From: Terry Reilly

Sent: Thursday, August 23, 2018 6:28:27 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 08/23/18

PDF attached

Weather and crop conditions

· A ridge of high pressure may evolve across the southeastern states, Delta, Corn Belt, and eastern Hard Red Winter Wheat Region Aug. 30 – Sep. 6 (two days later than what was predicted Monday).

· The second week of the weather outlook calls for cool temperatures across the US Corn Belt but that could change depending on ridge development.

· Before then, look for rain across the US northwestern Midwest areas Friday and Saturday.

· The Delta will see drier weather through Saturday.

· US spring wheat will see minor harvesting delays for the balance of the week.

· HRW wheat country will see showers on and off through early next week.

· Eastern Australia’s rainfall starts Thursday evening lasting through Saturday.

· Western Australia could see rain mid-next week.

· Eastern China will see net drying through at least August 29.

· Canada’s Prairies will remain on the dry side this week.

· Indonesia and Malaysia rainfall are slowing and some attribute the below normal rainfall to El Nino.

Corn.

- Corn futures hit a fresh 5-week low on Thursday on good US crop prospects. Futures were down for the fifth consecutive session and trading volume was above average.

- The funds sold an estimated net 18,000 corn contracts.

· Day four of the US crop tour showed yields in Minnesota could end up below average from too much rain and flooding early in the growing season.

· Argentina’s AgMin sees corn planting area up 2.7% to 9.35 million hectares

- USDA export sales for corn of 173,400 tons old crop and 1.055 million tons new-crop were good.

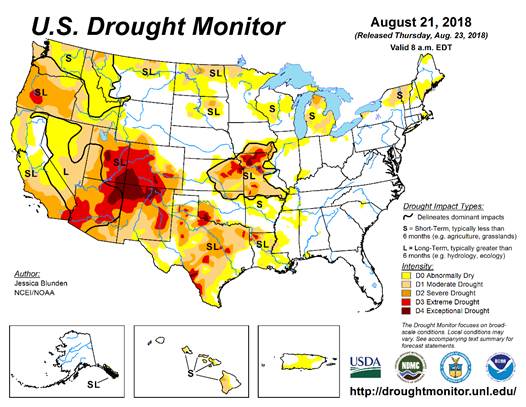

- USDA reported 13 percent of the US corn area is experiencing some type of drought as of 8/14, up from 11 percent last week and compares to 15 percent at this time a year ago. Missouri, Texas and Kansas are seeing the bulk of drought conditions.

- IGC raised their outlook for the 2018 world corn production to 1.064 billion tons, 12 million higher from previous.

- China’s central government is getting behind ethanol use by promoting the product in 15 districts this year. Details were lacking but it may mean additional funding to build or expand ethanol plants. China corn futures rallied on the news, but also traded higher after trade data showed a large decline in China corn imports.

- China January corn on Thursday was up 13 yuan or 0.7%.

- China imported 330,000 tons of corn in July, down 63.7 percent from last year.

- China imported 220,000 tons of sorghum in July, down 62.5 percent from 588,364 tons a year ago and off down 450,000 tons in June.

- China’s pork imports in July were at 88,163 tones.

- China reported a 4th case of African swine fever, affecting more than 1300 pigs in Wenzhou, Zhejiang province. This is the fourth known case and is also the fourth province, meaning its spreading. Total cull count is about 21k.

- Note China pig inventories have been on a steady decline since April 2017.

- Brazil chicken production was expected to fall 1-2 percent to 13MMT this year because of lower slaughter inventories, according to ABPA. Earlier this year they predicted a 2-4 percent increase. The truckers strike forced birds to be slaughtered or put down due to lack of feed supplies.

US crop tour

· Day four of the US crop tour showed yields in Minnesota could end up below average from too much rain and flooding early in the growing season.

