PDF attached

USDA:

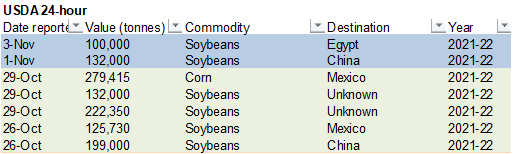

Private exporters reported sales of 100,000 metric tons of soybeans for delivery to Egypt during the 2021/2022 marketing year.

CBOT

prices traded lower, sharply lower for some markets, on a higher USD, weakness in outside commodity markets and positioning ahead of USDA’s November S&D November 99th update.

![]()

World

Weather Inc.

MOST

IMPORTANT WEATHER AROUND THE WORLD

- Unusually

cold air is over far eastern Russia, Mongolia and Xinjiang China and will remain in place through the weekend with some advancement into northeastern China over time - Temperatures

will be at record cold levels in some of this region for this time of year this weekend into early next week - A

major snowstorm is expected to impact northeastern China as the cold air comes into the region beginning Friday in Inner Mongolia and spreading southeast into the Northeast Provinces during the weekend.

- Snowfall

of 10-20 inches is possible in a part of northeastern China and blizzard or near blizzard conditions will be possible - Cold

rain and sleet are also expected - Travel

disruptions, power outages and some death to livestock and people will be possible - The

advertised storm in the forecast model data may be overdone and some moderation is possible over the next couple of days

- The

biggest concern will be to transportation and livestock health - The

coldest air should remain over eastern Russia and only a part of it will reach into northeastern China – just enough to induce the snowstorm - Eastern

Argentina, Uruguay, southern Paraguay and far southern Brazil continue to see an evolving forecast pattern of limited rainfall - This

fits well with the increasing La Nina influence and from the 22-year and 18-year cycles - Expect

dryness in these areas to be a festering feature this month and in December with a few breaks possible - Frequent

Brazil rain of significance will occur in the next ten days from eastern Mato Grosso, Tocantins and parts of northeastern Goias into Minas Gerais and Bahia - Some

of these areas will get greater than usual rainfall and local flooding may evolve next week - No

crop damage is expected, although some planting delay is expected - Brazil’s

best weather is expected from western and southern Mato Grosso through northern and eastern Mato Grosso do Sul where a good mix of rain and sunshine is expected over the next two weeks - Net

drying in Sao Paulo and parts northern Parana, Brazil will be closely monitored during the next ten days; the region could become a little too dry in time - U.S.

harvest weather will be nearly ideal through Tuesday of next week, although some showers will develop in the central parts of the nation on Tuesday - The

next more generalized precipitation event will be in the Midwest Wednesday through Friday of next week and a few showers from the same storm will also impact parts of the Delta and southeastern states briefly late in the week - Dry

weather will resume for many of these areas after Nov. 12 - West

Texas will be mostly dry over the next two weeks favoring cotton and other late season crop harvest progress - West-central

and southwestern parts of the U.S. Plains are expecting little to no rain for much of the next ten days to two weeks which is to be expected with intensifying La Nina conditions - Limited

precipitation is still expected in the northwestern U.S. Plains and central parts of Canada’s Prairies over the next ten days, but these areas will eventually have some potential for rain and snow as La Nina becomes more significant - Waves

of rain will occur frequently from northern California through the Cascade Mountains and coastal areas of Washington and Oregon during the next ten days to two weeks - Limited

precipitation will impact the San Joaquin Valley, southwestern desert region and southern U.S. Rocky Mountains during the next two weeks - Some

snow and rain will impact the southern Sierra Nevada, but resulting moisture will be lighter than usual - Temperatures

in central and interior western parts of North America will rise well above average briefly late this week into early next week followed by some cooling late next week - Southern

California and the southwestern desert region will continue dry biased for the next two weeks - Australia’s

rain frequency will be rising in the south and eastern parts of the nation during the next two weeks

- The

moisture boost will be great for summer crop planting, emergence and establishment, but the moisture will slow winter crop maturation and harvest progress - No

crop quality concerns are expected for a while, but a close watch on the harvest and rainfall will be warranted until wheat, barley and canola harvesting is complete - Southern

India will turn much wetter over the next week to ten days - The

precipitation will slow summer crop maturation and harvest progress and could raise a little cotton, rice and oilseed quality concern - The

wettest areas will include Andhra Pradesh, Tamil Nadu Kerala and Karnataka, although rain will fall in Maharashtra as well - Sugarcane

and coffee will benefit from the moisture - A

tropical cyclone may evolve in the eastern Arabian Sea later this week to the west of India.

