From: Terry Reilly

Sent: Monday, September 24, 2018 4:29:15 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 09/24/18

PDF attached

Below taken from World Weather Inc.

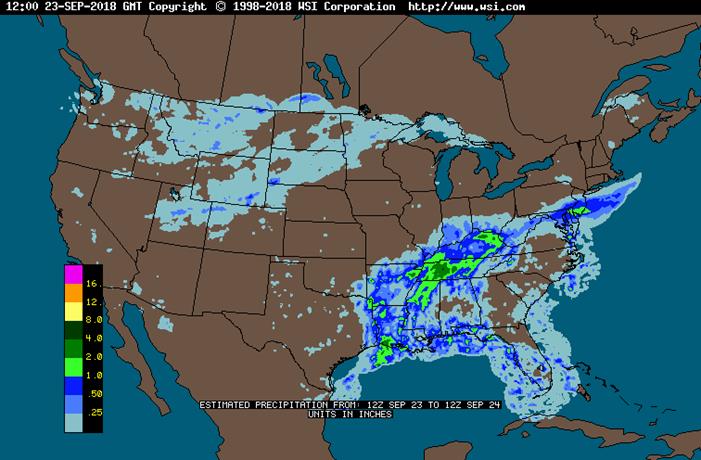

· Central and southern Oklahoma and north-central Texas saw some heavy rain over the weekend.

· Rain fell across western and northern Delta through parts of the Tennessee River Valley to Kentucky and farther northeast into New York, Pennsylvania and Virginia.

· Frequent showers will occur in the Delta this week raising concern over cotton quality and delaying the advancement of cotton, soybean, rice and sorghum harvest progress.

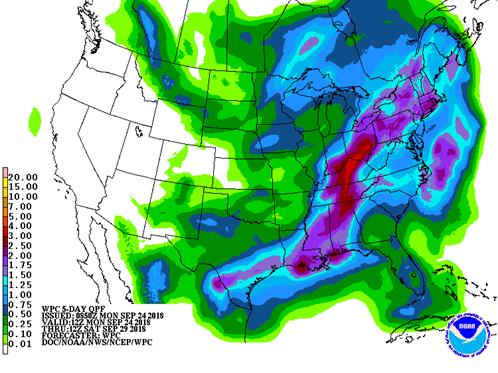

· The Midwest will see a mix of rain and sunshine this week and next week. Rainfall by next Sunday will vary from 0.10 to 0.60 inch with local totals near 1.00 inch with the exception of Kentucky and immediate neighboring areas where 1.00 to 3.00 inches and locally more may occur because of rain early to mid-week

· Hard red winter wheat areas may experience net drying this week with some areas completely dry while others in Oklahoma and Texas might receive another 0.20 to 0.75 inch – most of that occurs during mid-week.

· Northern Plains will receive 0.50 to nearly 2.00 inches of moisture from Montana to northern Minnesota with it occurring in waves

· U.S. bottom line includes an immediate need for drying in Oklahoma, Arkansas and northern Texas after weekend flooding. Additional drying is also needed in southern Minnesota, Wisconsin, Iowa and southeastern South Dakota where flooding occurred earlier last week. The southeastern states need continued limited rainfall after Hurricane Florence ravaged the area. Too much rain has been occurring in the Delta and this pattern may continue for a while resulting in some cotton and rice quality decline and harvest delays for many summer crops. Moisture in the northern and central Plains will be good for winter wheat planting, emergence and establishment. Cooling will slow maturation rates and some eventual frost and freezes are expected, but they may only help to defoliate soybeans and expedite summer crop maturation. Very little bean quality decline is expected because of cool temperatures. Frost and freezes are most likely this weekend through the first few days in October.

