From: Terry Reilly

Sent: Wednesday, July 18, 2018 7:53:09 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 07/18/18

PDF attached

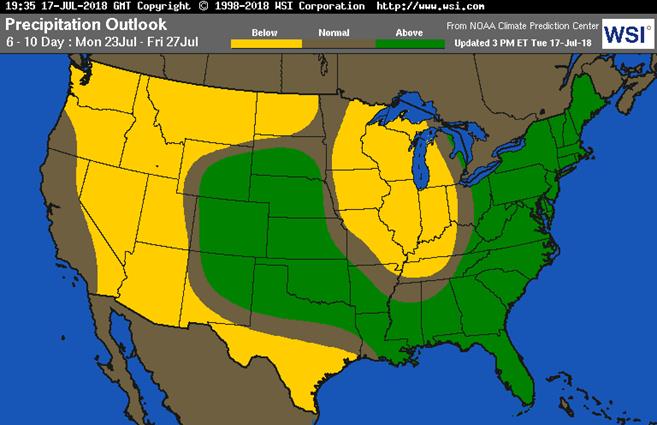

· There were no major changes to the 2-week US weather outlook for the Midwest.

· However, the evening GFS model (7/18) reduced rainfall for the Delta and southeastern Great Plains for week 1 and showed a mix of decreases/increases for several locations for week 2.

· Several waves of rain are forecast across the northern and central Plains, Midwest, Delta and southeastern states through July 31.

· Rainfall of 0.20 to 0.75 inch will impact the southwestern Corn Belt while 0.50 to 1.50 inches occurs in many other areas.

· The U.S. Pacific northwest and northwestern U.S. Plains will be dry or mostly dry during the next ten days

· Net drying will continue across the southwestern Corn Belt and the southern Plains.

· The Delta and southeastern states will see a mix of rain and sunshine.

· The northwestern Plains will see an increase of net drying.

· We are hearing lack of corn tasseling across WI. Feedback is welcome.

· The Canada Prairies will see net drying across the southern crop areas. Western and northern Alberta will be wettest.

· East-central China will continue to see net drying this week but the Northeast Provinces will improve with rain.

· Frequent rain will fall from eastern Europe through the western CIS this week.

· Western Europe will trend wetter this week.

Source: World Weather Inc. and FI

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Fri 85% cvg of up to 0.75”

and local amts to 1.50”

with some bands of

1.50-3.30”; S.D. to Wi.

wettest with a few bands

of heavy rain elsewhere;

far SE and far NW driest

Thu-Sat 90% cvg of up to 0.75”

and local amts to 1.50”

with a few bands of

1.50-2.75”

Sat 15% cvg of up to 0.20”

and locally more;

Wisc. wettest

Sun-Mon 40% cvg of up to 0.50” 25-40% daily cvg of

and local amts to 1.10”; up to 0.35” and locally

wettest NW more each day;

wettest east

Tue 30% cvg of up to 0.30”

and locally more;

wettest SE

Tue-Jul 27 5-20% daily cvg of up

to 0.30” and locally

more each day

Jul 25-28 5-20% daily cvg of up

to 0.30” and locally

more each day

Jul 28-30 55% cvg of up to 0.60”

and locally more

Jul 29-31 60% cvg of up to 0.60”

and locally more

Jul 31-Aug 1 5-20% daily cvg of up

to 0.25” and locally

more each day

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy-Thu 30-50% daily cvg of

up to 0.75”and local

amts over 1.50” each

day; N.C. and Va.

driest

Thu-Fri 5-20% daily cvg of up

to 0.25” and locally

more each day; wettest

Thursday; wettest north

Fri-Sun 85% cvg of up to 0.75”

and local amts to 1.50”

with some 1.50-3.0”

bands; driest west

Sat-Tue Up to 15% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Mon-Tue 15-35% daily cvg of

up to 0.70” and locally

more each day; Va.

and Carolinas wettest

Jul 25 40% cvg of up to 0.40”

and local amts to 1.0”

Jul 25-27 75% cvg of up to 0.75”

and local amts to 2.0”;

driest west

Jul 26-28 Up to 15% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Jul 28-29 15-35% daily cvg of

up to 0.60” and locally

more each day

Jul 29-31 50% cvg of up to 0.65”

and locally more

Jul 30-Aug 1 60% cvg of up to 0.75”

and locally more

Source: World Weather Inc. and FI

THURSDAY, JULY 19:

- Nicaragua on holiday

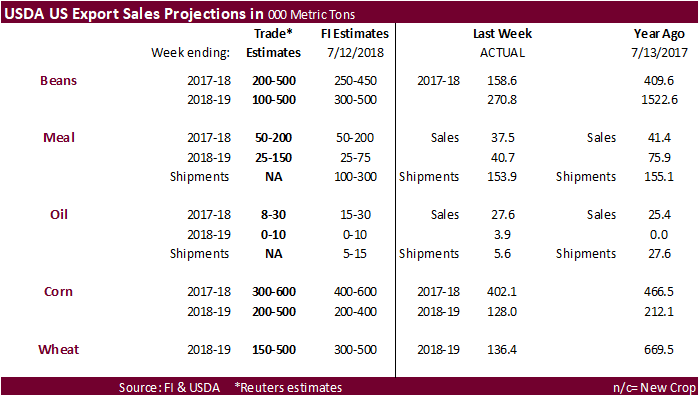

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- USDA red meat production for June, 3pm

- National Confectioners Association North America 2Q cocoa grind, ~4pm

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, JULY 20:

- Colombia on holiday

- Cocoa Association of Asia is set to release 2Q cocoa grind data

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- USDA milk production for June, 3pm

- USDA cattle on feed for June, 3pm

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- FranceAgriMer weekly updates on French crop conditions

Source: Bloomberg and FI

· US Housing Starts Change Jun: 1173K (est 1320K; prev R 1337K)

– Housing Starts (M/M) Jun: -12.3% (est -2.2%; prev R 4.8%)

– Building Permits Change Jun: 1273K (est 1330K; prev 1301K)

– Building Permits (M/M) Jun: -2.2% (est 2.2%; prev -4.6%)

Corn.

- Corn prices ended 0.50-1.25 cents higher on short covering. This is the third consecutive increase. Some areas of the US southwestern Corn Belt and Delta are starting to see expanding pockets of dryness.

- Funds bought an estimated net 4,000 corn contracts.

- The French corn crop could start harvest season a couple week earlier this year (mid-Aug) due to adverse weather.

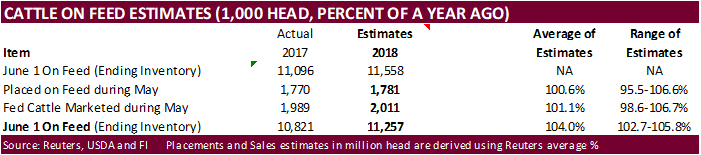

· The USDA Cattle on Feed report will be released on Friday. Estimates are below the export development section.

· USDA’s weekly Broiler Report showed eggs set in the US up 1 percent and chicks placed up 2 percent from a year ago. Cumulative placements from the week ending January 6, 2018 through July 14, 2018 for the United States were 5.14 billion. Cumulative placements were up 2 percent from the same period a year earlier.

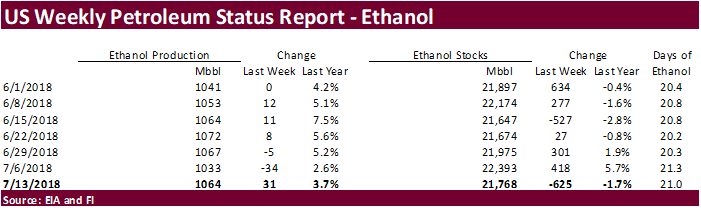

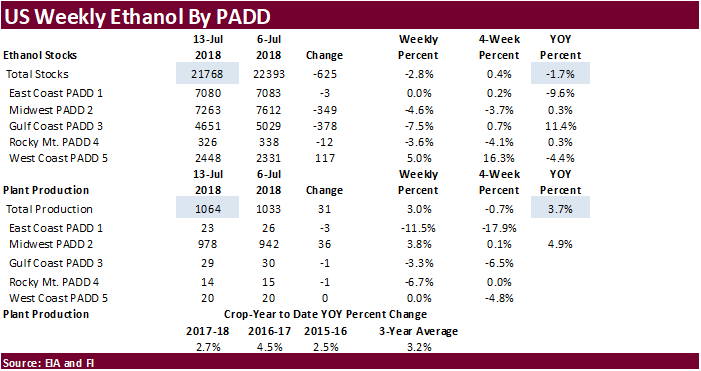

· September 2017 through mid-July ethanol production is running 2.7 percent above the same period a year ago.

· US ethanol stocks decreased 625,000 barrels to 21.768 million barrels from the previous week. A Bloomberg survey was looking for a 74k decline.

· South Korea’s KOCOPIA Group bought 60,000 tons if US corn at $211.47/ton c&f for arrival around November 20.

· China sold about 52-53 million tons of corn out of reserves this season.

Soybean complex.