- The

storm should stay over open water in the Arabian Sea, although it will spin a few waves of rain into the west coast of India through next week.

- The

storm’s movement is very questionable in today’s forecast models meaning there is still potential for the system to more significantly impact India, Pakistan, Oman or other areas in the Arabian Sea coastal areas

- Another

tropical cyclone is advertised to form in the Bay of Bengal Monday that is advertised to reach the lower east coast of India late next week and if this storm verifies it may produce some heavy rain in Andhra Pradesh, Telangana and/or Odisha - A

more active weather pattern in Russia during the coming two weeks will lead to a boost in snow cover for many areas in the north and central parts of the nation - Locally

heavy snow is possible in northern and eastern parts of Russia’s crop region and in most of the Ural Mountains - Ukraine

and southern Russia grain areas will receive some periods of rain during the week next week and into the following weekend - The

moisture will be good for use in the spring - Europe

weather will be favorable for fieldwork of all kinds, although it will have to advance around brief bouts of light rainfall - South

Africa will start receiving some needed rain in the central and eastern summer crop areas this weekend and next week that will eventually bring on a soil moisture boost - The

moisture will improve planting, germination and emergence conditions, although the distribution will not be uniform and many western crop areas will stay dry biased - Temperatures

will be warmer than usual in the northeast and slightly below average in the southwest through the next week - Northeastern

Xinjiang, China will experience some snow over the next couple of days disrupting any late season harvesting that may still under way

- An

extended period of drier weather will then occur from this weekend through most of next week to help get harvest back under way if it is not fully complete - Central

and western Xinjiang harvest weather will be nearly ideal during the next couple of weeks with only a few brief showers of insignificance expected late this week - Indonesia

and Malaysia weather will be wet biased over the next two weeks with frequent rain expected over saturated or nearly saturated soil causing some flooding - Coastal

areas of southern Vietnam will likely trend wetter than usual next week, but restricted rainfall is expected until then - Some

of the heavy rain may eventually push into the Central Highlands of Vietnam, but confidence is low

- Philippines

weather will remain favorably mixed with rain and sunshine through the next two weeks - Portions

of North Africa will get some needed rain late this week through the weekend - Northwestern

Algeria may get some excessive rain resulting in some coastal flooding - Northwestern

Algeria has been drier than usual in recent past years and this will be a good opportunity to improve soil moisture and water supply ahead of aggressive wheat and barley planting - Southwestern

Morocco remains in a multi-year drought with little rain of significance expected over the next couple of weeks - West-central

Africa will experience a good mix of weather during the next ten days to two weeks - Less

frequent rain in cotton areas will translate into better crop maturation conditions - Coffee,

cocoa, sugarcane and rice will also benefit from less frequent and less significant rainfall, although completely dry weather is not likely for a while - East-central

Africa rainfall will be favorably mixed for a while supporting coffee, rice, cocoa and a host of tropical crops - Mexico’s

weather will turn drier in the southwest leaving most of the nation with a good environment for crop maturation and harvesting

- Some

showers will occur along the east coast - Most

other areas will experience seasonal drying - Central

America rainfall will be erratic over the next two weeks with the greatest rain expected in Costa Rica and Panama - Western

and northern Colombia, Ecuador and Peru agricultural areas will be closely monitored over the next few weeks as the potential for flooding increases.

- The

risk may be greatest starting in the second week of the forecast and continuing into mid-November.

- Coffee,

sugarcane, corn and a host of other crops may eventually impacted by too much rain in Colombia

- Western

Venezuela may also be involved with the excessive moisture - Central

Asia cotton and other crop harvesting will advance swiftly as dry and warm conditions prevail - Today’s

Southern Oscillational Index was +6.48 and it was expected to drift a little higher over the coming week - New

Zealand weather is expected to be drier than usual during the coming week - Temperatures

will be seasonable. - Nov.

12-18 will trend wetter in western parts of South Island - Tropical

Storm Wanda was 705 miles west northwest of the Azores and expected to move closer to the islands this weekend - The

storm poses no threat to North America and will merge with a mid-latitude cold front next week while bringing rain to northwestern Europe

Thursday,

Nov. 4:

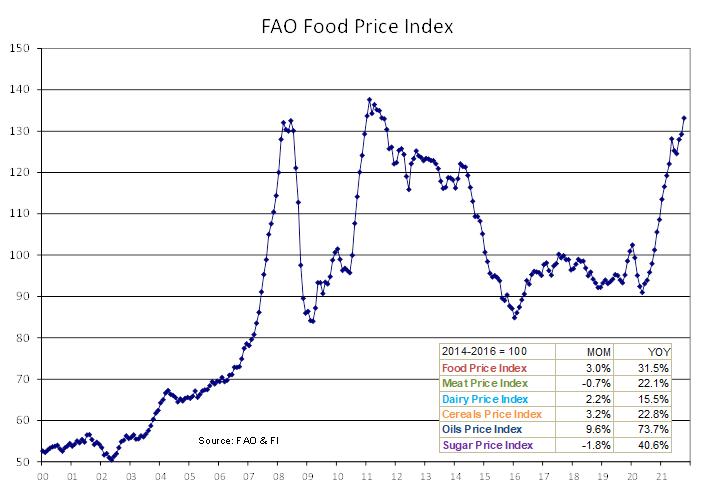

- FAO

World Food Price Index - USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - New

Zealand Commodity Price, 8pm Wednesday ET time - Port

of Rouen data on French grain exports - HOLIDAY:

India, Malaysia, Singapore

Friday,

Nov. 5:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - China’s

CNGOIC to publish demand-supply reports on corn, soy and other commodities - FranceAgriMer

weekly update on crop conditions - Malaysia

Nov. 1-5 palm oil exports - HOLIDAY:

India

Source:

Bloomberg and FI

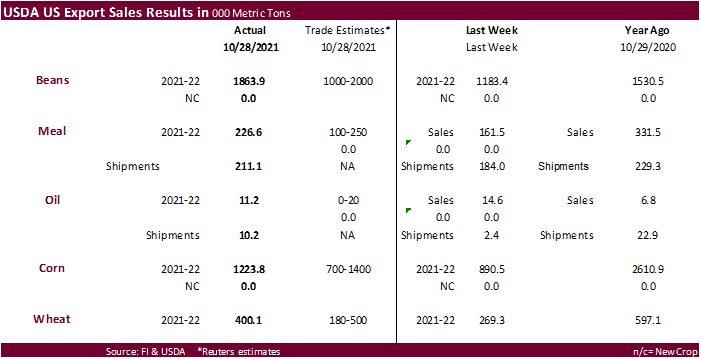

USDA

Export Sales

Sales

were reported at the high end of a range of expectations for the soybean complex, corn, and wheat. Soybean sales of 1.86 million tons included 1.2 million tons, but 510,000 tons of this was switched from unknow. Soybean commitments are running 33 percent

below the previous year’s pace and represent 57 percent of USDA’s export projection. Soybean meal sales were 2266,600 tons and shipments were good at 211,100 tons. Soybean oil sales of 11,200 tons were down slightly from the previous week, and shipments

were 10,200 tons, an improvement. USDA corn export sales of 1.224 million tons surprised us with the lack of 24-hour announcements for the week ending October 28 and included regular importing countries (no China). Corn commitments are running 7 percent

below year ago and sales are running 49 percent of USDA’s export projection. Sorghum sales were an impressive 265,600 tons including 268,500 tons for China (unknown decrease of 3,000). All-wheat sales improved 400,100 tons from 269,300 tons previous week.

US

Initial Jobless Claims Oct 30: 269K (est 275K; prev 281K; prevR 283K)

–

Continuing Jobless Claims Oct 23: 2.105M (prev 2.243M; prevR 2.239M)

US

Labour Costs Q3 P: 8.3% (est 7.0%; prev 1.3%)

US

International Trade $ Sep: -80.9B (est -80.5B; prev -73.3B)

Canada

Trade Balance Sep: 1.86B (est 1.55B; prev 1.94B)

US

Mortgage Rates Slip To 3.09% For First Drop In Four Weeks

US

EIA NatGas Storage Change (BCF) Oct 29: +63 (est +66; prev +87)

–

Salt Dome Cavern NatGas Stocks (BCF): +16 (prev +21)

73

Counterparties Take $1.349 Tln At Fed’s Fixed Rate Reverse Repo (prev $1.343 Tln, 74 Bidders)

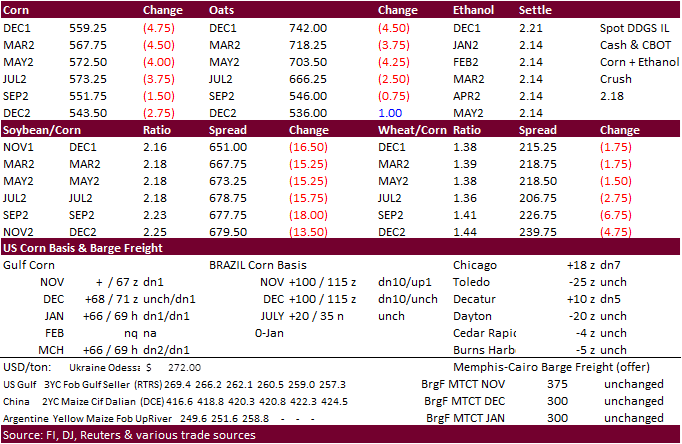

Corn

·

Corn futures started higher on technical buying, rebound in WTI crude oil, and higher wheat, but prices eroded after soybeans extended losses. Positioning was noted. December corn ended 4.75 cents lower, a one-week low. USDA

export sales were good.

