PDF Attached

In

a risk off session, outside markets led CBOT ag futures lower. USD was up 19 points and WTI crude down $1.10 around the time CBOT ags closed. Private exporters reported sales of 130,000 metric tons of corn for delivery to Mexico during the 2021/2022 marketing

year.

USDA

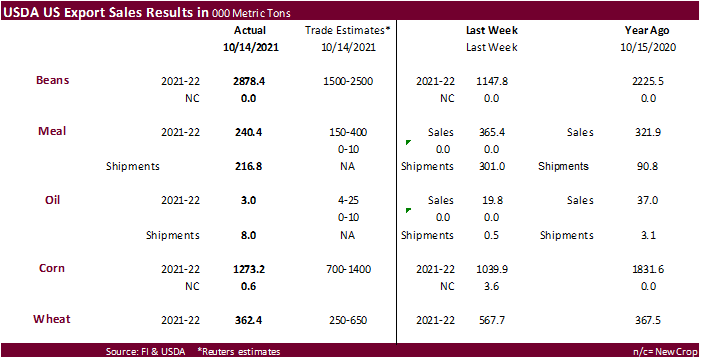

Export Sales were excellent for soybeans (China and unknown destinations), poor for soybean oil and within expectations for meal, corn and wheat. China didn’t buy US corn, but they bought sorghum. Pork sales were good at 20,900 tons.

![]()

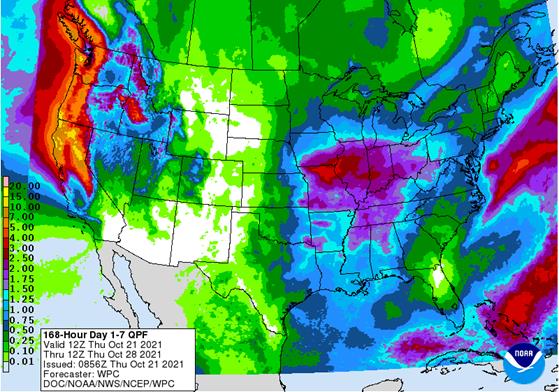

7-day

MOST

IMPORTANT WEATHER AROUND THE WORLD

- Northern

California and southwestern Oregon will experience a succession of heavy rain events through the weekend into Monday resulting in some flooding - Very

heavy mountain snow fall is expected with 1-3 feet of accumulation possible in the highest elevated areas - Favoring

the northern Sierra Nevada and other mountains in northern California - Moisture

totals will range from 2.00 to 4.00 inches along the Washington and northern two-thirds of the Oregon coast with a few areas to get upwards to 6.00 inches; however, moisture totals along the northern California coast and in the northern Sierra Nevada mountains

will range from 5.00 to 10.00 inches - Flooding

may cause damage to personal property, infrastructure and some agriculture - Stormy

weather in the northwestern U.S. this weekend into early next week will also bring some welcome moisture to the drought areas of the Yakima and Columbia River Basins as well as some light rain in the Snake River system - These

areas have all be drought stricken for much of the past year - U.S.

Great Plains weather will be mostly dry during the next ten days - This

will be a greater concern for the unirrigated high Plains region from southwestern Nebraska and eastern Colorado to the Texas Panhandle where dryness is already a factor - Wheat

emergence and establishment will be poor in unirrigated areas - Many

other wheat areas to the east will dry down, but crop weather in recent weeks has supported good planting progress and favorable emergence and early establishment - U.S.

Midwest, Delta and southeastern states will be a little more disrupted by precipitation this weekend through much of next week - Moderate

to heavy rain is expected in parts of the Midwest from a couple of weather systems - Harvest

delays should be expected, but improved weather is likely in the final days of October and early November - Rainfall

in the Delta will be moderately great early next week, but it should be of short duration - Concern

over cotton fiber quality may resume - Delays

in harvesting are likely for a little while - The

best alternating pattern of rain and sunshine will be in the southeastern states - Montana

and portions of neighboring Canada will be drier biased for the next ten days - U.S.

NWS 30-day outlook for November called for warmer than usual conditions in much of the nation excepting the far northwest and north-central areas along with a part of the western Corn Belt where equal chances for above, below and near normal temperatures was

suggested - Precipitation

was advertised below normal for most of the southern states from southern California through Kansas, Oklahoma and Texas to the southeastern states

- Above

normal precipitation was advertised for the Pacific Northwest, northern Rocky Mountain region and northwestern Plains as well as in the Great Lakes region and northeastern states

- U.S.

