From: Terry Reilly

Sent: Thursday, April 02, 2020 2:44:44 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 04/02/20

PDF attached includes US corn, soybean and all-wheat balances

Russia

and Saudi Arabia may slow oil production. China said they plan to buy oil for reserves and a rally in crude oil might be helping stocks out. US jobless claims were about double estimates at 6.648 million.

MARKET

WEATHER MENTALITY FOR CORN AND SOYBEANS:

Weather

in South America, South Africa and India remains favorable for most oilseed development. India’s rapeseed will benefit from drier weather to help reduce a quality decline because of moisture during crop maturation and harvest season.

Improving

rainfall in Southeast Asia will be good for palm oil production and corn planting.

China’s

recent flooding rain in the south and that which is expected this weekend into next week will delay early season coarse grain planting and will keep rapeseed development a little sluggish as well. Dryness is also a concern in Yunnan.

U.S.

early season grain and oilseed areas are facing similar conditions with frequent precipitation and soggy field conditions to limit field progress for a while. Today’s somewhat drier biased outlook does offer a few pockets of drying, but the bottom line will

require much more precipitation.

Australia needs greater rain in the south prior to late April and May planting of canola. Rain in New South Wales and neighboring Wednesday and that which occurs through Friday will help to moisten some areas, but follow up rain will be needed.

Europe’s

drier weather bias in place today will improve field conditions for planting, but warming temperatures are needed before much early corn will be seeded. Winter rapeseed will be breaking dormancy, but no aggressive crop development is expected for a while.

Warming next week will help improve the situation. Timely rain will be needed once seasonal warming becomes a little more significant.

Overall,

weather today will provide a mixed influence on market weather mentality with a bearish bias.

MARKET

WEATHER MENTALITY FOR WHEAT:

India’s

drier weather this week will help protect winter crop quality after weekend weather trended a little too wet in the north. China winter crops are in mostly good condition with more aggressive development expected as soon as additional warming kicks in.

U.S.,

Russia and Europe winter crop conditions vary from fair to very good. Recent frost and freezes in southern production areas did not permanently harm crops. Warming is needed in all production areas.

There

is some need for timely precipitation in the drier areas of western Kansas, eastern Colorado, central Washington, Kazakhstan, eastern portions of Russia’s Southern Region, the lower Volga River Basin and southeastern Europe. Recent wet weather in Spain was

ideal for its winter grains.

North

Africa and the Middle East will need dry weather soon to promote grain maturation and harvesting. Too much moisture could result in a grain quality decline. Morocco has been too dry this year and will come up quite short on production.

Wheat planting prospects for Australia and South Africa are good this year because of recent rain and that which is expected over the next few weeks.

Overall,

weather today will likely provide a mixed influence on market mentality.

Source:

World Weather Inc. and FI

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, 8:30am - UN’s

FAO World Food Price Index, 4am - Port

of Rouen data on French grain exports

FRIDAY,

April 3:

- ICE

Futures Europe weekly commitments of traders report on coffee, cocoa, sugar positions

- CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions

Source:

Bloomberg and FI

·

President Trump announced Russia is considering cutting oil production. Trump: Oil Output Cut Could Be As Much As 15m Bbls

·

US Crude Oil Futures Settle At $25.32/Bbl, Up $5.01 Or 24.67%

·

US Initial Jobless Claims Mar-28: 6648K (exp 3800K; prev 3283K)

–

Continuing Claims Mar-21: 3029K (exp 4941K; R prev 1784K)

·

US Trade Balance (USD) Feb: -39.9B (exp -40.0B; R prev -45.5B)

·

US Factory Orders (M/M) Feb: 0.0% (est 0.2%; prev -0.5%)

–

Factory Orders Ex-Transportation (M/M) Feb: -0.9% (prev R -0.4%)

–

Durable Goods Orders (M/M) Feb F: 1.2% (est 1.2%; prev 1.2%)

–

Durables Ex-Transportation (M/M) Feb F: -0.6% (est -0.6%; prev -0.6%)

–

Cap Goods Orders Nondef Ex-Air (M/M) Feb F: -0.9% (est -0.8%; prev -0.8%)

–

Cap Goods Ship Nondef Ex-Air (M/M) Feb F: -0.8% (est -0.8%; prev -0.7%)

Corn.