·

Funds sold an estimated net 5,000 corn contracts.

·

Goldman roll for December contacts starts Friday.

·

China mentioned their sow herd was 6 percent higher than normal. Production may cool due to higher feed costs.

Export

developments.

-

None

reported

Updated

11/01/21

December

corn is seen in a $5.30-$6.10 range

March

corn is seen in a $5.25-$6.25 range

·

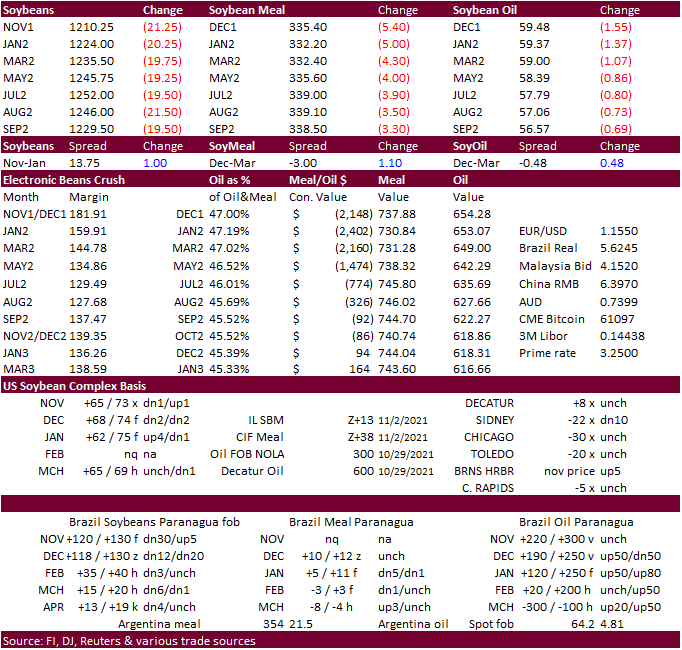

CBOT soybeans ended sharply lower on fund selling and early positioning ahead of the USDA October USDA report, despite good export sales. The USD rallied 47 points. Energy markets were mostly lower. Soybean meal finished $3.10-$5.00

lower, and soybean oil finished 73-145 points lower. Bear spreading was a feature. Soybean oil started higher

but

the selloff in meal and soybeans triggered selling. Many end users are covered for soybean oil through early next year, one reason for weakness in the front months. December SBO briefly broke below its 50-day MA of 59.44, and closed below that level, a bearish

signal. For long term traders, we see any breaks in soybean oil as a buying opportunity as renewable fuel production will ramp up in 2022 but may want to wait to see if we see additional selling over the short term.

·

Funds ended up selling an estimated net 16,000 soybean contracts, 5,000 soybean meal and 6,000 soybean oil.

·

Census US soybean exports were 80 million bushels, well above inspections that stood at 67.3 million bushels, an unusual discrepancy and likely a result from collecting data during and shortly after the hurricane. We will leave

our US soybean export projection unchanged at 2.060 billion bushels, 30 million below USDA. This takes into account normal Brazil planting progress, with the US export window winding down by early February.

·

Malaysia was on holiday.

·

Argentina soybean plantings were reported by the BA Grains Exchange at 7 percent complete, 33 points above the previous week and 3 points above this time last year.

·

Argentina has a chance for showers, but precipitation amounts will remain well below normal.

-

China’s

non-genetically modified soybeans used in foods such as tofu instead of animal feed have climbed to the highest level on record. (Bloomberg). The contract started in 2002.

Export

Developments

·

Under the 24-hour announcement system, private exporters sold 100,000 tons of soybeans to Egypt for 2021-22 crop year.

