PDF Attached

Refinitiv:

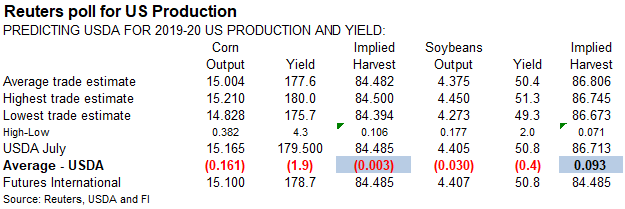

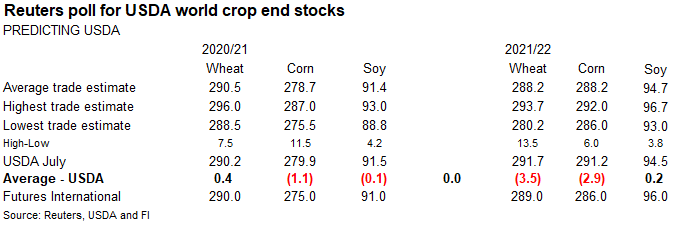

POLL- The yield average is 177.6 for US corn and 50.4 soybeans, 15.004 and 4.375 average for production. Looking at the ranges, they are tight, so any surprises should be considered. Low/high production ranges were reported at 14.828-15.210 for US corn

and 4.273-4.450 soybean production. USDA was at 15.165 & 4.405 billion bushels for July, both below the Reuters trade average, but not by much. I would focus on changes in US 2020-21 soybean crush and Brazil corn reduction on top of adjustments in US ending

stocks when USDA updates Aug 12.

WASHINGTON,

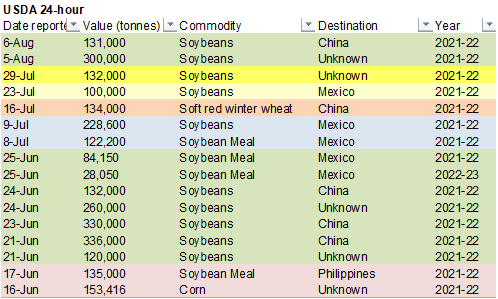

Aug 6, 2021—Private exporters reported to the U.S. Department of Agriculture export sales of 131,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year.

WORLD

WEATHER INC.

MOST

IMPORTANT WEATHER OF THE DAY

- Increasing

tropical activity is expected in the Atlantic Ocean this weekend

o

One disturbance will reach the Greater Antilles early next week and will approach Florida in the second weekend of the two week outlook

o

A second disturbance could become a tropical depression or tropical storm this weekend or early next week, according to the National Hurricane center, although the 0800 EDT update today reduced the potential for tropical cyclone

development this weekend

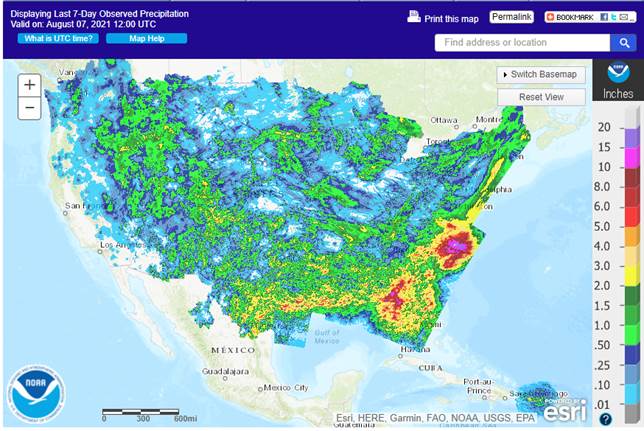

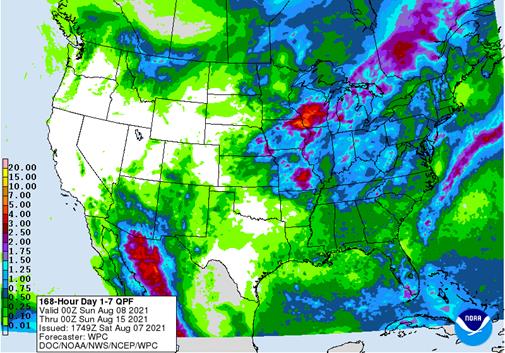

- U.S.