·

Corn futures started higher strength in WTI crude oil and US planting delay concerns, but bear spreading led to mixed settlement. While we were in the process of downward revising our weekly ethanol production

estimates for the US (updated corn balance attached), WTI crude oil jumped about $4.00 barrel higher after President Trump said he brokered a deal with Saudi Arabia and Russia on lowering crude oil production. This helped support corn prices. Algeria bought

corn but origin was thought to be Black Sea or US rather than Argentina.

·

US crude settled at $25.32/bbl, up $5.01 or 24.67%.

·

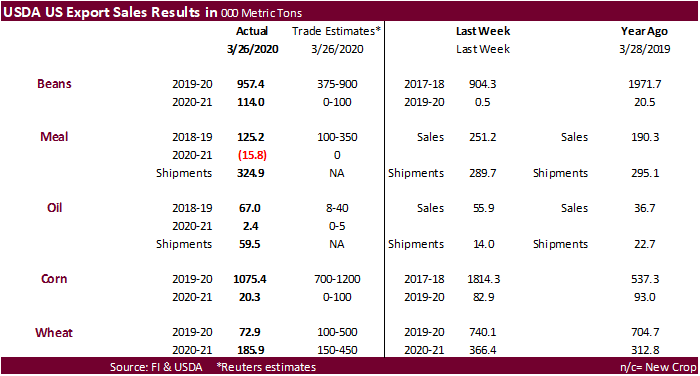

USDA export sales for corn of 1.075 million tons were at the high end of expectation. See text after the wheat comment.

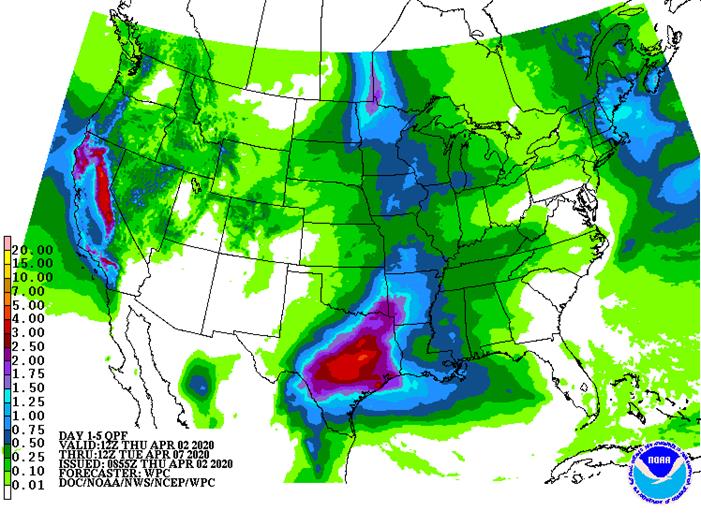

- Precipitation

for the Delta and lower Midwest early this month might be frequent enough to delay planting progress. - China’s

commerce ministry said main grain supplies are sufficient for domestic demand and will not be in shortage even without any imports. China’s ending stocks of wheat, corn and rice in 2019 totaled more than 280 million tons. Consumption on average is more than

200 million tons. - Ukraine’s

grain exports were record 46 million tons in the first nine months of the 2019-20 versus 37.6 million year earlier, according to the Ministry for Development of Economy, Trade and Agriculture. - Ukraine’s

grain and oilseed exports in 2019-20 July-June season were estimated by UGA at 57.2 million tons, above 55.6 million tons a month ago. Ukraine’s major traders union UGA said this week it agreed with an economy ministry proposal to limit wheat exports to 20.2

million tons in the 2019-20 season to avoid a rise in domestic bread prices. -Reuters

·

For new crop, several analysts are above 2.4 billion bushels, including myself, for ending stocks.

Export

Developments

- Algeria

bought 40,000 tons of corn for late April and early May shipment at about $192 to $193 a ton c&f. Origin was thought to be from the US.

- Egypt

might be looking around for a couple cargos of Ukraine corn. - Today

China was planned to auction off 20,000 tons of frozen pork from state reserves.

-

CBOT

May is seen in a $3.10 and $3.70 range. July could reach below $3.00 if we see a major reduction in US ethanol production. December is seen in a $2.85-$3.95 range.