From: Terry Reilly

Sent: Saturday, August 25, 2018 1:08:05 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 08/25/18

PDF attached

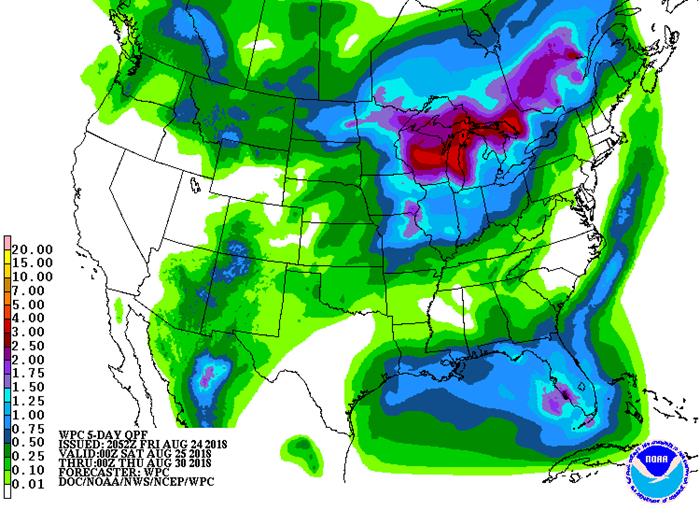

· Rain over the short-term could slow harvesting in the Delta and lower Midwest, while rain in the northern areas could benefit late maturation.

· A ridge of high pressure may evolve across the southeastern states, Delta, Corn Belt, and eastern Hard Red Winter Wheat Region Aug. 30 – Sep. 6 (two days later than what was predicted Monday).

· The second week of the weather outlook calls for cool temperatures across the US Corn Belt but that could change depending on ridge development.

· The Delta will see rain next week.

· US spring wheat will see minor harvesting delays for the balance of the week.

· HRW wheat country will see showers on and off through early next week.

· Eastern Australia’s rainfall starts Thursday evening lasting through Saturday.

· Western Australia could see rain mid-next week.

· Eastern China will see net drying through at least August 29.

· Canada’s Prairies will remain on the dry side this week.

· Indonesia and Malaysia rainfall are slowing and some attribute the below normal rainfall to El Nino.

We look for US crop conditions to be steady when reported on Monday.

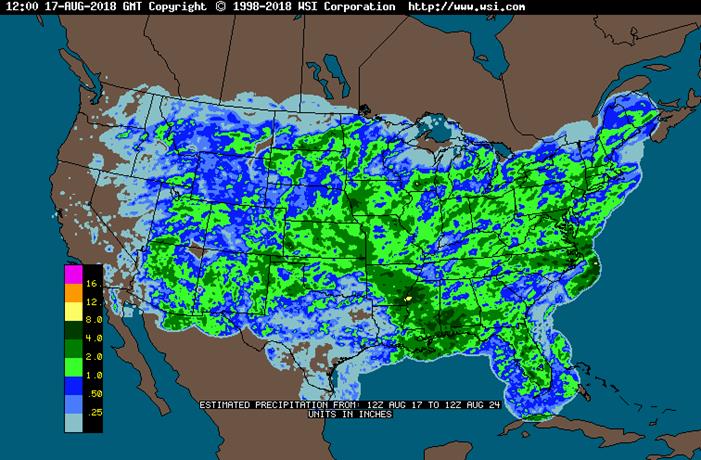

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Sat 75% cvg of up to 0.75”

and local amts to 1.75”;

driest south; wettest

west

Sat-Sun 40% cvg of up to 0.75”

and local amts over 2.0”;

wettest NE

Sun-Mon 40% cvg of up to 0.40”

and local amts to 1.0”;

driest south

Mon-Tue 60% cvg of up to 0.75”

and local amts to 1.50”;

driest NW

Tue-Wed 75% cvg of up to 0.75”

and local amts to 2.0”

Wed-Thu 40% cvg of up to 0.75”

and local amts to 1.75”;

wettest south

Thu-Sep 1 80% cvg of up to 0.75”

and local amts to 1.75”