Updated

11/4/21

Soybeans

– January $11.80-$13.25 range, March $11.50-$13.50

Soybean

meal – December $315-$360, March $310-$360

Soybean

oil – December 58.25-62.50 cent range (down 125 & 50, respectively),

March 56-65

·

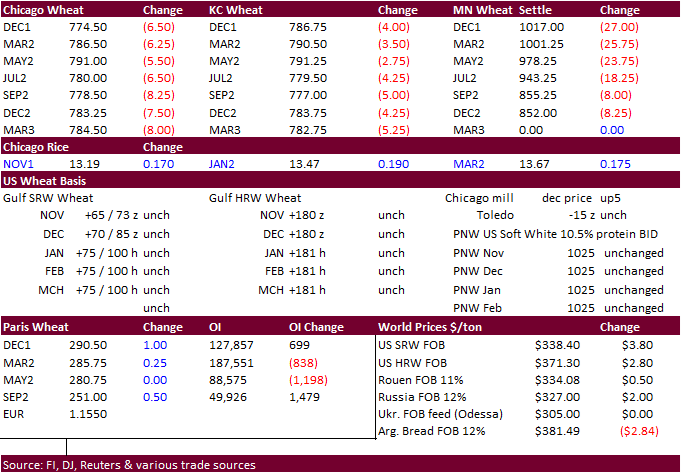

US wheat futures started higher but ended lower led by a large decline in Minneapolis front month contracts. The higher USD and widespread commodity selling pressured prices. Some noted Minneapolis wheat was overbought and needed

a pull back.

·

There is some concern over US wheat conditions bias US southwest and parts of the central Great Plains that missed out on rains this week. Too much rain threatening wheat quality for the eastern Australia wheat crop is also supportive.

·

Funds sold an estimated net 5,000 Chicago soft red winter wheat contracts.

·

USDA export sales improved from the previous week.

·

China traders there were concerned over tight wheat stocks might have been relieved after the government mentioned wheat stocks were sufficient for 1.5 years. They went onto say China vegetable oil production was “basically normal.”

·

Paris December wheat was up 1.00 euros at 290.

·

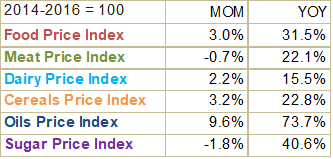

The World Food Price Index hit a 10-year high in October led by the rapid increase of vegetable oils.

Export

Developments.

-

Pakistan

received offers for 90,000 tons of wheat

for Jan through April shipment. Lowest offer was believed to be $407.38 a ton, cost and freight (c&f) included. -

Jordan

passed on barley. -

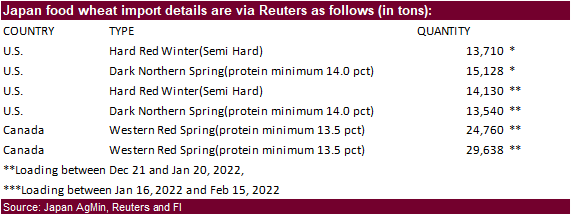

Japan

bought 143,396

tons of food

wheat. Original details as follows.

·

Ethiopia seeks 300,000 tons of milling wheat on November 9.

·

Ethiopia seeks 400,000 tons of wheat on November 30.

Rice/Other

·

(Bloomberg) — U.S. 2021-22 cotton ending stocks seen at 3.16m bales, 38,000 bales below USDA’s previous est., according to the avg in a Bloomberg survey of nine analysts.