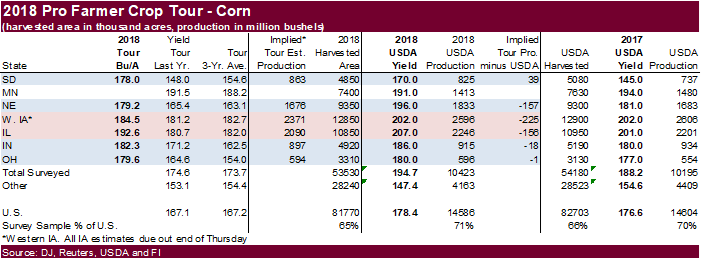

- Day three of the crop tour was viewed slightly friendly for corn futures. Western IA corn yields from 3 districts came in above last year and a three-year average but the 2018 average for the three districts of 184.5 bu/ac falls below USDA’s all-IA corn yield of 202.0 bu/ac. Corn yields varied across the western area of IA as weather had a negative impact on some areas. IL corn yield was estimated at 192.6 bu/ac, above last year and tour average, but it falls below USDA’s 207 bu/ac and 201.0 bu/ac in 2017.

- Day two of the US ProFarmer Crop Tour showed corn yields up from a year ago and above average. NE was pegged at 179.2 bu/ac, up from 165.4 in 2017 and average of 163.1 bu/ac. IN was projected sharply higher than a year ago at 179.6 bushels per acre, above 164.6 for 2017 and average of 154.0 bu/ac.

- Day one of the US ProFarmer Crop Tour showed South Dakota corn yields up from a year ago and above average. SD was pegged at 178.0 bu/ac, up from 148.0 in 2017 and average of 154.6 bu/ac. Ohio were projected sharply higher than a year ago at 179.6 bushels per acre, above 164.6 for 2017 and average of 154.0 bu/ac.

Soybean complex.

· The soybean complex traded lower again on large US crop prospects, early light harvest pressure and sharply weaker barge and Gulf basis. African swine fever spread to a fourth province in China. At least 21k hogs have been culled.

· After the close, The White House released a statement saying the trade talks between the US and China had ended. The White House also said that the two nations “exchanged views on how to achieve fairness, balance, and reciprocity in the economic relationship.” The soy complex did sell off into the close and the lack of and solid agreement between China and the U.S. may have weighed on the market.

· The funds sold net 7,000 soybeans, sold 4,000 soybean meal, and net even on soybean oil.

· Argentina’s AgMin sees the 2017/18 soybean harvest at 37.78 million tons, up 0.30% from last months 37.48 million tons and down 31.3% from last year’s 55 million tons.

· Day four of the US crop tour showed yields in Minnesota could end up below average from too much rain and flooding early in the growing season which forced replants in some areas.

· USDA export sales for soybeans were 152,700 tons old crop and 1.149 million tons new-crop, good in our opinion. Soybean meal exports sales slipped from the previous week while soybean oil improved slightly. However soybean oil export sales remain low.

- USDA reported 18 percent of the US soybean area is experiencing some type of drought as of 8/14, up from 16 percent last week and compares to 16 percent at this time a year ago. Missouri, Texas, Michigan and Arkansas are seeing the bulk of drought conditions.

· The Brazilian real hit its lowest level against the USD since February 2016.

· Malaysia is back from holiday and November palm futures fell to a 1-week low.

US crop tour

· Day four of the US crop tour showed yields in Minnesota could end up below average from too much rain and flooding early in the growing season which forced replants in some areas.

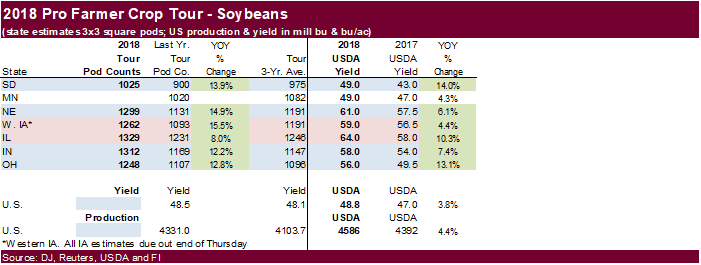

· Day three of the crop tour shows western IA pod counts are very good as they average 15.5% higher than last year. USDA looks for all Iowa soybean yield to increase 4.4%. Eastern IA will be survey today/Thursday. IL pod counts are up 8% from last year while USDA predicts a 10.3% rise in the soybean yield for the state.