NWS 90-Day weather outlook for November through January suggested warmer than usual temperatures for most of the nation excepting the Pacific Northwest, and northern Plains where equal chances for above, below and near normal temperatures was suggested - The

only cooler than usual bias was advertised for western Washington State - Precipitation

was suggested to be greater than usual from the northern Rocky Mountain region and northwestern Plains into the Pacific Northwest and from the eastern Midwest into the northeastern states - Below

average precipitation was advertised for the southern states from southern California through Oklahoma and Texas to the southeastern states from Florida to North Carolina - Equal

chances for above, below and near normal precipitation was advertised for all other areas - Another

round of flooding rain is expected along the central Vietnam Coast beginning this weekend and lasting through Monday - Rain

totals of 6.00 to 12.00 inches and locally more will result with the Hue and Da Nang areas to be most impacted - The

area impacted was already hit with flooding rainfall during the past weekend and early on Monday of this week - A

tropical cyclone may impact the same region during the middle part of next week further perpetuating the flood conditions - Personal

property damage has been and will likely continue to be greater than that on agriculture with a human impact likely greatest - A

tropical disturbance will evolve over the Philippines this weekend and it will organize into a weak tropical cyclone over the south China Sea Sunday and Monday while trekking to the west toward Vietnam - The

storm may move across Vietnam’s Central Highlands raising some concern over coffee and other crops in the region - The

developing system will need to be closely monitored, but the impact on coffee and Vietnam is a week away - Today’s

forecast models have made this tropical system much weaker than advertised Wednesday and that may reduce some of the rain and certainly the potential for high wind speeds in coffee and other crop areas of the Central Highlands - A

Low pressure center moving off the Tunisia, Africa coast this weekend will move over the central Mediterranean Sea and intensify - This

system has potential to possibly become a subtropical storm with impacts on Sicily and far southern Italy next week

- The

storm could produce torrential rainfall and strong wind speeds - Confidence

is low, but the potential storm will need to be closely monitored - There

is also some potential that it could impact Greece as well - A

tropical disturbance off the southwestern Mexico coast today and Friday will evolve into a tropical storm Friday before turning into Mexico over Michoacan Sunday or Monday

- The

storm may also impact western Guerrero and southeastern Jalisco with heavy rain and strong wind speeds - Coastal

crops and personal property will be at risk of damage, although this will be small storm - Excessive

rain and flooding will be the greatest threat, especially in coastal areas - Moisture

from this storm will stream into the Texas coastal region and may help enhance rain in the U.S. Delta next week - Argentina

will receive some welcome rain today into Saturday - Coverage

will be high, but resulting rainfall may be a little light varying from 0.15 to 0.75 inch and locally more - Net

drying is expected after this for Sunday through most of next week - Argentina

still needs greater rain in northwestern parts of the nation where dryness is still significant in the topsoil - Subsoil

moisture is still low over a larger part of the west-central and north parts of the nation

- Next

week’s temperatures will likely trend warmer than usual while dry weather prevails resulting in notable drying for much of the nation - Southern

Brazil’s forecast continues to have a drier bias for the next couple of weeks, although some showers will occur briefly this weekend and possibly again in the second weekend of the outlook - Net

drying in southern Brazil, Uruguay, southern Paraguay and eastern Argentina is not unusual for La Nina events during late spring and summer - La

Nina is still evolving, but as it does this potential for dryness is likely to be reinforced during November warranting a close watch

- Center

west, center south and interior southern parts of Brazil will continue to experience a good mix of rain and sunshine over the next two weeks resulting in favorable planting, germination and emergence conditions for corn and soybeans - Cotton

will also benefit from the pattern - Sugarcane,

citrus and coffee crops are rated favorably and expected to continue benefiting from alternating periods of rain and sunshine during the next two weeks - Australia’s

western and southern crop areas will experience a good mix of rain and sunshine over the next two weeks

- The

environment will be ideal for support of reproducing and filling winter crops - The

nation is well on its way to a huge winter wheat, barley and canola crop - Interior

Eastern Australia is expecting dry weather for the next week to ten days favoring sorghum and cotton planting in irrigated areas and in areas with good soil moisture, but dryland production areas need moisture - Winter

wheat, barley and canola will continue performing very well with good yields possible - Queensland

harvesting is likely done or winding down - World

Weather, Inc. is still looking for a rainfall boost in November for eastern Australia that might threaten some of the wheat, barley and canola quality in New South Wales and Victoria.

- Northern

and eastern China will experience a mostly good weather pattern for summer crop maturation and harvest progress

- Winter

crop planting in the North China Plain and Yellow River Basin will advance well - East-central

and interior southern China will experience alternating periods of rain and sunshine maintaining good field moisture for wheat and rapeseed planting while supporting some summer crop maturation and harvest progress - India’s

weather will be mostly good over the next couple of weeks - Rain

will fall most often in the far south and extreme eastern parts of the nation - Summer

crop harvesting and winter crop planting should advance well - Russia’s

Volga River Basin will continue in need of greater moisture, although winter crops are semi-dormant and established well enough to survive winter if there is good snow cover during period of extreme cold - Soil

conditions are little dry, but moisture was present when crops were emerging - Ukraine

and most of Europe away from the North and Baltic Seas will see tranquil weather for a while allowing late season farming activity to wind down - Winter

crop planting and summer crop harvesting continues to advance well across the European Continent and little change is likely - A

few periods of snow and rain will impact a part of Canada’s Prairies over the next two weeks, but resulting precipitation will not break the drought - Harvesting

of this year’s crops is complete, but the rain is needed to restore soil moisture after a multi-year drought seriously reduced production in 2021 - Southeastern