western Corn Belt rainfall this weekend into mid-week next week will prove to be very important since it offers some needed moisture to slow down the potential advancement of dryness from the northern Plains and upper Midwest into Iowa,

o

Rain will fall Saturday into Sunday with some follow up moisture in a part of the region during mid-week next week

- Sufficient

rain will fall for a short term improvement in soil moisture further delaying the onset of moisture stress that is still expected later this month - Iowa,

southeastern Minnesota, Wisconsin, Illinois, eastern Nebraska and northern Missouri will be impacted

- Drying

is expected in the western Corn Belt beginning late next week and lasting beyond mid-month - Crop

stress will eventually develop, but how soon that occurs and how significant it is will be largely determined by rainfall in this coming week - South

Texas harvest conditions will continue very good through the weekend as dry weather dominates the region - U.S.

Delta weather continues to improve with less frequent and less significant rain

o

Harvest progress is expected to advance well for corn and other early season crops

o

Soybean, rice, cotton and other crops will continue to develop well with lingering soil moisture and a few showers periodically

- U.S.

southeastern states weather will remain well mixed over the next ten days supporting normal crop development - Florida

could experience a boost in rainfall during the second weekend of the two week outlook from a tropical wave or tropical disturbance - West

Texas cotton, corn and sorghum conditions are rated favorably and should stay that way for a while

o

Warmer weather this weekend into early next week will help to accelerate plant growth rates

- Far

western U.S. weather will remain drier biased for the next ten days to two weeks

- Canada’s

Prairies will experience unsettled weather for the next five days allowing some scattered showers and thunderstorms to occur in parts of the Prairies that have been drought stricken all summer

o

Resulting rainfall will not be enough to seriously change crop or field conditions, although some locally moderate rain may evolve in a few areas

- Southeast

Canada corn, soybean and wheat conditions are rated favorably with little change likely over the next week to ten days

o

Wheat harvest progress is advancing well on the drier days

o

Corn and soybean production potentials are very good

- India’s

weather will continue wet in central and eastern parts of the nation for the next week to ten days while southern and far northwestern areas as well as Pakistan experience net drying conditions

o

Some crop stress is expected in western Gujarat, western Rajasthan and southern and central Pakistan because of predicted dryness

o

Interior southern India will be drying down, but crops will manage relatively well with lingering subsoil moisture – at least for a while

- Greater

rain will be needed soon - Grain

quality concerns remain from France to Belarus where small grain and a few winter rapeseed crops have been negatively impacted by frequent rainfall this season

o

Rain will continue periodically in these areas through the weekend

o

Net drying is expected in many of these wetter areas next week

- Southeastern

Europe’s dry and warm bias will continue over the next ten days

o

The impact will be mostly on the Balkan countries where the ground is already dry and recent temperatures have been hot

o

Unirrigated summer crops are stressed and need significant rain soon to protect production potentials

- China

continues to recover from serious flooding, but another week may be needed for some of the flood water to recede from crop areas in east-central China - China

weather over the next ten days will be erratic with alternating periods of rain and sunshine in key grain, oilseed, rice and cotton areas

o

Flooding rain has occurred most recently in the southern coastal provinces due to Tropical Storm Lupit

- Additional

heavy rain will fall into Saturday - Some

crop damage to rice and some sugarcane will be possible - Frequent

rain will fall near and south of the Yangtze River during the next ten days resulting in some rising potential for localized flooding - Thailand

rainfall is expected to continue lighter than usual in many areas during the next week to ten days

o

Totally dry weather is not likely, but a part of the interior east and interior south will fail to receive more than 1.50 inches which is well below that of most years

o

Vietnam rainfall is also expected to be lighter than usual while Laos and eastern Cambodia are plenty moist along with Myanmar

- Indonesia

and Malaysia weather is expected to trend wetter and that will prove to be quite favorable after recent weeks of lighter than usual rain

o

The weekend and next week will be wettest with some heavy rain possible in western Sumatra and moderate amounts in Malaysia