Aug 31-Sep 1 30% cvg of up to 0.60”

and local amts to 1.40”;

wettest north

Sep 2-5 5-20% daily cvg of up 10-25% daily cvg of

to 0.25” and locally up to 0.25” and locally

more each day more each day

Sep 6-7 50% cvg of up to 0.50”

and locally more

Sep 6-8 60% cvg of up to 0.50”

and locally more

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy-Sat Mostly dry with a few

insignificant showers

Tdy-Mon 15-35% daily cvg of

up to 0.50” and locally

more each day; west

and south wettest

Sun-Thu 5-20% daily cvg of up

to 0.35” and locally

more each day

Tue-Wed 5-20% daily cvg of up

to 0.35” and locally

more each day

Thu-Sep 1 15-35% daily cvg of

up to 0.50” and locally

more each day

Aug 31-Sep 7 Up to 20% daily cvg of

up to 0.25” and locally

more each day; some

days may be dry

Sep 2-7 5-20% daily cvg of up

to 0.35” and locally

more each day

Source: World Weather and FI

Bloomberg weekly agenda

MONDAY, AUG. 27:

- U.K. summer bank holiday

- SGS data for Malaysia’s Aug. 1-25 palm oil exports, 3am ET (3pm Kuala Lumpur)

- EU’s monthly Monitoring Agricultural Resources (MARS) bulletin on crop progress and weather conditions in Europe, 7am ET (noon London)

- EU weekly grain, oilseed import and export data, 10am ET (3pm London)

- USDA weekly corn, soybean, wheat export inspections, 11am

- USDA weekly crop progress report, 4pm

- Ivory Coast weekly cocoa arrivals

TUESDAY, AUG. 28:

- Palm Oil Trade Fair & Seminar in Kuala Lumpur, Aug. 28-29. Speakers include Oil World Executive Director Thomas Mielke, LMC Intl Chairman James Fry and Godrej Director Dorab Mistry

WEDNESDAY, AUG. 29:

- EIA U.S. weekly ethanol inventories, output, 10:30am

THURSDAY, AUG. 30:

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, AUG. 31:

- Malaysia on holiday; No palm oil futures trading on Bursa Malaysia Derivatives

- Statistics Canada’s domestic crop production report for July, 8:30am ET

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

Source: Bloomberg and FI

Bloomberg weekly agenda

FRIDAY, AUG. 24:

- ProFarmer issues final yield estimates after crop tour, 2pm

- USDA cattle-on-feed report for July, 3pm

- Unica bi-weekly report on Brazil Center-South sugar output

- Salvadoran coffee council’s El Salvador July export data

- Nicaragua’s coffee council releases July export data

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

MONDAY, AUG. 27:

- U.K. summer bank holiday

- SGS data for Malaysia’s Aug. 1-25 palm oil exports, 3am ET (3pm Kuala Lumpur)

- EU’s monthly Monitoring Agricultural Resources (MARS) bulletin on crop progress and weather conditions in Europe, 7am ET (noon London)

- EU weekly grain, oilseed import and export data, 10am ET (3pm London)

- USDA weekly corn, soybean, wheat export inspections, 11am

- USDA weekly crop progress report, 4pm

- Ivory Coast weekly cocoa arrivals

TUESDAY, AUG. 28:

- Palm Oil Trade Fair & Seminar in Kuala Lumpur, Aug. 28-29. Speakers include Oil World Executive Director Thomas Mielke, LMC Intl Chairman James Fry and Godrej Director Dorab Mistry

WEDNESDAY, AUG. 29:

- EIA U.S. weekly ethanol inventories, output, 10:30am

THURSDAY, AUG. 30:

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, AUG. 31:

- Malaysia on holiday; No palm oil futures trading on Bursa Malaysia Derivatives

- Statistics Canada’s domestic crop production report for July, 8:30am ET

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

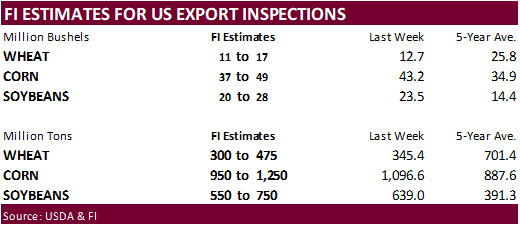

The CFTC report showed no records for the major commodities in traditional funds or managed money. There were some positions very close to record. Traditional funds bought more than expected corn, wheat and soybean meal, and sold a less than expected number of soybeans. Traditional funds sold a little more soybean oil than the trade guessed. For the week ending 8/21, money managers were busy buying soybeans and corn, although much of that occurred early on.

· US Durable Goods Orders (Jul P): -1.7%(est -1.0%, prevR 0.7%)

· US Durables Ex Transport (Jul): 0.2% (est 0.5%, prevR 0.1%)

· US Durables Ex Defence (Jul) (M/M): -1.0% (est 0.8%, prevR 1.2%)

· US Cap Goods Orders Nondef (Jul P):1.4%(est 0.5%,prevR 0.6%)

· US Cap Goods Ship Nondef (Jul P):0.9%(est 0.3%,prevR 0.9%)

Corn.