Canada crop conditions and harvest progress has been varied - Southwestern

Ontario is too wet, and fieldwork has been slowed - Most

of Quebec weather has been more favorable for fieldwork to advance normally - These

conditions may prevail for a while - South

Africa will receive periodic rainfall during the coming ten days and that will bolster soil moisture for improved conditions for late season wheat development and early planting of summer crops - Eastern

parts of North Africa will receive rain this weekend into Monday impacting Algeria and Tunisia most significantly - No

heavy rain is expected except in a few coastal Tunisia locations - Morocco

will remain dry - Central

Africa will continue to experience periodic rainfall during the next ten days maintaining good coffee, cocoa, sugarcane, rice, cotton and other crop conditions - Drier

weather will soon be needed in some cotton and cocoa areas - Rainfall

in the next seven days is expected to be greater than usual - Rainfall

in the second week of the forecast will trend drier favoring better crop maturation conditions - Rain

will fall frequently in Indonesia, Malaysia and Philippines through the next ten to 12 days maintaining a good outlook for palm oil, coconut, corn, rice, sugarcane, citrus and many other crops - Mexico

rainfall will be erratic over the next week with pockets of the nation a little wetter biased while other areas are a little drier biased - Southern

areas will be wetter biased mostly in association with this late weekend and early next week’s land-falling tropical cyclone in the southwest - Central

America rainfall will be below average in the coming week except in Costa Rica, Panama and El Salvador and Guatemala where rainfall will be near to above normal - Central

Asia cotton and other crop harvesting will advance swiftly as dry and warm conditions prevail - Today’s

Southern Oscillational Index was +11.38 and it was expected to move higher during the coming week - New

Zealand weather is expected to be a little drier than usual and temperatures will be seasonable.

Thursday,

Oct. 21:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - International

Grains Council monthly report - Port

of Rouen data on French grain exports - USDA

red meat production, 3pm

Friday,

Oct. 22:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions - U.S.

cattle on feed; cold storage data for pork, beef and poultry, 3pm - USDA

NASS Chicken and Eggs. - HOLIDAY:

Thailand

Monday,

Oct. 25:

- Monthly

MARS bulletin on crop conditions in Europe - USDA

export inspections – corn, soybeans, wheat, 11am - U.S.

poultry slaughter, 3pm - U.S.

cotton condition; corn, soy and cotton harvesting; winter wheat planting, 4pm - Malaysia

Oct. 1-25 palm oil exports - Ivory

Coast cocoa arrivals - HOLIDAY:

New Zealand

Tuesday,

Oct. 26:

- EU

weekly grain, oilseed import and export data - EARNINGS:

WH Group

Wednesday,

Oct. 27:

- EIA

weekly U.S. ethanol inventories, production - Brazil’s

Unica releases cane crush, sugar output data (tentative)

Thursday,

Oct. 28:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - Port

of Rouen data on French grain exports

Friday,

Oct. 29:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - Vietnam’s

General Statistics Office releases October trade data - FranceAgriMer

weekly update on crop conditions - U.S.

agricultural prices paid, received, 3pm

Source:

Bloomberg and FI

USDA

Export Sales

Soybean

export sales were excellent at 2.878 million tons and included China (1,884,400 MT, although 526,000 MT switched from unknown destinations and decreases of 6,300 MT, good amount for unknown destinations (568,800MT) and the Netherlands (127,300 MT – including

124,000 MT switched from unknown destinations). Soybean commitments are still running sharply below a year ago, by 36 percent. Soybean oil export sales were a low 3,000 tons but shipments improved to 8,000 tons. Canada bought 100 tons of new-crop soybean

oil. Soybean meal export sales were 240,400 tons, within expectations while shipments were 216,800 tons, down from 301,000 previous week. Corn export sales were within expectations at 1.273 million tons and included unknown destinations (456,700 MT) and

Mexico (377,100 MT). There were no corn sales to China. All-wheat export sales of 362,400 tons were within expectations but down from 567,700 tons previous week. USDA reported 262,500 tons of sorghum sales, including 127,300 tons to China and 103,000 tons

to unknown. Pork sales were good at 20,900 tons.

Macros

US$

Cross Current Swaps -3% following Turkey cutting -200bps. US$ is higher on volume across the board.