- Philippines

rainfall decline has helped ease flooding in western Luzon

o

Less rain fell in the region this week, but rain has continued to fall maintaining excessive moisture and flooding in some areas

- Some

damage to rice and other crops has occurred

o

Lighter rainfall will continue for a few days

o

Soil conditions in Philippines are now driest in western Mindanao and in some of the southern Visayan Islands

- CIS

weather over the coming ten days will provide net drying conditions in from eastern Ukraine through portions of Russia’s Southern Region and Volga River Basin into the southern Ural Mountains Region and northwestern Kazakhstan

o

Rain will fall in western and central Ukraine, Belarus, the Baltic States, far western Russia and in most of the eastern Russia New Lands

- The

moisture will be good for late season crops, but dryness in summer corn, sorghum and sunseed areas from southern Russia into Kazakhstan is a concern and greater rainfall needed, but not much more than sporadic showers will occur for at least ten days - Brazil

coffee areas are beginning to warm up after last week’s frost and freezes

o

A lack of rain and warmer temperatures will stress crops while trying to recover from the freeze which should lead to some additional concern over 2022 production

- Most

Brazil grain, citrus and sugarcane areas were also free of damaging cold in recent days and there will be no further concern about that potential

o

The impact of cold weather last week in citrus areas was minimal, but it may have been a little greater in sugarcane areas, but not as great as that which occurred July 19-21

o

Winter wheat production may have been negatively impacted by the freezes of July 19-21 and July 29-30.

- Brazil

rainfall will be limited to coastal areas during the coming week

o

The nation’s temperatures will be mild to warm in the east with no other threats of frost or freezes

o

Warm temperatures are expected to evolve in the west and north

o

Some rain will evolve in the far south during mid-week next week

- Argentina

weather will be dry biased today, but rain is expected this weekend

o

Soil conditions are still dry in the west where wheat and barley may not be as well established as they should be, although most of the crop is in better shape than either of the past two years

o

The weekend rain will be welcome, but probably no enough to seriously improve crops in the west that are a little too dry

- Winter

crops are semi-dormant and will not likely respond to the precipitation for a while - Tropical

Storm Lupit will move from the coastal region near the Fujian/Guangdong common border area across the northern tip of Taiwan this weekend before moving across Japan’s main island next week

o

The storm has already produced flooding rain to coastal areas of southern China and it will do the same for parts of Taiwan this weekend before bringing rain to Kyushu, Honshu and Shikoku Japan next week

o

Crop damage should be low because of the storm’s weak intensity

- Tropical

Storm Mirinae will stay far enough to the east of Japan’s main islands this weekend and early next week to be a minimal impact on the nation’s crops and property - Australia

weather will be favorably mixed for canola, wheat and barley

o

Crops have established well in most of the nation

o

Queensland and northern New South Wales need more rain

o

This week’s rainfall will be lighter and less frequent than that of last week

- Ethiopia

rainfall has been abundant in recent weeks along with that in Kenya, according to the U.S. Climate Prediction Center, but Uganda has been drier than usual

o

The next two weeks will be wetter than usual in western and central Ethiopia and near to above normal in Kenya and Uganda coffee and cocoa production areas

- West-central

Africa rainfall has diminished seasonably for a while

o

Rainfall during July was below average in southwestern Nigeria and Cameroon while closer to normal in other coffee, cocoa, sugarcane and coffee areas

o

Rainfall was above normal last month in Senegal

o

Rain will be needed in Ghana and Ivory Coast soon, but this is the normal dry season and rain will resume in September

- South

Africa weather was mostly dry Thursday except for a few southern coastal showers

o

Some periodic showers will occur in the far southwest of the nation – mostly near the coast during the coming week while other areas will be dry

- Southern

Oscillation Index has reached +12.01 and it will continue to decline over the next several days - Mexico

weather has been improving with increased rainfall in the south and west parts of the nation

o

Drought conditions are waning and crops are performing better

o

Dryness remains in eastern Chihuahua and northeastern parts of the nation

o

Weather over the next ten days will offer some relief, but more rain will be needed in the drier areas

- Central

America rainfall has been plentiful and will remain that way

o

Central America rainfall will be near to above average during the next ten days

- New

Zealand rainfall during the coming week will be near normal except in the western part of South Island where rainfall will be greater than usual

o

temperatures will be seasonable

Source:

World Weather Inc.