- Day two of the US ProFarmer Crop Tour showed IN soybean pods in a 3-by-3 foot area averaged 1,312, above 1169 pods a year ago and the three-year average of 1147 pods. Pods in NE averaged 1,299 pods, up from 1131 pods in 2017 and the three-year average of 1191. See our table below

- Day one of the US ProFarmer Crop Tour showed South Dakota soybean pods in a 3-by-3 foot area averaged 1,024.7, above 900.0 pods a year ago and the three-year average of 975.1 pods. Pods in Ohio averaged 1,248.2 pods, up from 1,107.0 pods in 2017 and the three-year average of 1,095.8.

- Final results will be out Friday, August 24. Follow the Pro Farmer Midwest Crop Tour here on Twitter #pftour18

· Wheat futures finished lower in a see-saw trade. Technical selling was seen all session, outside of an early session bid following the floor open that briefly turned SRW positive.

· Funds sold an estimated 4,000 contracts of Chicago wheat.

· EU December wheat was 1.00 euro lower at 205.75 euros.

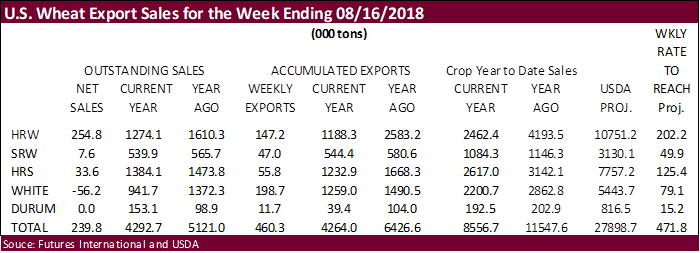

· USDA export sales for all wheat were poor at 239,800 tons. There were 56,200 tons of net reduction for white wheat. 254,800 tons of sales were added to HRW. SRW sales were only 7,600 tons.

- USDA reported 32 percent of the US hay area is experiencing some type of drought as of 8/14, up from 31 percent last week and compares to 15 percent at this time a year ago. Missouri, Utah, Oregon, and Colorado are worse off.

- It’s time to start thinking about 2019 US winter wheat seedings. We look for a small increase in area from wheat was planted for 2018 harvest. Note 31 percent of the US wheat area is experiencing some type of drought, down from 33 percent last week but double where it was a year ago. Missouri, Texas and Oklahoma are hardest hit areas.

· The IGC reduced its forecast for 2018 world wheat production by 5 million tons to 716 million tons from previous.

· The EU granted wheat imports under quota of 26,000 tons.

· SovEcon projected a 6-year low in end of 2018-19 (June 2019) Russia grain stocks to 10.1MMT after they lowered grain production to 109.6MMT from 113.9MMT previously.

· Russia may see a short to medium-term boost in wheat exports after the currency hit its lowest level since April 2016 and wheat prices from other major exporters appreciated in recent months. SovEcon warned of strengthening domestic Russia wheat prices in the months ahead.

· Kazakhstan’s AgMin put grain output at over 20 million tons – gross weight. 2017 Kazakhstan grain production was 21.9 million tons in bunker weight. Bunker weights – grain that has not been cleaned.

- China imported 600,000 tons of barley in July, down 16.2 percent from a year earlier.

- China’s wheat imports in July were down 43 percent from a year ago to 140,000 tons.

- Argentina has seen drought conditions creep back with 15 percent of the wheat area affected. One group said that could expand to 30 percent by early September.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.