·

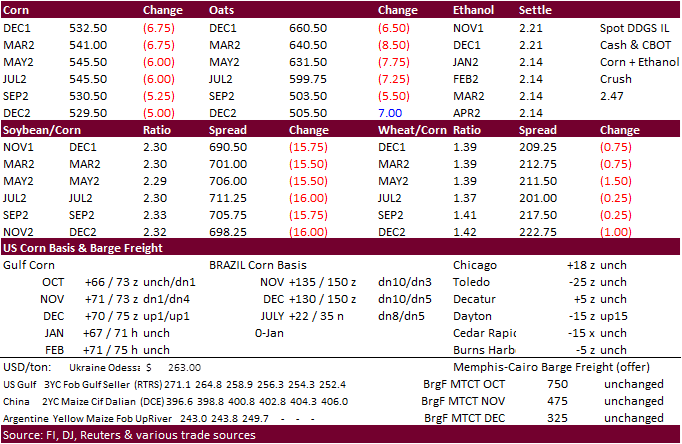

Corn ended 4.25-7.0 cents lower on widespread commodity selling. USDA export sales were 1.273 million tons, withing expectations, but didn’t include China. Sales are on track to fall short of USDA’s export projection, but we

have a long way to go for the crop year. China did buy 127,300 tons of sorghum.

·

Funds sold an estimated net 8,000 corn contracts.

·

The US generated 1.16 billion D6 blending credits in September, down from 1.21 billion in August.

·

Archer-Daniels-Midland sold its Peoria, Illinois ethanol plant, to BioUfja Group.

·

Reuters: Mexico’s agriculture minister say Mexico will not limit GMO corn imports from U.S.

https://www.reuters.com/world/americas/mexicos-agriculture-minister-say-mexico-will-not-limit-gmo-corn-imports-us-2021-10-20/

·

The International Grains Council (IGC) increased their estimate for the 2021-22 global corn crop by 1 million tons to 1.210 billion tons. U.S. corn crop was seen at 381.5 million tons, up from a previous 380.3 million tons. They

projected the 2021 EU corn production at 67.5 million tons, up from 64.9 million tons previously and above the 2020 crop of 64.6 million tons.

·

The USDA Broiler Report showed broiler-type eggs set in the United States up 2 percent and chicks placed up 2 percent. Cumulative placements from the week ending January 9, 2021, through October 16, 2021, for the United States

were 7.62 billion. Cumulative placements were up slightly from the same period a year earlier.

Export

developments.

-

None

reported

Updated

10/12/21

December

corn is seen in a $4.85-$5.55 range

March

corn is seen in a $5.00-$5.70 range

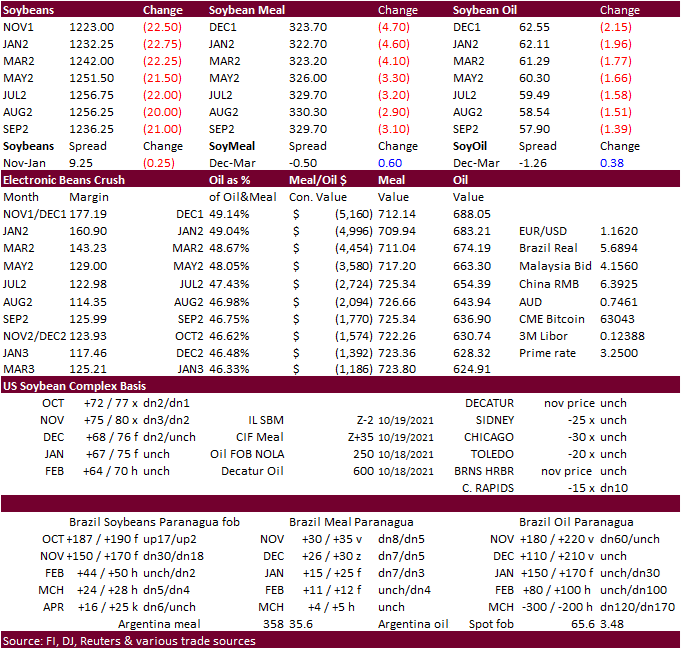

·

CBOT soybeans, meal and soybean oil ended sharply lower in a risk off trade. Soybeans were higher over the past five days. Paris rapeseed sold off. WTI December crude oil is back below $83/barrel and USD higher. USDA export

sales were excellent, but product sales (meal and oil) declined from the previous week. Offshore values were leading meal and soybean oil lower this morning. Funds sold an estimated net 12,000 soybean contracts, 3,000 meal and 7,000 soybean oil.

·

Soybeans finished 20-21.50 cents lower, ,soybean oil 148-212 points lower (bear spreading) and meal $2.70-4.40 lower.

·

US domestic soybean meal basis was sharply higher in the rail market. Chicago, Decatur (IL), and Morristown (IN) were up $8/short ton. KC, Missouri, was up $5/short ton.

·

Paris rapeseed futures were off 15.75 at 686.25 euros/ton.

·

Brazil soybean premiums weakened this week as the USD continues to gain over the Brazilian real.

·

The US generated 385 million D4 blending credits in September, down from 421 million in August.

·

Malaysian palm oil traded lower on Thursday by 103 ringgit and cash was off $20/ton.

·

There was another good round of overnight CME palm oil block trades, many of them strips. Participants are taking large deliveries against the contracts. Importers and exporters like to use the CME palm oil contracts as it settled

in USD, and they don’t have to worry as much over local currency fluctuations. It’s an easy way for them to hedge. End users such as commercials are unlikely participants in these block trades.