Saturday,

Aug. 7

- China’s

first batch of July trade data, incl. soybean, edible oil, rubber and meat imports

Monday,

Aug. 9:

- USDA

export inspections – corn, soybeans, wheat, 11am - U.S.

crop conditions – corn, cotton, soybeans, wheat, 4pm - Ivory

Coast cocoa arrivals - EARNINGS:

Minerva - HOLIDAY:

Japan, Singapore

Tuesday,

Aug. 10:

- EU

weekly grain, oilseed import and export data - Brazil’s

Conab releases data on yield, area and output of corn and soybeans - Purdue

Agriculture Sentiment - HOLIDAY:

Malaysia

Wednesday,

Aug. 11:

- EIA

weekly U.S. ethanol inventories, production - Malaysian

Palm Oil Board’s stockpiles, output and production data - Brazil’s

Unica publishes data on cane crush and sugar output (tentative) - Vietnam’s

customs department releases July trade data - EARNINGS:

JBS, Wilmar - HOLIDAY:

Indonesia

Thursday,

Aug. 12:

- USDA’s

monthly World Agricultural Supply and Demand (WASDE) report, noon - USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - China

farm ministry’s monthly supply-demand report (CASDE) - New

Zealand Food Prices - Port

of Rouen data on French grain exports - HOLIDAY:

Thailand

Friday,

Aug. 13:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions - EARNINGS:

Olam, Golden Agri

Source:

Bloomberg and FI

Reuters

headlines on China trade data (table was unavailable)

-

CHINA

JULY CRUDE OIL IMPORTS 41.24 MLN TONNES VS 40.14 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL OIL PRODUCT IMPORTS 15.04 MLN TONNES VS 18.73 MLN TONNES YR EARLIER – CUSTOMS -

CHINA

JULY OIL PRODUCT EXPORTS 4.64 MLN TONNES VS 6.44 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JULY OIL PRODUCT IMPORTS 2.52 MLN TONNES VS 2.14 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL CRUDE OIL IMPORTS 301.83 MLN TONNES VS 319.76 MLN TONNES YR EARLIER – CUSTOMS -

CHINA

JAN-JUL OIL PRODUCT EXPORTS 41.08 MLN TONNES VS 36.95 MLN TONNES YR EARLIER – CUSTOMS -

CHINA

JULY UNWROUGHT COPPER AND COPPER PRODUCTS IMPORTS, 424,280.3 TONNES, VS 428,437.5 TONNES IN JUNE – CUSTOMS -

CHINA

JULY RARE EARTH EXPORTS 3,955.4 TONNES VS 4,012.4 TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL RARE EARTH EXPORTS 27,781.0 TONNES VS 22,735.8 TONNES YR EARLIER – CUSTOMS -

CHINA

JULY UNWROUGHT ALUMINIUM AND ALUMINIUM PRODUCTS EXPORTS 469,030.60 TONNES VS 454,397.40 TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL UNWROUGHT COPPER AND COPPER PRODUCTS IMPORTS, 3,219,071.9 TONNES, VS 3,600,722.4 TONNES A YR EARLIER – CUSTOMS -

CHINA

JULY STEEL PRODUCTS EXPORTS 5.67 MLN TONNES VS 6.46 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL UNWROUGHT ALUMINIUM AND ALUMINIUM PRODUCTS EXPORTS 3,085,140.60 TONNES VS 2,737,114.30 TONNES YR EARLIER – CUSTOMS -

CHINA

JAN-JUL STEEL PRODUCTS EXPORTS 43.05 MLN TONNES VS 32.88 MLN TONNES YR EARLIER – CUSTOMS -

CHINA

JULY IRON ORE IMPORTS 88.51 MLN TONNES, VS 89.42 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL IRON ORE IMPORTS 649.03 MLN TONNES, VS 658.93 MLN TONNES A YR EARLIER – CUSTOMS -

