PDF attached

USDA released their March Prospective Plantings and March 1 Grain Stocks reports

Reaction: Bearish soybeans, supportive for corn and wheat.

USDA NASS briefing

https://www.nass.usda.gov/Newsroom/Executive_Briefings/2022/03-31-2022.pdf

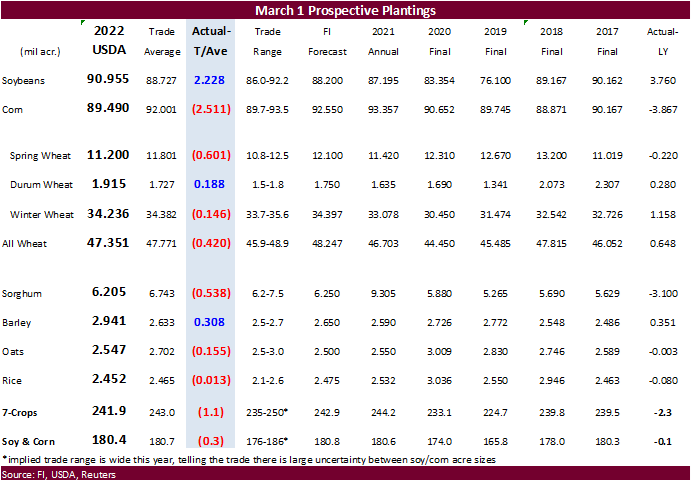

Acreage for the 7 major row crops (excluding cotton) came in less than expected by only 0.3 million acres. Corn acres were by far the largest surprise, coming in at only 89.490 million, 2.5 million below trade expectations. Soybeans of 91 million were also a surprise as they came in 2.2 million above an average trade guess. The soybean area is higher than corn, second time in history, behind 2018 when a wet spring forced producers to switch from corn to soybeans. This year we think corn acres were lost in several areas as producers opted to plant other commodities, including tobacco and cotton. Sorghum at 6.2 million acres were below expectations and down roughly 15 percent from 2021. The US winter wheat area came in 1.4 million acres above trade expectations at 34.236 million acres. Spring wheat was 11.200 million acres, 600,000 below trade expectations and durum at 1.915 million, 188,000 acres below expectations. Cotton was reported at 12.234 million, above 11.220 million last year.

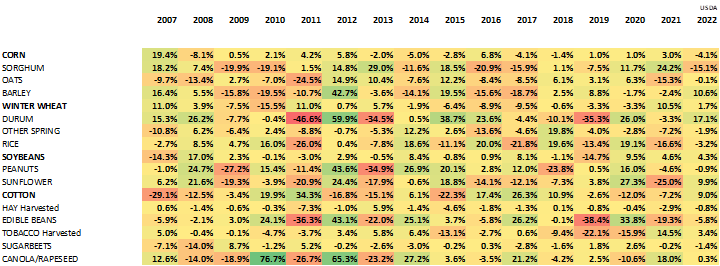

Percentage change heat map, y/y

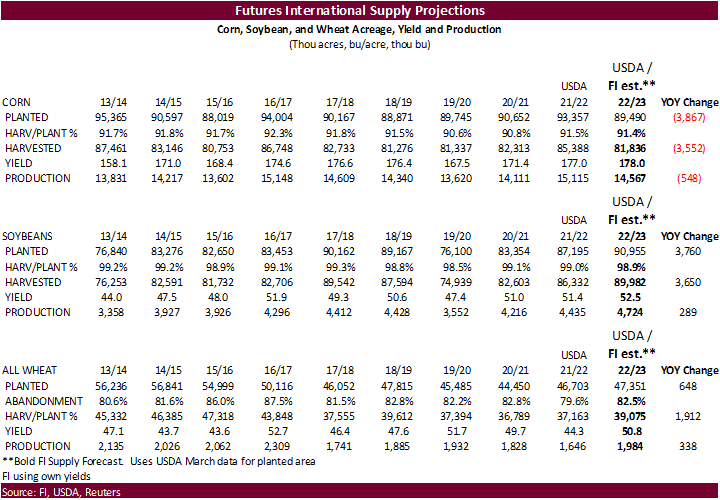

Based on the latest data, following table is our prediction for US supply.

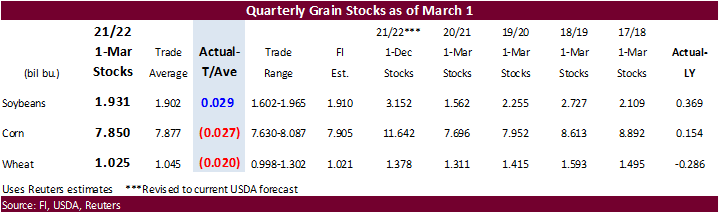

Grain stocks were 29 million bushels above expectations for soybeans, 27 million less for corn, and 20 million less for all-wheat. USDA made slight changes to December 1 soybean and corn stocks. December 1 wheat stocks were lowered 12 million bushels. We look for the “extra” soybean supply to get absorbed by exports by the end of the crop year.

For corn, implied feed demand was about 50 million bushels above expectations. For wheat, stocks are expected to remain ample and US carryout stocks could increase 15 million bushels in the April S&D update. Implied wheat for feed use was about 15 million bushels below our expectations. Note wheat stocks are lowest since 2008.

Look for the trade to continue trading Black Sea headlines but eventually we can’t ignore US weather. The Great Plains are in need of precipitation.

FI price ranges Updated 3/31/22

May corn is seen in a $6.75 and $8.10 range

December corn is seen in a wide $5.50-$8.00 range

Soybeans – November is seen in a wide $12.75-$15.50 range

Soybean meal – May $430-$500

Soybean oil – May 68.50-74.00

Chicago May $9.00 to $12.00 range, December $8.50-$11.00

KC May $9.00 to $12.00 range, December $8.75-$11.50

MN May $9.75‐$12.00, December $9.00-$11.75

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.