·

Cargo surveyor SGS reported month to date October 20 Malaysian palm exports at 920,085 tons, 150,011 tons below the same period a month ago or down 14.0%, and 210,493 tons below the same period a year ago or down 18.6%.

Export

Developments

·

None reported

Updated

10/18/21

Soybeans

– November $11.50-$13.00 range, March $11.50-$13.50

Soybean

meal – December $295-$335, March $300-$360

Soybean

oil – December 59-65 cent range, March 56-65

·

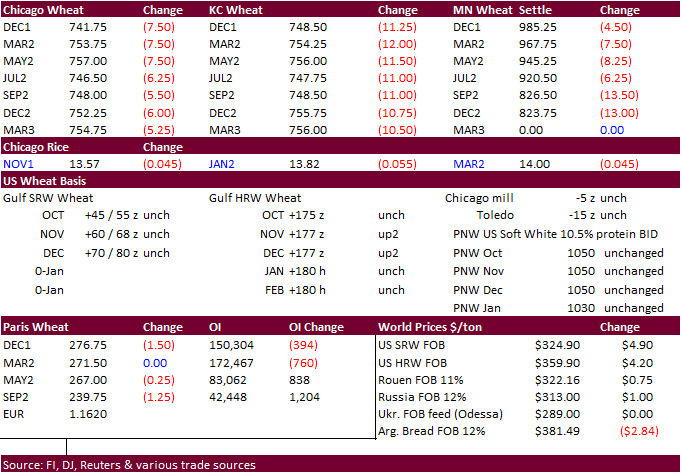

US wheat futures prices ended lower from a higher USD (up around 19 points at the close) and weaker soybeans and corn. KC led the lower trade. Mn saw limited losses on tight global high protein supplies and the December contract

remains near its contract high. USDA export sales slowed from the previous week.

·

Funds sold an estimated net 6,000 Chicago SRW wheat contracts.

·

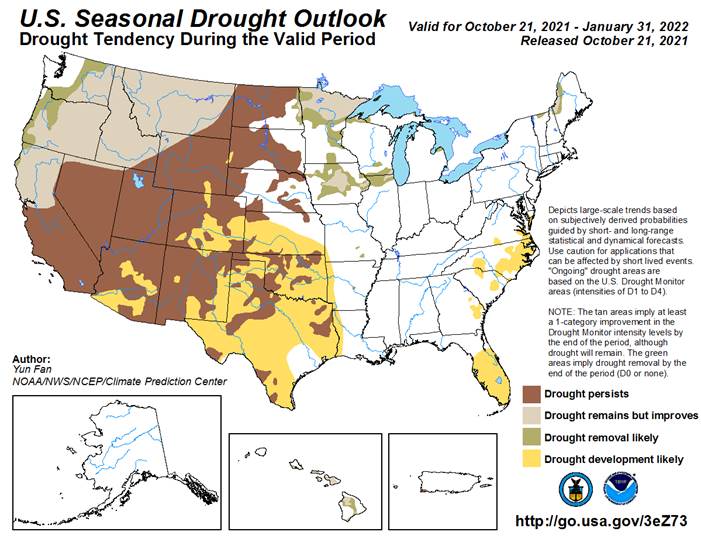

NOAA’s long term forecast calls for drought conditions to increase across the southwest over the winter months.

·

Paris December wheat was down 1.50 euros at 276.75. The contract hit a contract high on Wednesday.

·

The International Grains Council (IGC) left unchanged their estimate for the 2021-22 global wheat crop at 781 million tons.

·

USDA Attaché: Egypt Grains. Wheat imports are seen at 12.4 million tons, up from 12.14 million tons for their 2020-21 projections.

https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Grain%20and%20Feed%20Update_Cairo_Egypt_09-16-2021

Export

Developments.

·

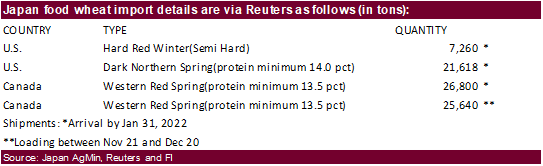

Jordan seeks 120,000 tons of wheat on October 27, optional origin, for shipment between March 1-15, March 16-31, April 1-15 and April 16-30.

·

Turkey’s TMO purchased an estimated 300,000 tons of wheat. They sought 11.5% and 12.5% protein content for shipment between Dec. 10 and Dec. 31.

·

Japan bought 81,318 tons of food wheat as expected. Original details as follows:

·

Jordan passed 120,000 tons of feed barley for FH January through FH March shipment.

·

Pakistan seeks 90,000 tons of wheat on October 25.

·

Turkey seeks 235,000 tons of feed barley on October 26.

·

Ethiopia seeks 300,000 tons of milling wheat on November 9.

·

Ethiopia seeks 400,000 tons of wheat on November 30.

Rice/Other

·

Maldives seeks 25,000 tons of parboiled rice with offers due by October 28.

·

Mauritius seeks 6,000 tons of white rice on October 26 for January 1-March 31 shipment.