CHINA

JULY SOYBEAN IMPORTS 8.67 MLN TONNES, VS 10.72 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL SOYBEAN IMPORTS 57.63 MLN TONNES, VS 55.13 MLN TONNES A YR EARLIER – CUSTOMS -

CHINA

JULY COAL IMPORTS 30.18 MLN TONNES, VS 28.39 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL COAL IMPORTS 169.74 MLN TONNES, VS 199.68 MLN TONNES A YR EARLIER – CUSTOMS -

CHINA

JULY NATURAL GAS IMPORTS 9.34 MLN TONNES VS 10.21 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL NATURAL GAS IMPORTS 68.96 MLN TONNES VS 55.60 MLN TONNES YR EARLIER – CUSTOMS -

CHINA

JULY COPPER CONCENTRATES IMPORTS, 1.89 MLN TONNES, VS 1.67 MLN TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL COPPER CONCENTRATES IMPORTS, 13.39 MLN TONNES, VS 12.63 MLN TONNES A YR EARLIER – CUSTOMS -

CHINA

JULY MEAT IMPORTS 854,000 TONNES, VS 743,000 TONNES IN JUNE – CUSTOMS -

CHINA

JAN-JUL MEAT IMPORTS 5.93 MLN TONNES, VS 5.75 MLN TONNES A YR EARLIER – CUSTOMS

Commitment

of Traders

US

Change In Nonfarm Payrolls Jul: 943K (est 858K; prevR 938K; prev 850K)

US

Unemployment Rate Jul: 5.4% (est 5.7%; prev 5.9%)

US

Average Hourly Earnings (M/M) Jul: 0.4% (est 0.3%; prevR 0.4%; prev 0.3%)

US

Average Hourly Earnings (Y/Y) Jul: 4.0% (est 3.9%; prevR 3.7%; prev 3.6%)

7US

Change In Private Payrolls Jul: 703K (est 709K; prevR 769K; prev 662K)

US

Change In Manufacturing Payrolls Jul: 27K (est 26K; prevR 39K; prev 15K)

US

Average Weekly Hours All Employees Jul: 34.8 (est 34.7; prevR 34.8; prev 34.7)

US

Labor Force Participation Rate Jul: 61.7% (est 61.7%; prev 61.6%)

US

Underemployment Rate Jul: 9.2% (prev 9.8%)

Canadian

Net Change In Employment Jul: 94.0K (est 150K; prev 230.7K)

Canadian

Unemployment Rate Jul: 7.5% (est 7.4%; prev 7.8%)

Canadian

Hourly Wage Rate Permanent Employees (Y/Y) Jul: 0.6% (est 0.2%; prev 0.1%)

Canadian

Participation Rate Jul: 65.2% (est 65.5%; prev 65.2%)

Canadian

Full Time Employment Change Jul: 83.0K (prev -33.2K)

Canadian

Part Time Employment Change Jul: 11.0K (prev 263.9K)

NY

Fed Purchases $12.401 Bln In Tsy Coupons

68

Counterparties Take $952.134 Bln At Fed’s Fixed-Rate Reverse Repo (prev $944.335 Bln, 70 Bidders)

US

Consumer Credit (USD) Jun: 37.690B (est 23.000B; prev R 36.690B)

- US

corn futures traded higher Friday on strength in soybeans amid China demand and higher wheat. US corn demand developments were slow this week with a limited amount of import tenders. The US weather forecast still calls for Midwest to see rain across the

west central and northwestern areas today through Monday. Corn options were active on Friday. Fundamental news was light. Some traders are speculating China might be back in buying corn for new-crop delivery, but we saw no confirmation of that as of Saturday

morning. - A

Reuters poll calls for the US corn yield to come in near 177.6 bu/ac and production at 15.004 million. The yield would be 1.9 below USDA July and production 161 million bushels below USDA. Implied harvested are nearly at USDA’s current estimate.

- Farm

Futures pegged the US corn yield at 178.7 bu/acre and production at 15.1 billion bushels. USDA is at 179.5 bu and 15.165 billion.