Estimates

range from 2.9m to 3.5m bales

Global

ending stocks seen 48,000 bales lower at 87.08m bales

Updated

11/01/21

December

Chicago wheat is seen in a $7.30‐$8.25 range, March $7.25-$8.40

December

KC wheat is seen in a $7.35‐$8.35, March $7.00-$8.50

December

MN wheat is seen in a $9.70‐$11.50, March $9.00-$11.75

U.S. EXPORT SALES FOR WEEK ENDING 10/28/2021

FAX 202-690-3275

|

|

CURRENT MARKETING YEAR |

NEXT MARKETING YEAR |

||||||

|

COMMODITY |

NET SALES |

OUTSTANDING SALES |

WEEKLY EXPORTS |

ACCUMULATED EXPORTS |

NET SALES |

OUTSTANDING SALES |

||

|

CURRENT YEAR |

YEAR |

CURRENT YEAR |

YEAR |

|||||

|

|

THOUSAND METRIC TONS |

|||||||

|

WHEAT |

|

|

|

|

|

|

|

|

|

HRW |

206.0 |

1,887.2 |

1,633.2 |

62.7 |

3,272.9 |

4,484.4 |

0.0 |

0.0 |

|

SRW |

54.2 |

600.0 |

418.6 |

27.0 |

1,308.4 |

937.7 |

0.0 |

0.0 |

|

HRS |

73.0 |

1,025.4 |

1,616.6 |

45.8 |

2,427.5 |

3,108.5 |

0.0 |

0.0 |

|

WHITE |

66.9 |

728.7 |

1,936.2 |

0.9 |

1,607.5 |

2,080.8 |

0.0 |

0.0 |

|

DURUM |

0.0 |

72.4 |

200.9 |

0.0 |

77.3 |

340.0 |

0.0 |

0.0 |

|

TOTAL |

400.1 |

4,313.6 |

5,805.5 |

136.4 |

8,693.6 |

10,951.4 |

0.0 |

0.0 |

|

BARLEY |

0.0 |

22.8 |

31.1 |

0.1 |

7.3 |

10.9 |

0.0 |

0.0 |

|

CORN |

1,223.8 |

25,115.0 |

26,335.3 |

748.5 |

5,893.5 |

6,853.9 |

0.0 |

337.4 |

|

SORGHUM |

265.6 |

2,748.0 |

3,027.0 |

3.7 |

269.4 |

614.8 |

0.0 |

0.0 |

|

SOYBEANS |

1,863.9 |

21,422.7 |

31,853.2 |

2,650.5 |

10,892.7 |

16,578.6 |

0.0 |

19.8 |

|

SOY MEAL |

226.6 |

3,769.9 |

3,596.4 |

211.1 |

912.9 |

875.5 |

-0.2 |

36.9 |

|

SOY OIL |

11.2 |

112.7 |

174.2 |

10.2 |

21.1 |

53.8 |

0.0 |

0.1 |

|

RICE |

|

|

|

|

|

|

|

|

|

L G RGH |

11.9 |

222.3 |

464.5 |

30.4 |

315.9 |

215.2 |

0.0 |

0.0 |

|

M S RGH |

0.0 |

6.8 |

20.4 |

0.2 |

2.3 |

8.5 |

0.0 |

0.0 |

|

L G BRN |

0.1 |

8.4 |

11.3 |

0.2 |

16.4 |

10.3 |

0.0 |

0.0 |

|

M&S BR |

0.1 |

54.3 |

18.7 |

0.1 |

14.4 |

29.8 |

0.0 |

0.0 |

|

L G MLD |

2.5 |

86.3 |

87.1 |

2.5 |

218.5 |

112.7 |

0.0 |

0.0 |

|

M S MLD |

15.3 |

67.6 |

146.6 |

16.8 |

94.6 |

103.9 |

0.0 |

0.0 |

|

TOTAL |

29.8 |

445.6 |

748.8 |

50.2 |

662.1 |

480.5 |

0.0 |

0.0 |

|

COTTON |

|

THOUSAND RUNNING BALES |

||||||

|

UPLAND |

139.1 |

6,450.3 |

5,667.3 |

141.9 |

2,058.5 |

3,197.9 |

20.6 |

856.9 |

|

PIMA |

31.8 |

215.2 |

266.3 |

7.6 |

84.2 |

161.0 |

1.8 |

1.8 |

This

summary is based on reports from exporters for the period October 22-28, 2021.

Wheat: Net

sales of 400,100 metric tons (MT) for 2021/2022 were up 49 percent from the previous week and 4 percent from the prior 4-week average. Increases primarily for Mexico (101,400 MT, including decreases of 26,000 MT), South Korea (50,000 MT), Taiwan (48,400 MT),

unknown destinations (31,700 MT), and Japan (30,300 MT), were offset by reductions for China (100 MT). Exports of 136,400 MT were down 27 percent from the previous week and 60 percent from the prior 4-week average. The destinations were primarily to Mexico

(27,000 MT), Panama (24,600 MT), Honduras (23,400 MT), Jamaica (22,500 MT), and Canada (17,800 MT).

Corn:

Net sales of 1,223,800 MT for 2021/2022 were up 37 percent from the previous week and 10 percent from the prior 4-week average. Increases primarily for Mexico (666,300 MT, including decreases of 18,300 MT), Japan (114,900 MT, including 50,900 MT switched

from unknown destinations and decreases of 15,500 MT), Guatemala (105,400 MT), Colombia (77,500 MT, including 50,000 MT switched from unknown destinations), and Saudi Arabia (74,000 MT), were offset by reductions for unknown destinations (12,900 MT) and Panama

(1,800 MT). Exports of 748,500 MT were up 9 percent from the previous week, but down 17 percent from the prior 4-week average. The destinations were primarily to Mexico (317,300 MT), Japan (162,900 MT), Colombia (136,200 MT), Venezuela (43,600 MT), and Nicaragua

(26,300 MT).

Optional

Origin Sales:

For 2021/2022, new optional origin sales of 29,000 MT were reported for Italy (20,000 MT) and unknown destinations (9,000 MT). The current outstanding balance of 508,300 MT is for unknown destinations (379,000 MT), South Korea (65,000 MT), Italy (55,300 MT),

and Saudi Arabia (9,000 MT).