December

Chicago wheat is seen in a $7.00‐$7.75 range, March $6.50-$7.75

December

KC wheat is seen in a $7.10‐$7.95, March $6.82-$8.25

December

MN wheat is seen in a $9.00‐$10.00, March $9.00-$10.00

USDA

Export Sales

U.S.

EXPORT SALES FOR WEEK ENDING 10/14/21

|

|

CURRENT |

NEXT |

||||||

|

COMMODITY |

NET |

OUTSTANDING |

WEEKLY |

ACCUMULATED |

NET |

OUTSTANDING |

||

|

CURRENT |

YEAR AGO |

CURRENT |

YEAR AGO |

|||||

|

|

THOUSAND |

|||||||

|

WHEAT |

|

|

|

|

|

|

|

|

|

|

206.5 |

1,640.9 |

1,643.2 |

111.9 |

3,167.3 |

4,144.4 |

0.0 |

0.0 |

|

|

50.9 |

639.2 |

403.9 |

21.0 |

1,207.4 |

879.4 |

0.0 |

0.0 |

|

|

62.2 |

1,000.9 |

1,507.0 |

16.6 |

2,336.8 |

2,904.7 |

0.0 |

0.0 |

|

|

60.9 |

642.8 |

1,452.2 |

10.6 |

1,598.8 |

1,939.5 |

0.0 |

0.0 |

|

|

-18.1 |

42.4 |

220.9 |

0.0 |

61.4 |

321.6 |

0.0 |

0.0 |

|

|

362.4 |

3,966.2 |

5,227.2 |

160.2 |

8,371.8 |

10,189.5 |

0.0 |

0.0 |

|

BARLEY |

0.0 |

23.7 |

32.9 |

0.7 |

6.4 |

9.1 |

0.0 |

0.0 |

|

CORN |

1,273.1 |

24,437.8 |

22,943.7 |

1,041.7 |

4,456.4 |

5,390.9 |

0.5 |

337.4 |

|

SORGHUM |

262.5 |

2,355.2 |

2,752.5 |

37.8 |

263.6 |

463.5 |

0.0 |

0.0 |

|

SOYBEANS |

2,878.4 |

23,431.6 |

33,926.3 |

2,207.3 |

5,836.5 |

11,423.2 |

0.0 |

19.8 |

|

SOY |

240.4 |

3,777.0 |

3,593.0 |

216.8 |

517.8 |

348.1 |

6.1 |

36.6 |

|

SOY |

3.0 |

99.5 |

193.7 |

8.0 |

8.5 |

21.5 |

0.1 |

0.1 |

|

RICE |

|

|

|

|

|

|

|

|

|

|

67.4 |

285.7 |

525.2 |

2.2 |

238.1 |

125.6 |

0.0 |

0.0 |

|

|

0.0 |

7.3 |

21.3 |

0.2 |

1.9 |

7.6 |

0.0 |

0.0 |

|

|

5.8 |

9.1 |

12.0 |

0.5 |

15.5 |

9.4 |

0.0 |

0.0 |

|

|

0.1 |

54.3 |

20.6 |

0.1 |

14.2 |

27.9 |

0.0 |

0.0 |

|

|

3.9 |

77.4 |

47.8 |

62.2 |

204.3 |

88.5 |

0.0 |

0.0 |

|

|

4.4 |

69.6 |

113.5 |

2.9 |

75.4 |

80.0 |

0.0 |

0.0 |

|

|

81.4 |

503.3 |

740.4 |

68.1 |

549.4 |

339.0 |

0.0 |

0.0 |

|

COTTON |

|

THOUSAND |

||||||

|

UPLAND |

391.8 |

6,155.7 |

5,761.9 |

117.4 |

1,853.2 |

2,699.1 |

63.9 |

816.3 |

|

|

23.9 |

184.7 |

254.6 |

5.4 |

74.4 |

123.2 |

0.0 |

0.0 |

This

summary is based on reports from exporters for the period October 8-14, 2021.

Wheat: Net

sales of 362,400 metric tons (MT) for 2021/2022 were down 36 percent from the previous week and 6 percent from the prior 4-week average. Increases primarily for Nigeria (98,000 MT), Japan (92,100 MT), Colombia (76,100 MT, including 31,000 MT switched from

unknown destinations), Thailand (52,200 MT), and Venezuela (33,000 MT, including 30,000 MT switched from unknown destinations), were offset by reductions for unknown destinations (36,100 MT). Exports of 160,200 MT were down 65 percent from the previous week

and 66 percent from the prior 4-week average. The destinations were primarily to Mexico (41,700 MT), Venezuela (33,000 MT), Colombia (32,100 MT), South Korea (30,300 MT), and Taiwan (17,600 MT).