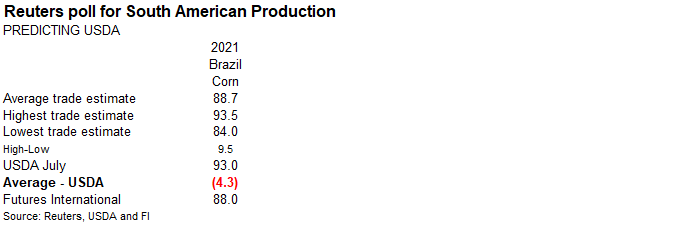

- A

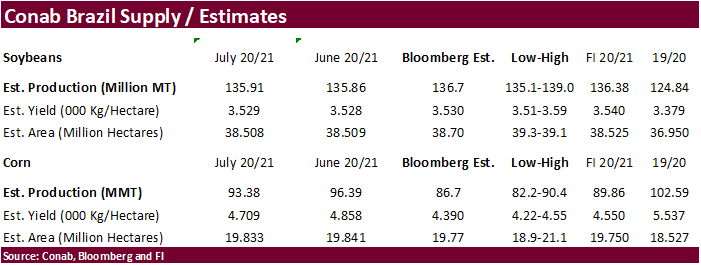

Reuters poll looks for Brazil corn production to be lowered to 88.72 million tons from 93 million. We look for USDA to cut Brazil corn production by 5 million tons next week. Latest Brazil corn production to come out was AgRural, with a 60.9 million ton

estimate, down from 65.3 million tons a year ago. - China’s

Sinograin sold 26,447 tons of imported US corn, 12% of what was offered. They also sold 12,962 tons of non-GMO corn from the Ukraine, 26% of what was offered.

- Argentina’s

BA Exchange reported that the corn harvest is 89.2% complete and left production unchanged at 48 million tons.

Export

developments.

- Qatar

seeks about 100,000 tons of barley on August 18 for Sep-Nov delivery.

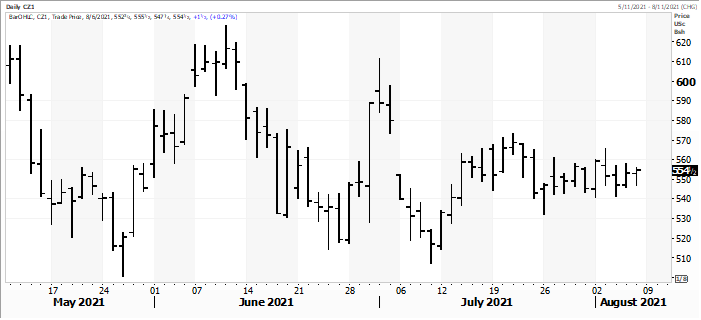

December

corn has been in a sideways trading range sin mid-July

Source:

Reuters

September

corn is seen is a $5.25-$6.00 range.

December

corn is seen in a $4.25-$6.00 range.

-

US

soybean complex ended higher on Friday on improving demand, not weather. Recall the last two Friday’s soybeans traded lower. There was additional talk of China securing soybeans off the PNW and this was confirmed by USDA as they announced 131,000 tons of

soybeans were sold to China for 2021-22 delivery. -

A

Reuters poll calls for the US soybean yield to and up near 50.4 bu/ac, 0.4 below USDA’s 50.8 July estimate, and production to come in near 4.375 billion bushels, 30 million below USDA. It’s interesting to seer the average trade guess calls for the harvested

area to increase 93,000 acres while the implied corn area is expected to be near unchanged form USDA’s estimate. Both soybean and corn production estimates indicate large supplies that may be needed for USDA’s current demand projections.

-

China

July soybean imports were 8.67 million tons, down a hefty 14 percent from 10.1 million during July 2020. Jan-Jul soybean imports are still running above year ago. Reuters noted a Saturday story that “crushing margins in Rizhao, Shandong province, a major

processing hub in eastern China hit their lowest levels on record in June this year, before climbing back up.” Crush margins improved on our working spreadsheet from the previous week but are still low enough to indicate they will be stepping up crush rates.