Barley:

No net sales were reported for the week. Exports of 100 MT were down 92 percent from the previous week and 90 percent from the prior 4-week average. The destination was to Taiwan.

Sorghum:

Net sales of 265,600MT for 2021/2022 resulting in increases for China (268,500 MT) and Japan (100 MT), were offset by reductions for unknown destinations (3,000 MT). Exports of 3,700 MT were up 77 percent from the previous week, but down 90 percent from the

prior 4-week average. The destination was primarily to China (2,300 MT).

Rice:

Net

sales of 29,800 MT for 2021/2022 were up 19 percent from the previous week, but down 44 percent from the prior 4-week average. Increases were primarily for Japan (13,000 MT), Guatemala (10,200 MT), Canada (1,700 MT), Mexico (1,500 MT), and Honduras (1,300

MT). Exports of 50,200 MT were down 20 percent from the previous week and 4 percent from the prior 4-week average. The destinations were primarily to Honduras (21,800 MT), Japan (13,000 MT), Mexico (9,200 MT), Canada (2,200 MT), and Jordan (2,100 MT).

Exports

for Own Account:

For 2021/2022, new exports for own account totaling 100 MT were to Canada. The current exports for own account outstanding balance is 200 MT, all Canada.

Soybeans:

Net sales of 1,863,900 MT for 2021/2022 were up 58 percent from the previous week and 19 percent the prior 4-week average. Increases primarily for China (1,207,300 MT, including 510,000 MT switched from unknown destinations and decreases of 14,000 MT), Mexico

(157,400 MT, including decreases of 1,100 MT), the Netherlands (142,100 MT, including 120,000 MT switched from unknown destinations and decreases of 3,900 MT), Egypt (140,500 MT, including decreases of 1,600 MT), and Spain (92,900 MT, including 64,000 MT switched

from China and 26,000 MT switched unknown destinations), were offset by reductions for unknown destinations (137,600 MT). Exports of 2,650,500 MT were up 10 percent from the previous week and 46 percent from the prior 4-week average. The destinations were

primarily to China (1,864,500 MT), Mexico (178,600 MT), the Netherlands (142,100 MT), Spain (92,900 MT), and Egypt (87,100 MT).

Export

for Own Account:

For 2021/2022, new exports for own account totaling 29,800 MT were for Canada. The current exports for own account outstanding balance is 66,400 MT, all Canada.

Soybean

Cake and Meal:

Net sales of 226,600 MT for 2021/2022 primarily for Mexico (71,000 MT), Guatemala (44,200 MT), Morocco (24,000 MT), El Salvador (22,700 MT), and Venezuela (20,500 MT, including 18,000 MT switched from unknown destinations), were offset by reductions primarily

for unknown destinations (18,600 MT). Total net sales reductions of 200 MT for 2022/2023 were for Japan. Exports of 211,100 MT were primarily to Ecuador (40,300 MT), Honduras (34,000 MT), Canada (30,500 MT), Mexico (23,900 MT),

and Venezuela (20,500 MT).

Soybean

Oil:

Net sales of 11,200 MT for 2021/2022 were primarily for Mexico (6,500 MT), Costa Rica (4,000 MT), and Guatemala (500 MT). Exports of 10,200 MT were primarily to Costa Rica (4,200 MT), Jamaica (3,500 MT), Mexico (1,200 MT), and Honduras (1,000 MT).

Cotton:

Net sales of 139,100 RB for 2021/2022 were down 61 percent from the previous week and 51 percent from the prior 4-week average. Increases were primarily for China (44,800 RB, including decreases of 30,400 RB), India (24,300 RB), Turkey (23,700 RB), Vietnam

(18,100 RB), and Peru (13,700 RB). Net sales of 20,600 RB for 2022/2023 reported for Turkey (13,200 RB) and Pakistan (8,800 RB), were offset by reductions for China (1,400 RB). Exports of 141,900 RB were up noticeably from the previous week and up 42 percent

from the prior 4-week average. The destinations were primarily to China (61,100 RB), Mexico (24,400 RB), Pakistan (13,100 RB), Turkey (7,400 RB), and El Salvador (6,900 RB). Net sales of Pima totaling 31,800 RB–a marketing-year high–were up noticeably

from the previous week and from the prior 4-week average. Increases were primarily for Vietnam (8,700 RB), India (7,900 RB, including decreases of 400 RB), China (7,300 RB), Pakistan (3,700 RB), and Turkey (2,200 RB). Total net sales of 1,800 RB for 2022/2023

were for Egypt. Exports of 7,600 RB were up noticeably from the previous week and up 39 percent from the prior 4-week average. The destinations were primarily to India (5,400 RB), Peru (1,600 RB), and Thailand (400 RB).