Corn:

Net sales of 1,273,100 MT for 2021/2022 were up 22 percent from the previous week and 67 percent from the prior 4-week average. Increases primarily for unknown destinations (456,700 MT), Mexico (377,100 MT, including decreases of 39,300 MT), Japan (230,100

MT, including 114,400 MT switched from unknown destinations, decreases of 62,000 MT, and 55,000 MT – late), Colombia (111,500 MT, including 59,000 MT switched from unknown destinations and decreases of 31,500 MT), and Nicaragua (76,000 MT), were offset by

reductions for Guatemala (15,300 MT). Total net sales of 500 MT for 2022/2023 were for Canada.

Exports of 1,041,700 MT were up 14 percent from the previous week and 36 percent from the prior 4-week average. The destinations were primarily to Mexico (447,500 MT), Japan (176,200 MT), China (143,100 MT), Colombia (93,600 MT), and Guatemala (65,100

MT).

Optional

Origin Sales:

For 2021/2022, new optional origin sales of 89,800 MT were reported for South Korea (65,000 MT) and Italy (24,800 MT). Decreases totaling 50,000 MT were reported for unknown destinations. The current outstanding balance of 339,800 MT is for unknown destinations

(250,000 MT), South Korea (65,000 MT), and Italy (24,800 MT).

Late

Reporting: For

2021/2022, net sales totaling 55,000 MT of corn were reported late for Japan.

Barley:

No net sales were reported for the week. Exports of 700 MT were unchanged from the previous week, but up noticeably from the prior 4-week average. The destination was to Japan.

Sorghum:

Net sales of 262,500 MT for 2021/2022 were up noticeably from the previous week and from the prior 4-week average. Increases were reported for China (127,300 MT), unknown destinations (103,000 MT), and Eritrea (32,200 MT, including 30,000 MT switched from

unknown destinations). Exports of 37,800 MT were down 39 percent from the previous week and 32 percent from the prior 4-week average. The destinations were primarily to Eritrea (32,200 MT) and China (3,100 MT).

Rice:

Net

sales of 81,400 MT for 2021/2022–a marketing-year high–were up noticeably from the previous week and up 54 percent from the prior 4-week average. Increases primarily for Mexico (47,800 MT), Honduras (17,100 MT), El Salvador (9,000 MT), Jordan (3,700 MT),

and Canada (2,600 MT), were offset by reductions primarily for Iraq (7,100 MT). Exports of 68,100 MT were up noticeably from the previous week and up 79 percent from the prior 4-week average. The destinations were primarily to Iraq (32,900 MT), Haiti (25,600

MT), Canada (4,000 MT), Mexico (3,100 MT), and Jordan (1,000 MT).

Exports

for Own Account:

For 2021/2022, the current exports for own account outstanding balance is 100 MT, all Canada.

Soybeans:

Net sales of 2,878,400 MT for 2021/2022 were up noticeably from the previous week and from the prior 4-week average. Increases were primarily for China (1,884,400 MT, including 526,000 MT switched from unknown destinations, decreases of 6,300 MT, and 54,000

MT – late), unknown destinations (568,800 MT), the Netherlands (127,300 MT, including 124,000 MT switched from unknown destinations and decreases of 2,700 MT), Egypt (97,300 MT), and Bangladesh (57,800 MT, including 55,000 MT switched from unknown destinations).

Exports of 2,207,300 MT were up 29 percent from the previous week and up noticeably from the prior 4-week average. The destinations were primarily to China (1,659,500 MT), the Netherlands (127,300 MT), Mexico (97,500 MT), Turkey (66,000 MT), and Japan (63,900

MT).

Export

for Own Account:

For 2021/2022, the current exports for own account outstanding balance is 5,800 MT, all Canada.

Late

Reporting: For

2021/2022, net sales totaling 54,000 MT of soybeans were reported late for China.

Soybean

Cake and Meal:

Net sales of 240,400 MT for 2021/2022 primarily for Ecuador (64,900 MT, including decreases of 100 MT), Canada (49,800 MT, including decreases of 2,000 MT), Denmark (45,000 MT), Colombia (35,100 MT, including 9,200 MT switched from unknown destinations and

decreases of 200 MT), and Nicaragua (18,000 MT), were offset by reductions primarily for Mexico (6,900 MT), Spain (6,000 MT), and Guatemala (4,600 MT). For 2022/2023, net sales of 6,100 MT were reported for Japan (3,600 MT) and the Netherlands (2,500 MT).

Exports of 216,800 MT were primarily to the Philippines (48,700 MT), Colombia (47,300 MT), Guatemala (34,000 MT), Mexico (23,500 MT), and Canada (17,200 MT).

Soybean

Oil:

Net sales of 3,000 MT for 2021/2022 were reported for Mexico (2,200 MT) and the Dominican Republic (800 MT). Total net sales of 100 MT for 2022/2023 were for Canada. Exports of 8,000 MT were to Guatemala (7,500 MT), Mexico (400 MT), and Canada (100 MT).