They crush for mainly meal but could be focusing on soybean oil soon. -

We

heard China washed out cargoes of Canadian canola oil and EU rapeseed oil this week. At least two (60k/ton) cargoes of canola and an unknown amount of EU rapeseed oil. Some think the recent purchases of US soybeans was to make up for the loss in vegetable

importable supplies, but we also heard earlier this week that China was only about 40 percent covered for soybean domestic consumption for the month of October. Either way you look at it, China soybean flash sales are supportive as we have not seen a good

demand headline in a while, including crush. -

Global

vegetable oil markets were hardest hit out of the major agriculture markets this week. Over the long term we remain bullish soybean oil amid increasing demand for renewable diesel.

-

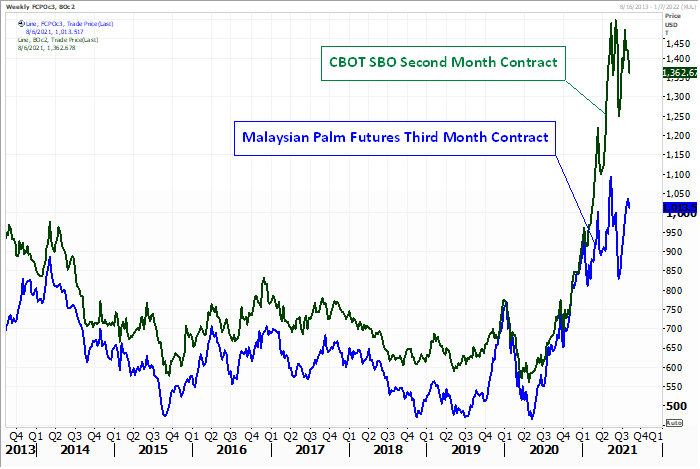

Palm

oil futures were 57 ringgits higher on Friday and for the week, were down about 2.2%.

-

Safras

reported Brazil producers sold an estimated 24 percent of the upcoming 142.2 million soybean new-crop (their estimate),up from 21.5% in June and compares to 43.3% year earlier. Average is just over 20%. We think producers have been reserve sellers due to

market volatility and concerns over the ongoing drought situation.

Export

Developments

- USDA

reported under the 24-hour reporting system 131,000 tons of soybeans were sold to China for 2021-22 delivery.

Soybean

oil versus palm oil.

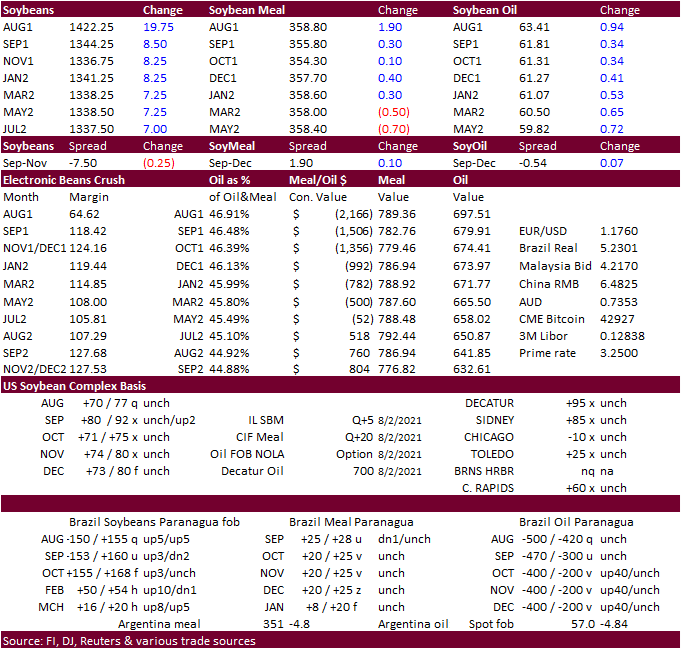

We expect the discrepancy to stick around given US demand for biofuels. What used to be the $75-$110 spread norm is now $150-250/ton.

Source:

Reuters and FI

Updated

8/3/21

September

soybeans are seen in a $12.50-$14.50 range; November $11.75-$15.00

September

soybean meal – $335-$370; December $320-$425

September

soybean oil – 57.50-69.00; December 48-67 cent range

- Wheat

ended higher Friday due to ongoing concerns over global high protein wheat supplies. World import demand remains steady. Other news was light. There was no change in the Friday weather forecast for the Great Plains . Rain is expected for eastern NE and

northeastern KS Saturday and then Monday. Next week we look for some US harvesting pressure to settle in prior to the release of the USDA report. US spring wheat harvesting is running above normal pace for this time of year.