- Corn futures ended higher on short covering. Open Interest was up more than 30k on Thursday indicating a rush of shorts into the market. On Friday they took light profit, reversing a 5-day downtrend in December corn. Corn prices are hovering around July 19 levels.

- September corn settled below the lower end of $3.50 of our previous trading range. September corn may trade in a $3.35-$3.65 range.

- Funds bought an estimated net 8,000 corn on Friday.

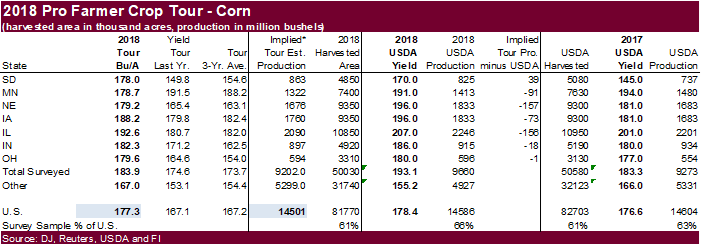

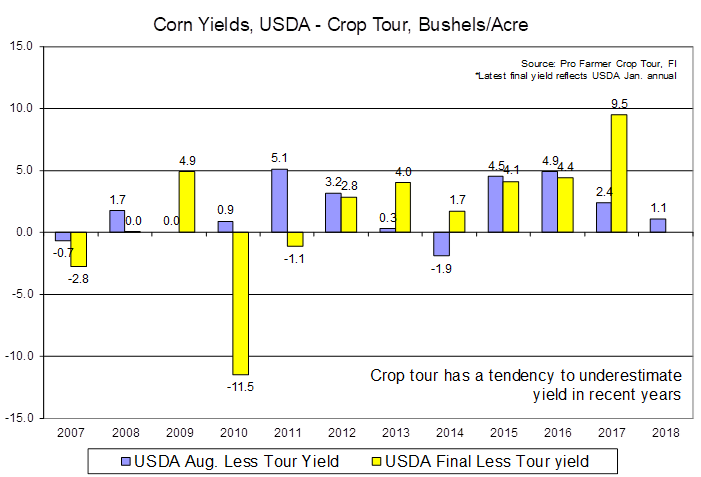

- ProFarmer estimated the US corn crop at 14.501 billion bushels, below USDA’s August estimate of 14.586 billion. With a yield of 177.3, below 178.4 bu/ac for USDA August, we agree. Corn yields are variable across a wide part of the WCB unlike soybeans which for the most part look good. The ProFarmer implied harvested area is about in line with USDA’s August estimate, and based on recent FSA data, we also agree with their findings.

- Overall, we found the annual crop tour yield as a little friendly corn and bearish soybeans.

- Mexico said it’s close on reaching a trade deal with the US that are holding back NAFTA talks.

- Canada may come back to the table soon.

- The EU and US may reach a trade deal before May 2019.

- French corn conditions as of Aug. 20 were unchanged from the previous week at 61 percent, down from 80 percent a year earlier.

- South Africa’s CEC on August 28 will update their corn production next week and a Reuters poll calls for 13.11 million tons, down 0.7 percent from the 13.207 million tons in July.

- African Swine Fever was discovered in Romania, at a large pig farm where 140,000 animals will be culled.

· South Korea’s (KFA) bought about 61,000 tons of corn from the United States at $209.95 a ton c&f for arrival around Jan. 15, 2019.

· China sold 788,487 tons of corn out of reserves at 1,439 yuan per ton ($209.34/ton), 19.8 percent of what was offered.

· Yesterday they sold 2.095MMT of corn out of reserves at 1,548 yuan per ton ($225.20/ton), 52.6 percent of what was offered.

· Another 4 million tons will be offered on Thursday and Friday of next week.

· China sold about 65.4 million tons of corn out of reserves this season.

The USDA Cattle on Feed report showed inventories at the end of August at a record 11.093 million head, 4.6 percent higher than last year and in line with expectations. Placements were higher than expected and highest for the month of July since 2012. Marketings were slightly above a trade guess and highest since 2013. US cattle inventories are high and it will take a while for the numbers to decline. This has driven tallow and grease prices lower, making the feedstock more attractive for biodiesel producer. Yellow grease in the east is about $600/ton, down $105/ton from a year ago.