Cotton:

Net sales of 391,800 RB for 2021/2022 were up noticeably from the previous week and up 20 percent from the prior 4-week average. Increases were primarily for China (272,800 RB, including decreases of 100 RB), Turkey (76,900 RB), Vietnam (15,800 RB, including

300 RB switched from Japan), Mexico (6,200 RB), and Bangladesh (5,000 RB, including decreases of 100 RB). Net sales of 63,900 RB for 2022/2023 were primarily for China (50,000 RB) and Turkey (13,200 RB). Exports of 117,400 RB were up 23 percent from the

previous week, but down 16 percent from the prior 4-week average. The destinations were primarily to China (46,400 RB), Mexico (18,700 RB), Turkey (11,900 RB), Pakistan (9,600 RB), and Bangladesh (8,500 RB). Net sales of Pima totaling 23,900 RB–a marketing-year

high–were up noticeably from the previous week and up 58 percent from the prior 4-week average. Increases were primarily for India (17,000 RB), Peru (2,800 RB, including decreases of 300 RB), and China (1,800 RB). Exports of 5,400 RB were down 49 percent

from the previous week and 28 percent from the prior 4-week average. The destinations were primarily to India (4,500 RB), Austria (500 RB), and Peru (200 RB).

Optional

Origin Sales:

For 2021/2022, the current outstanding balance of 8,800 RB is for Pakistan.

Exports

for Own Account:

For 2021/2022, the current exports for own account outstanding balance of 4,800 RB is for China (4,700 RB) and Vietnam (100 RB).

Hides

and Skins:

Net sales of 415,700 pieces for 2021 were up 62 percent from the previous week and 13 percent from the prior 4-week average. Increases primarily for China (277,700 whole cattle hides, including decreases of 7,900 pieces), South Korea (63,000 whole cattle

hides, including decreases of 1,000 pieces), Thailand (23,700 whole cattle hides, including decreases of 1,000 pieces), Mexico (20,200 whole cattle hides, including decreases of 100 pieces), and Cambodia (10,600 whole cattle hides), were offset by reductions

for Taiwan (1,000 pieces). Exports of 472,100 pieces were up 37 percent from the previous week and 35 percent from the prior 4-week average. Whole cattle hide exports were primarily to China (299,000 pieces), South Korea (53,500 pieces), Thailand (37,300

pieces), Mexico (33,600 pieces), and Taiwan (20,600 pieces).

Net

sales of 150,500 wet blues for 2021 were up noticeably from the previous week and up 22 percent from the prior 4-week average. Increases primarily for China (136,200 unsplit, including decreases of 100 unsplit), Mexico (8,400 grain splits, including decreases

of 400 grain splits), and Italy (7,300 unsplit and 100 grain splits, including decreases of 13,100 unsplit), were offset by reductions for Vietnam (1,300 unsplit), Thailand (200 unsplit), and South Korea (100 grain splits). Net sales of 52,100 wet blues for

2022 were reported for Italy (28,100 unsplit) and Vietnam (24,000 unsplit). Exports of 227,900 wet blues were up 75 percent from the previous week and 72 percent from the prior 4-week average. The destinations were primarily to Italy (88,700 unsplit and

12,500 grain splits), China (77,700 unsplit), Vietnam (16,000 unsplit), Thailand (13,400 unsplit), and South Korea (7,000 grain splits and 1,600 unsplit). Total net sales of 48,200 splits were reported for China, including decreases of 4,400 splits. Exports

of 335,200 pounds were to China (255,200 pounds) and Vietnam (80,000 pounds).

Beef:

Net

sales of 7,800 MT reported for 2021–a marketing-year low–were down 50 percent from the previous week and 51 percent from the prior 4-week average. Increases were primarily for Japan (2,300 MT, including decreases of 300 MT), China (1,600 MT, including decreases

of 200 MT), South Korea (1,100 MT, including decreases of 400 MT), Taiwan (1,100 MT, including decreases of 100 MT), and Mexico (300 MT, including decreases of 200 MT). Net sales reductions of 200 MT for 2022 resulting in increases primarily for Chile (200

MT) and Indonesia (100 MT), were more than offset by reductions for South Korea (500 MT). Exports of 17,100 MT were up 10 percent from the previous week, but unchanged from the prior 4-week average. The destinations were primarily to South Korea (5,400 MT),

Japan (4,000 MT), China (3,000 MT), Mexico (1,400 MT), and Taiwan (1,100 MT).

Pork:

Net

sales of 20,900 MT reported for 2021 were down 38 percent from the previous week and 36 percent from the prior 4-week average. Increases primarily for Mexico (10,200 MT, including decreases of 500 MT), South Korea (3,700 MT, including decreases of 300 MT),

Japan (3,200 MT, including decreases of 200 MT), Colombia (800 MT, including decreases of 300 MT), and the Dominican Republic (800 MT), were offset by reductions for Bahamas (200 MT) and New Zealand (100 MT). Net sales of 1,400 MT for 2022 were primarily

for Chile (1,300 MT). Exports of 32,800 MT were up 11 percent from the previous week and 5 percent from the prior 4-week average. The destinations were primarily to Mexico (15,000 MT), Japan (4,400 MT), China (4,100 MT), Colombia (2,700 MT), and Canada (1,800

MT).

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.