- Soybeans opened higher, traded lower, and turning higher all by mid-morning. Prices settled higher. The higher trade was in part to follow through buying amid recovery after prices nearly hit a decade low. US demand remain good despite the absence of China. Under the 24-hour announcement system, US exporters reported the sales of 199,500 tons of soybeans for delivery to Pakistan during the 2018/2019 marketing year. Pakistan has not shown up in the 24-hour announcement system for a long time, but they are active in buying soybeans on a regular basis, as indicted in the weekly USDA export sales report.

- The import arb between Brazil and US soybeans into China is nearing parity, and that is gaining the attention of bull traders that hope to see China step back in and buy US. Brazil premiums slipped midweek, while US was about unchanged.

- Brazil’s shipping lineup is still heavy with 5.8 million tons in the lineup.

· Soybean meal ended lower while unwinding of meal/oil spreading pressure soybean oil.

· Funds bought an estimated net 3,000 soybean contracts, sold 3,000 meal and bought 3,000 soybean oil.

· News was very light and commercial interest in futures trading was slow on Wednesday.

· North Dakota soybeans, corn and soybeans are developing well ahead of normal pace. In SD, 1/5 of the winter crop was harvested.

- Under the 24-hour announcement system, US exporters reported the sales of 199,500 tons of soybeans for delivery to Pakistan during the 2018/2019 marketing year. Weekly exports to Pakistan below.

- China sold 140,068 of 2013 soybeans at an average price of 2993 yuan per ton, or $446.57/ton, 28 percent of the total.

· China sold 972,370 tons of soybeans out of reserves so far, this season.

· China failed to sell 56,611 tons of soybean oil out of state reserves.

- The CCC seeks 12,500 tons of soybean meal for Honduras, opened until July 18, for early October shipment.

- Results awaited: Iran seeks 30,000 tons of sunflower oil on July 10.

- Results awaited: Iran seeks 30,000 tons of palm olein oils on July 10.

- Iran seeks 30,000 tons of soybean oil on August 1.

- South Korea seeks 1,500 tons of non-GMO soybeans on July 25 for September-December delivery.

· All three US wheat markets traded two-sided, ending mixed in Chicago, mostly lower in KC and lower in MN. Chicago wheat futures hit the $5.05/bu mark for the first time since July 10, before pairing gains. The contract ended below $4.95. KC wheat settled just below $4.90 and MN below $5.30/bu.

· Funds today sold an estimated net 3,000 SRW wheat contracts.

· Egypt approved to import 120,000 tons of wheat from AOS and Union, two main supplies, bypassing the GASC. This might be in effort to make up for cargoes that were previous rejected/cancelled, but later we learned the cargos already arrived.

· German farming association DBV lowered its estimate of the German winter barley crop by 700,000 tons to 7.3 million tons from early July, down from 9.0 million tons harvested in 2017. Yields were forecast at 6 tons/hectare versus 7.4 tons in 2017. The association could not determine winter rapeseed or winter wheat production as information lacked, but noted the harvest started 2-3 weeks early because of dry conditions, and crop sizes will be significantly lower.

· Australia will see another round of net drying in eastern Australia, threatening crop establishment. Longer-term, traders are worried El Nino will yield negatively impact crops in the eastern regions. Rain is badly needed.

Net drying across the PNW is stressing spring wheat.

Source: World Weather and FI

· Egypt approved to import 120,000 tons of wheat from AOS and Union, two main supplies, bypassing the GASC. This might be in effort to make up for cargoes that were previous rejected/cancelled, but later we learned the cargos already arrived.

- Bahrain Flour Mills seeks 17,000 tons of semi-hard wheat and 8,000 tons of hard wheat, on July 24, valid until July 25, for shipment in late Aug/early Sept. Origins include Australia, Baltics, & Canada.

- Japan in a SBS import tender passed on 120,000 tons of feed wheat and 200,000 tons of barley for arrival by December 28.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on July 25 for arrival by December 28.

- China sold 6858 tons of 2013 imported wheat from state reserves at auction at an average price of 2235 yuan/per ton or $332.90/ton, 0.4 percent of what was offered.

- Japan seeks 57,914 tons of US food wheat on Thursday for September loading.

· Jordan seeks 120,000 tons of wheat on July 19 for Oct-Nov shipment.

- Bangladesh seeks 50,000 tons of optional origin milling wheat on July 25 for shipment within 40 days of contract signing.

Rice/Other

- Egypt plans to import 500,000-700,000 tons of rice paddy over the next year.

- Results awaited: Thailand seeks to sell 120,000 tons of raw sugar on July 18.

· Results awaited: Mauritius seeks 6,000 tons of white rice for Sep 1-Nov 30 shipment.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.