8/25/18 Corn prices could see additional selling pressure leading up to the start of US harvest season.

September corn settled below the lower end of $3.50 of our previous trading range.

September corn may now trade in a $3.35-$3.65 range.

December corn is seen in a $3.05-$3.80 range.

· A rise in open interest this week was an indication new shorts entered the market. The soybean complex traded higher on Friday on profit taking but gave up gains to settle unchanged to 1.25 cents higher. Soybean meal eventually ended lower, in part to weakness in the China oilmeal markets. Soybean oil ended higher in large part to a rally in WTI crude oil. Commercial hedging increased late in the week.

· Funds bought 2,000 soybeans, sold 2,000 soybean meal and bought 3,000 soybean oil.

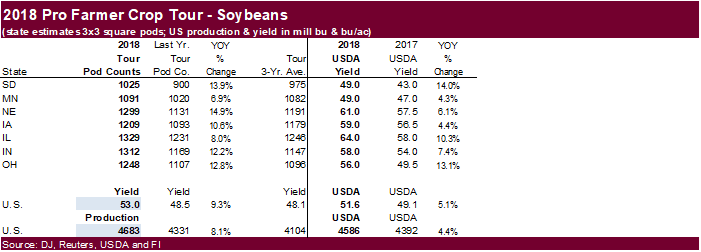

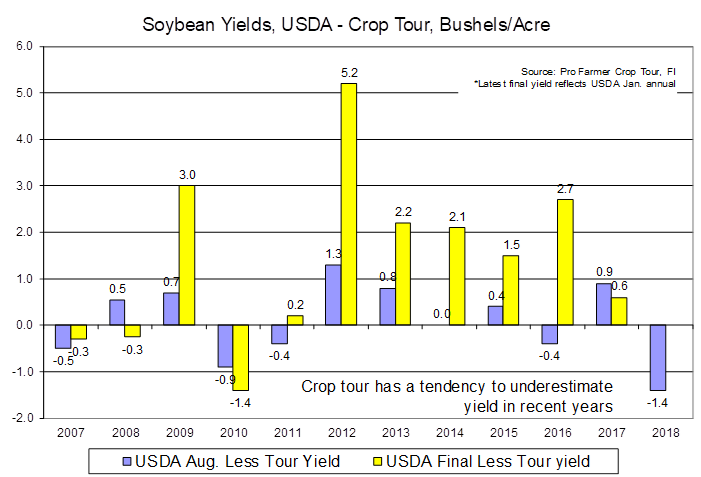

· The ProFarmer crop tour pegged the US soybean yield at a high 53.0 bushels per acre, which reflected a 4.683-billion-bushel crop. This means the implied US soybean harvested area is about 515,000 acres below USDA. Based on FSA acres, we look for USDA to trim the US soybean harvest area, but not by that much of an amount. The ProFarmer yield is higher than USDA’s 51.6 bu/ac, despite recent declines in crop conditions. At 4.683 billion, that would be a record US soybean crop.

· Overall, we found the annual crop tour yield as a little friendly corn and bearish soybeans.

- Mexico said it’s close on reaching a trade deal with the US that are holding back NAFTA talks.

· Uncertainty over the US/China trade deal was thought to contribute to weakness in US soybean bids for export.

· Traders are awaiting the Brazil court to rule on glyphosate ban.

· Brazil exported about 1.78MMT of soybeans for the week ending Aug 17, down from 2.13MMT previous week. 67MMT was thought to be committed this season.

· China soybean meal was down about 3% this week in large part to African swine fever.

· AmSpec reported August 1-25 Malaysian palm exports at 821,485 tons, down 9 percent from the same period a month ago.

· The USDA on Monday may unveil its $12 billion producer, stockpiling, and agriculture chain assistance program. Agri-Pulse via a DJ story mentioned the payment rate for soybean farmers has been preliminarily proposed at $1.65 per bushel and 1 cent per bushel for corn farmers.

· Last we heard IL crude now 25 under, East 25 over, Southeast 25 to 50 over and West nominal 50 under. Gulf basis steady around 250 over for crude degummed soybean oil. SA was mixed this week with Argentina 100 over degummed, and Brazil 140 over.

· US cattle inventories are high and it will take a while for the numbers to decline. This has driven tallow and grease prices lower, making the feedstock more attractive for biodiesel producer. Yellow grease in the east is about $600/ton, down $105/ton from a year ago.

· The CCC seeks 15,610 tons of crude degummed soybean oil on August 29 for export to Pakistan. Shipment was for Sep 27 to Oct 7.