Optional

Origin Sales:

For 2021/2022, the current outstanding balance of 8,800 RB is for Pakistan.

Exports

for Own Account:

For 2021/2022, the current exports for own account totaling 4,700 RB to China were applied to new or outstanding sales. The outstanding balance of 100 RB is for Vietnam.

Hides

and Skins:

Net sales of 463,500 pieces for 2021 were down 18 percent from the previous week, but up 3 percent from the prior 4-week average. Increases primarily for China (378,400 whole cattle hides, including decreases of 17,000 pieces), South Korea (36,200 whole cattle

hides, including decreases of 1,200 pieces), Thailand (25,700 whole cattle hides, including decreases of 400 pieces), Indonesia (9,600 whole cattle hides), and Mexico (8,500 whole cattle hides, including decreases of 3,300 pieces), were offset by reductions

primarily for Cambodia (4,800 pieces). Net sales of 6,200 pieces for 2022 were reported for China (3,600 whole cattle hides) and Mexico (2,600 whole cattle hides). Total net sales reductions of 2,800 calf skins were for Italy. In addition, total net sales

of 1,400 kip skins were for Italy. Exports of 402,400 pieces were down 1 percent from the previous week and 7 percent from the prior 4-week average. Whole cattle hide exports were primarily to China (261,800 pieces), South Korea (58,300 pieces), Mexico (31,200

pieces), Thailand (29,700 pieces), and Brazil (13,600 pieces).

Net

sales of 92,400 wet blues for 2021 were down 57 percent from the previous week and 37 percent from the prior 4-week average. Increases primarily for Italy (47,900 unsplit, 100 grain splits, and decreases of 200 grain splits), Thailand (20,200 unsplit), China

(13,700 unsplit), Vietnam (10,500 unsplit), and Mexico (1,300 unsplit, including decreases 3,000 unsplit and 200 grain splits), were offset by reductions for Brazil (1,800 unsplit). Net sales reductions of 200 wet blues for 2022 resulting in increases for

Mexico (3,000 unsplit) and Italy (1,600 unsplit), were more than offset by reductions for Vietnam (4,800 unsplit). Exports of 134,200 wet blues were up 7 percent from the previous week, but down 13 percent from the prior 4-week average. The destinations

were primarily to China (46,600 unsplit), Italy (30,100 unsplit and 11,300 grain splits), Vietnam (29,400 unsplit), Mexico (5,000 grain splits and 4,300 unsplit), and Thailand (6,200 unsplit). Net sales of 961,900 splits were for Vietnam (960,000 splits)

and China (1,900 splits). Exports of 242,900 pounds were to Vietnam (200,000 pounds) and China (42,900 pounds).

Beef:

Net

sales of 16,700 MT for 2021 were down 13 percent from the previous week, but up 15 percent from the prior 4-week average. Increases were primarily for South Korea (6,700 MT, including decreases of 500 MT), China (2,800 MT, including decreases of 100 MT),

Japan (2,200 MT, including decreases of 500 MT), Taiwan (1,600 MT, including decreases of 100 MT), and Canada (1,000 MT, including decreases of 100 MT). Net sales of 3,500 MT for 2022 were primarily for South Korea (2,700 MT) and Japan (700 MT). Exports

of 16,800 MT were unchanged from the previous week, but up 3 percent from the prior 4-week average. The destinations were primarily to South Korea (4,600 MT), Japan (4,500 MT), China (3,100 MT), Taiwan (1,100 MT), and Mexico (1,100 MT).

Pork:

Net

sales of 45,700 MT for 2021 were up 55 percent from the previous week and 72 percent from the prior 4-week average. Increases primarily for Mexico (18,500 MT, including decreases of 500 MT), China (16,000 MT, including decreases of 300 MT), Japan (3,500 MT,

including decreases of 200 MT), Canada (2,500 MT, including decreases of 400 MT), and South Korea (2,000 MT, including decreases of 1,100 MT), were offset by reductions for Chile (700 MT). Net sales of 400 MT for 2022 were reported for Japan. Exports of

33,800 MT were up 3 percent from the previous week and 9 percent from the prior 4-week average. The destinations were primarily to Mexico (15,800 MT), China (4,400 MT), Japan (4,300 MT), Colombia (2,800 MT), and South Korea (2,300 MT).

Export

Adjustment:

Accumulated exports of pork to the Dominican Republic were adjusted down 3 MT for week ending

October 21st. This shipment was reported in error.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.