rain

is expected in Russia’s Southern region and temperatures will be mild enough to conserve the resulting rainfall through lower evaporation rates -

A

boost in rainfall is advertised for western, central and northern Ukraine after the end of this week and the moisture increase will bring on better crop and field conditions -

Argentina

received some welcome rainfall Tuesday and early today in Buenos Aires and La Pampa -

Moisture

totals varied from 0.10 to 0.60 inch in central and southern Buenos Aires and La Pampa with local totals of 1.00 to 2.00 inches in western Buenos Aires -

The

greatest rain fell in east-central Buenos Aires where 2.00 to 4.39 inches resulted in several areas.

-

Wheat

and barley emergence and establishment will improve as a result of the rain.

-

Argentina

will see additional rain today and Thursday mostly in the south and east-central parts of the nation while the west-central and northwest stay a little too dry -

Far

southern Brazil will receive periodic rainfall during the next ten days maintaining a typically moist pattern in the soil from Rio Grande do Sul into Paraguay, southernmost Mato Grosso do Sul and parts of both Parana and southern Sao Paulo -

The

moisture will be great for winter crops and should not have much impact on Safrinha crop maturation or harvesting -

Safrinha

cotton and late corn harvesting in Brazil will advance well due to continued dry and warm weather -

There

is no threat of cold weather in Brazil coffee, citrus or sugarcane areas during the next two weeks -

Southeastern

Canada crop conditions are rated favorably with little change likely for a while -

Canada’s

southwestern and central Prairies will dry down over the next week to ten days and temperatures will slowly rise above normal.

-

Crop

stress will rise once again as soil moisture is slowly depleted -

The

greatest stress will eventually evolve in central, west-central, southwestern and south-central Saskatchewan and southeastern Alberta, but conditions will remain favorable through the weekend -

India’s

monsoonal rainfall is expected to continue widespread across the nation during the next two weeks with all areas impacted and most getting sufficient rain to bolster soil moisture and/or induce flooding -

Some

areas may become too wet, but the precipitation will occur with sufficient breaks to prevent serious flooding from occurring -

Nationwide

rainfall is still expected to be above normal at mid-August and serious relief should occur to the dry areas of Uttar Pradesh and Bihar which have not received nearly as much rain as usual so far this year. Cotton, groundnut and soybean areas of northwestern

India should experience mostly good weather for crop improvements after flooding rain earlier this month -

China’s

weather is still advertised to be drier than usual in the southeastern corner over the next five days, but rain is expected thereafter -

The

return of rain should benefit rice and other late season crops -

The

greatest rain is still a week away -

Timely

rainfall is expected in most other areas in the nation during the next two weeks maintaining moisture abundance and a mostly good crop development environment -

China’s

Xinjiang province continues to experience relatively good weather -

A

few showers and thunderstorms are expected, but most of the region will be dry with temperatures varying greatly over the week to ten days -

Some

cooling is expected in Argentina late this week into early next week -

Sumatra,

Indonesia rainfall has started to improve with a couple of central west coast locations reporting heavy rainfall Monday and early today -

Rain

-

All

other Southeast Asian nations will experience an abundance of rainfall during the next few weeks resulting in some flooding in the Philippines and the Maritime provinces -

Australia

weather in the coming ten days will be favorable for most winter crops -

Central

Queensland received rain Wednesday and Thursday favoring a boost in topsoil moisture for a part of winter crop country

-

Western

Australia will get most of the significant rain this coming week, but some rain will eventually reach the southeastern parts of the nation in time next week.

-

South

Korea rice areas are still dealing with drought, despite some rain that fell recently.

-

Some

additional showers are expected over the next couple of weeks, but a soaking rain will continue to elude the region -

Western

Pacific Ocean tropical activity is expected to increase greatly over the next two weeks with multiple storms possibly impacting China, Taiwan, Japan and the Korean Peninsula -

The

stormiest conditions are expected in the second week of the forecast -

There

are no tropical cyclones in the Atlantic Ocean, Caribbean Sea or Gulf of Mexico and none are expected during the next ten days -

Tropical

Storm Frank remained well off the southwest coast of Mexico today -

This

system is expected to become better organized and evolve into a hurricane, but its movement should be away from western North America

-

East-central

Africa rainfall this week will be greatest in central and western Ethiopia, but it will soon be increasing in Uganda and Kenya -

Tanzania

is normally dry at this time of year, and it should be that way for the next few of weeks -

West-central

Africa rainfall has been and will continue sufficient to support coffee, cocoa, sugarcane, rice and cotton development normally -

Some

greater rain would still be welcome in the drier areas of Ivory Coast -

Seasonal

rains are shifting northward leading to some drying in southern areas throughout west-central Africa -

Cotton

areas are expecting greater rainfall in the next couple of weeks -

South

Africa’s crop moisture situation is favorable for winter crop establishment, although some additional rain might be welcome -

Restricted

rainfall is expected for a while, but the crop is rated better than usual -

Central

America rainfall will continue to be abundant to excessive and drying is needed -

Mexico

rain will be most abundant in the west and southern parts of the nation -

Rain

in the Greater Antilles will occur periodically, but no excessive amounts are likely -

Today’s

Southern Oscillation Index was +7.33 and it will continue to drift a little lower over the next few days, but should gradually level out -

New

Zealand weather is expected to be well mixed over the next two weeks -

Temperatures

will be seasonable with a slight cooler bias

Source:

World Weather INC

Bloomberg

Ag Calendar

Wednesday,

July 27:

- EIA

weekly U.S. ethanol inventories, production, 10:30am - Earnings:

Bunge

Thursday,

July 28:

- USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - Buenos

Aires grains exchange weekly crop report - HOLIDAY:

Thailand

Friday,

July 29:

- Vietnam

July coffee, rice and rubber export data - FranceAgriMer

weekly update on crop conditions - ICE

Futures Europe weekly commitments of traders report - US

agricultural prices paid, received, 3pm - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - HOLIDAY:

Thailand

Source:

Bloomberg and FI

Macros

US

Durable Goods Orders Jun P: 1.9% (est -0.4%; prev 0.8%)

–

Durable Goods Ex Transportation Jun P: 0.3% (est 0.2%; prev 0.7%; prevR 0.5%)

–

Cap Goods Orders Nondef Ex Air Jun P: 0.5% (est 0.2%; prev 0.6%; prevR 0.5%)

–

Cap Goods Ship Nondef Ex Air Jun P: 0.7% (est 0.2%; prev 0.8%; prevR 1.0%)

US

Wholesale Inventories (M/M) Jun P: 1.9% (est 1.5%; prev 1.8%; prevR 1.9%)

US

Pending Home Sales (M/M) Jun: -8.6% (est -1.0%; prev R 0.4%)

–

Pending Home Sales NSA (Y/Y): -19.8% (est -13.5%; prev R -12.3%)

US

DoE Crude Oil Inventories (W/W) 22-Jul: -4.523M (est -1.037M; prev -0.445M)

–

Distillate Inventories: -0.784M (est +0.500M; prev -1.295M)

–

Cushing OK Crude: +0.751M (prev +1.143M)

–

Gasoline Inventories: -3.304M (est -0.857M; prev +3.498M)

–

Refinery Utilization: -1.5% (est +0.4%; prev -1.2%)

102

Counterparties Take $2.189 Tln At Fed Reverse Repo Op (prev $2.189 Tln, 98 Bids)

·

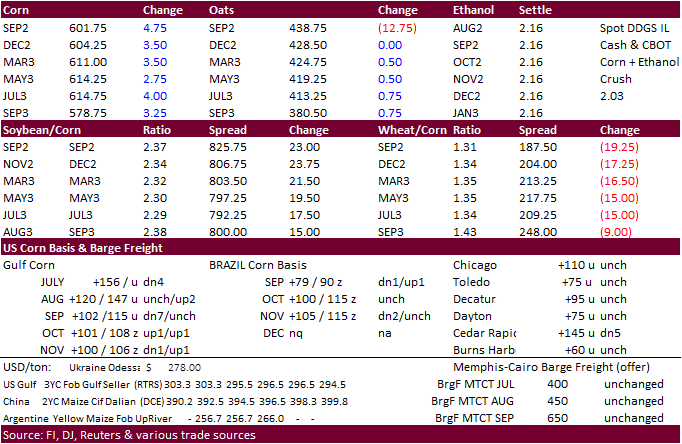

CBOT corn started higher on follow through buying from dryness across Europe and drier weather for the US through first week of August. Prices eventually eroded from a reversal in wheat to the downside but rebounded into the close

with September settling 3.25 cents higher and December 2.25 cents higher. Bull spreading was a feature all day.

·

Funds bought an estimated net 1,000 corn contracts.

·

Look for US weather to remain the driver for price influence.

·

South Africa’s CEC in their initial estimate of the 2022 corn crop was 14.713 million tons, down 10 percent from 16.315 million tons collected in 2021. White corn was seen at 7.470 million tons and 7.243 million tons for yellow

corn.

·

Bloomberg: Saudi Arabia is expected to increase its price for crude oil to a record differential for September.

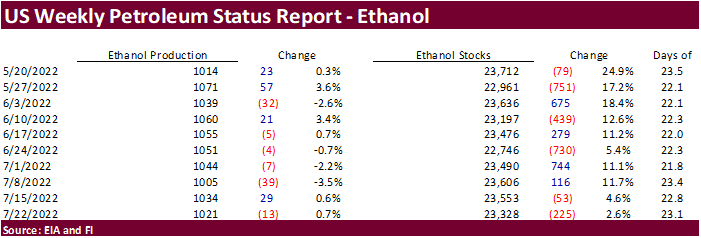

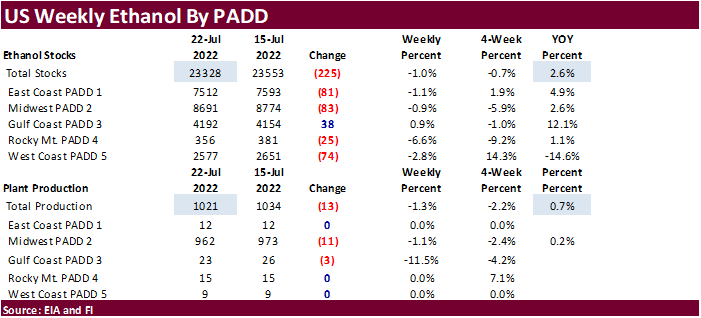

US

weekly ethanol production

decreased 13,000 barrels from the previous week to 1.021 million and stocks decreased 225,000 barrels to 23.328 million. A Bloomberg poll looked for weekly US ethanol production to be down 2,000 barrels and stocks up 95,000 barrels to 23.648 million. Weekly

gasoline demand increased 724,000 barrels to 9.245 million.

US

DoE Crude Oil Inventories (W/W) 22-Jul: -4.523M (est -1.037M; prev -0.445M)

–

Distillate Inventories: -0.784M (est +0.500M; prev -1.295M)

–

Cushing OK Crude: +0.751M (prev +1.143M)

–

Gasoline Inventories: -3.304M (est -0.857M; prev +3.498M)

–

Refinery Utilization: -1.5% (est +0.4%; prev -1.2%)

USDA

Attaché: Canada Grain and Feed Update

·

None reported

Updated

7/25/22

September

corn is seen in a $5.10 and $6.40 range

December

corn is seen in a $5.00-$7.50 range