- USDA seeks 5,000 tons of refined oil for the export program on September 5 for October shipment.

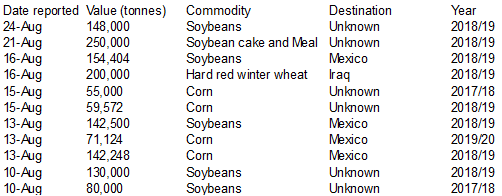

- USDA reported private exporters reported to the U.S. Department of Agriculture export sales of 146,000 tons of soybeans for delivery to unknown destinations during the 2018-19 marketing year.

- During the week ending August 31, China plans to sell 301,200 tons of 2013 soybeans, 60,100 tons of 2011-2013 rapeseed oil, and 53,800 tons of imported 2011 soybean oil.

- China sold nearly 1.3MMT of soybeans out of reserves this season.

- Iran seeks 30,000 tons of sunflower oil on September 24.

September soybeans are seen in a $8.25-$9.10 range; November $8.00-$9.50 range.

September soybean meal $295-335 range; December $280-$350 range.

September soybean oil 27.60-29.50 range; December 27.50-30.50 range.

- Changing tune. We lowered out short-term outlook on wheat given the recent developments in currency fluctuations and slow US demand. Global weather problems are starting to abate, and wheat no long looks like the sleeping giant in the agriculture space if a bull run would develop.

· On Friday US wheat futures traded to nearly a 4-month low, down 7 percent this week basis the nearby Chicago contract. Slow US demand and a favorable export environment for Russia wheat exports sent futures lower. EU futures also posted weakness this week and Australia’s improvement in weather sent funds selling US wheat. Two out of the three US September wheat contracts settled below our short-term trading ranges late this week. See our updated September ranges below. Note only one more week to deliveries.

· Adding pressure to Monday’s trade could be China’s announcement to release wheat out of reserves. China summer wheat production fell 2.4 percent to 128.35 million tons.

· Funds sold 5,000 Chicago wheat.

· EU December wheat was 3.00 euro lower at 202.75 euros.

- The German AgMin pegged the Germany’s 2018 winter wheat crop at 19.1 percent from the 2017 to 19.4 million tons. The Germany 2018 grain harvest was estimated at 34.5 million tons, down 15.8 percent on the year. Germany saw their highest summer temperatures since 1881.

- Germany will become a net importer of grains for the first time since 1986 if conditions hold.

Export Developments.

· Taiwan seeks 110,500 tons of US milling wheat from the US on August 31 fir October/November shipment.

· Tunisia bought 50,000 tons of soft milling wheat and 50,000 tons of feed barley for shipment around October. The wheat was bought in two consignments, each of 25,000 tons, one at $238.25 a toe c&f and one at $238.60 a toe c&f.

· The barley was also bought in two 25,000 ton consignments, one at $251.48 a ton c&f and the other at $252.37 a ton c&f.

· China sold 5,050 tons of 2013 imported wheat at 2,242 yuan per ton ($326.16/ton), 0.31 percent of what was offered.

· Jordan seeks 120,000 tons of feed barley on August 28.

· Jordan seeks 120,000 tons of hard milling wheat on Aug 29 for Nov/Dec shipment.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on August 29 for arrival by January 31.

Rice/Other

· South Korea seeks 92,783 tons of rice on Aug. 31 for Nov/Dec arrival.

TONNES(M/T) GRAIN TYPE ARRIVAL/PORT

10,000 Brown medium Nov 30/Gwangyang

10,000 Brown medium Dec 31/Busan

20,000 Brown medium Dec 31/Gunsan

20,000 Brown medium Dec 31/Mokpo

20,000 Brown medium Dec 31/Donghae

12,783 Brown long Nov 30/Masan

· China reported early rice production down 4.3 percent from year ago.

· Results awaited: Egypt’s ESIIC seeks 100,000 tons (150k previously) of raw sugar for shipment within the first half of September and two 50,000-ton shipments from September 15-Oct 15.

· Results awaited: Thailand plans to sell 120k tons of raw sugar on Aug. 22.

Changing tune. We lowered out short-term outlook on wheat given the recent developments in currency fluctuations and slow US demand. Global weather problems are starting to abate, and wheat no long looks like the sleeping giant in the agriculture space if a bull run would develop.

- September Chicago wheat $4.95-$5.35 range.

- September KC $5.00-$5.40 range.

- September MN $5.50-$5.80 range.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.