PDF attached

US Acreage

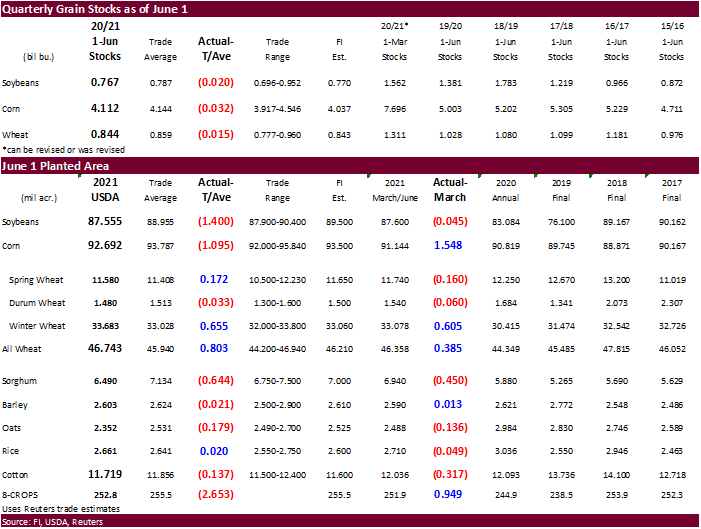

Much lower-than-expected US planted acres for soybeans and corn were reported this morning. Corn acres came in 1.095 million acres below expectations at 92.692 million, 1.55 million above March. Some estimates thought the US corn area would expand as much as 5.5 million acres. US soybean plantings were actually lowered from March by 45,000 acres to 87.555 million acres and were 1.4 million acres below expectations. The all-wheat area was taken up 385,000 acres to 46.743 million and were 803,000 acres below expectations. USDA found an additional 605,000 winter wheat acres from March. Spring and durum were revised lower from March. The area for the three minor feedgrains were also reported less than expected. What was the most surprising that comes to mind for this report was the net change for the total acres for the 8 major crops. The 8-crop area expanded only 949,000 acres from March to 252.8 million acres. The trade was looking for 255.5 million. For comparison there were 244.9 million in 2020, 238.5 million in 2019, 253.9 million in 2018 and 252.3 million in 2017.

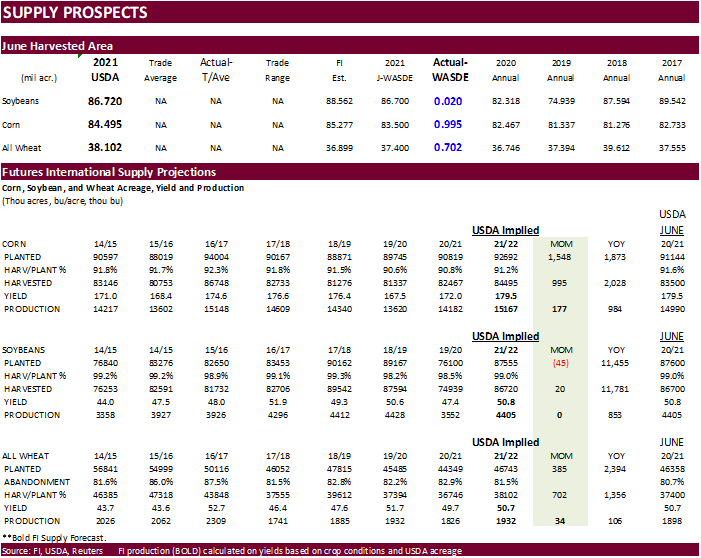

US soybean production in July may not be changed much by USDA if they use their current yield. Corn production could be revised up 177 million, and all-wheat up 34 million, using USDA’s current harvested area, and June yields. Note corn production may end up only about 140 million bushels below our previous working estimate. But the fact remains implied US soybean and corn production will end up below trade expectations, and this is why some contracts traded limit higher post USDA report. An unfavorable weather going forward may result in August corn and soybean yields coming in USDA’s current 179.5 and 50.8 projection. We are using 177.8 for corn and 51.2 for soybeans, based on the latest crop ratings. That puts corn around 15 billion and soybeans around 4.44 billion. For immediate balance adjustments, we will adjust corn demand and stocks (lower) and may leave soybean demand unchanged. For all-wheat, USDA is due to update winter wheat production (higher) in July. They will also report initial spring and durum production (much lower than implied June estimate) next month. Look for USDA to revise lower their 2021-22 US all-wheat stocks estimate.

US June 1 grain stocks were reported below expectations, but not by a large amount for all three major commodities. Unlike other grain stocks reports, we did not see the large discrepancies. There were also very small revisions to March 1 stocks.

Price limits

https://www.cmegroup.com/trading/price-limits.html

USDA NASS Executive Summary

https://www.nass.usda.gov/Newsroom/Executive_Briefings/2021/06-30-2021.pdf

September corn $4.50 and $6.00

December corn is seen in a $4.25-$6.00 range.

August soybeans are seen in a $12.75-$15.00 range (up 60/50); November $11.75-$15.00 (up25/up50)

August soybean meal – $330-$410 (up10/20); December $320-$425 (unch/up25)

August soybean oil – 60-66; December 46-67 cent range (up 100 on back end)

September Chicago wheat is seen in a $5.90-$7.00 range

September KC wheat is seen in a $5.60-$6.70

September MN wheat is seen in a $7.50-$9.00 (up50/up50)

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.