- Russia’s

formula based wheat export customs duty will decline to $31/ton, from $31.40/ton, according to the AgMin. China’s Sinograin sold 26,447 tons of imported US corn, 12% of what was offered. They also sold 12,962 tons of non-GMO corn from the Ukraine, 26% of

what was offered. - December

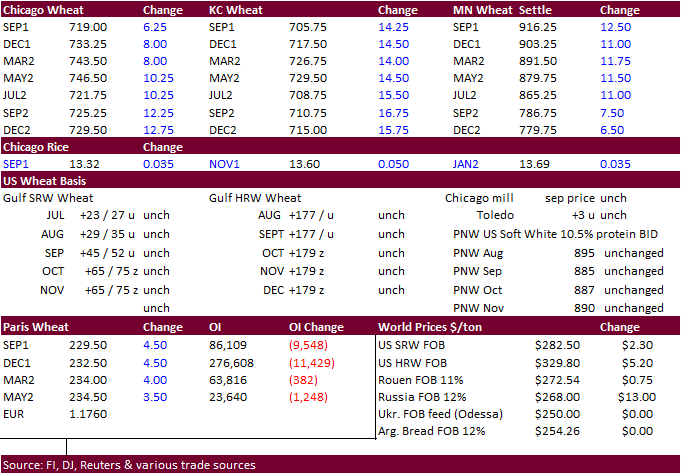

Paris wheat was up 4.25 at 232.25 euros per ton. We would not be surprised to see another leg up in this market next week if USDA decides to lower Black Sea wheat production led by trimming Russian supplies.

- Argentina’s

BA Exchange left the wheat planting unchanged at 6.5 million hectares from last week and the crop is 99.7% planted.

US

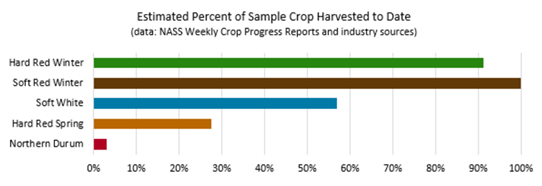

Wheat Associates: “The HRW harvest is winding down with less than 10% remaining. The SW crop is progressing quickly with more than 50% harvested; testing data are reflective of a stressed crop. Durum conditions are slightly better than HRS but remain

drought and heat stressed. HRS harvest is nearly 30% complete while durum harvest is just underway.”

- South

Korea’s KOFIMIA bought 135,100 tons of US (100k) and Canadian wheat (35,100), various proteins for October shipment for most.

- The

Taiwan Flour Millers’ Association bought 48,000 tons of grade 1 northern spring, hard red winter and white milling wheat to be sourced from the United States, for shipment from the U.S. Pacific Northwest coast between Sept. 24 and Oct. 8. - Tunisia

bought 75,000 tons of soft wheat at $315/ton and 100,000 tons of barley at $296.08/ton

for

late Aug through third week of September shipment. - Pakistan

seeks 400,000 tons of wheat for Sep and Oct shipment. - Jordan

is back in for 120,000 tons of wheat on August 11. - Japan

(SBS) seeks 80,000 tons of feed wheat and 100,000 tons of feed barley on August 18 for loading by November 30.

Algeria

seeks at least 50,000 tons of wheat for Aug/Sep shipment. - Bangladesh

seeks 50,000 tons of wheat on August 18. - Pakistan

seeks 400,000 tons of wheat on August 23.

Rice/Other

- South

Korea’s Agro-Fisheries & Food Trade Corp. seeks 39,226 tons of rice from the United States for arrival in South Korea on Jan. 31 and March 31, 2022.

Updated 7/29/21

September Chicago wheat is seen in a $6.25‐$7.50 range

September KC wheat is seen in a $5.90‐$7.25

September MN wheat is seen in a $8.50‐$10.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.