· South America’s greatest rainfall this week will be concentrated on northeastern Argentina, far southern Brazil and immediate neighboring areas of Paraguay and Uruguay

· Canada Prairies are advertised to be wetter biased over the next week to ten days with frequent bouts of light precipitation and cooler than usual temperatures

· Western Europe is facing another week to ten days of below average precipitation

· Eastern Europe will receive periodic precipitation this week, but mostly north of Italy and the Balkan Countries

· Russia’s middle and upper Volga Basin will experience improving soil moisture over the next ten days improving the establishment and emergence of winter wheat and rye

· Russia’s lower Volga River Basin and southeastern Ukraine may not get abundant moisture for a while, but light precipitation will still be beneficial

· Eastern Australia will receive some rain during the coming week, but no general soaking is likely and much of the moisture will be confined to far northeastern New South Wales and southeastern Queensland

· Western Australia may receive some rain Friday through the weekend, but it is not expected to be well organized

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Tue 80% cvg of up to 0.40” 100% cvg of 0.40-1.50”

and local amts to 1.0”; and local amts to 3.0”

Neb. to Wi. wettest in Ky. and south Oh.

with up to 0.60” and

local amts to 1.10”

elsewhere

Wed 15% cvg of up to 0.20”

and locally more;

wettest east

Wed-Thu 30% cvg of up to 0.20”

and locally more;

wettest north

Thu Mostly dry with a few

insignificant showers

Fri-Sat 40% cvg of up to 0.65” 35% cvg of up to 0.65”

and local amts to 1.35”; and local amts to 1.35”;

Ia. wettest north Il. wettest

Sun-Oct 1 65% cvg of up to 0.75”

and local amts to 1.50”;

wettest south

Sun-Oct 2 80% cvg of up to 0.75”

and local amts to 1.50”

Oct 2-4 80% cvg of up to 0.75”

and local amts to 2.0”

Oct 3-5 80% cvg of up to 0.75”

and local amts to 2.0”

Oct 5-8 Up to 20% daily cvg of

up to 0.20” and locally

more each day

Oct 6-8 Up to 20% daily cvg of

up to 0.20” and locally

more each day

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy 50% cvg of up to 0.75”

and local amts to 1.50”;

wettest west

Tdy-Wed 100% cvg of 0.30-1.30”

with lighter rain in a few

areas and local amts over

2.50”; wettest south

Tue-Thu 90% cvg of up to 0.75”

and local amts to 1.50”

with some 1.50-3.0”

amts in the west;

driest SE

Thu-Fri 10-25% daily cvg of

up to 0.35” and locally

more each day;

wettest south

Fri-Sat 20-35% daily cvg of

up to 0.40” and locally

more each day

Sat 60% cvg of up to 0.40”

and locally more;

wettest south

Sun-Oct 2 5-20% daily cvg of up 5-20% daily cvg of up

to 0.20” and locally to 0.20” and locally

more each day more each day

Oct 3-5 75% cvg of up to 0.65” 70% cvg of up to 0.65”

and local amts to 1.40” and local amts to 1.40”

Oct 6-8 Up to 20% daily cvg of 5-20% daily cvg of up

up to 0.25” and locally to 0.25” and locally

more each day more each day

Source: World Weather Inc. and FI

TUESDAY, SEPT. 25:

- Intertek and AmSpec release their respective data on Malaysia’s Sept. 1-25 palm oil exports, 11pm ET Monday (11am Kuala Lumpur Tuesday)

- SGS data for same period, 3am ET Tuesday (3pm Kuala Lumpur Tuesday)

- Unica’s bi-weekly Brazil Center-South sugar output, 9am ET (10am Sao Paulo)

- USDA poultry slaughter for August, 3pm

- S&P Platts Kingsman sugar conference in Miami, 1st day of 2, with speakers from ED&F Man Sugar, RaboResearch, Citi, Mexico National Chamber of the Sugar and Alcohol Industries, Sucroliq, Puma Energy

WEDNESDAY, SEPT. 26:

- EIA U.S. weekly ethanol inventories, output, 10:30am

- FOMC rate decision, 2pm; analysts expect the Fed to raise U.S. interest rates by 25 basis points

- South African crop estimates

- Globoil international vegetable oil conference in Mumbai, Sept. 26-28

- Commerce Minister Suresh Prabhu and Food Minister Ram Vilas Paswan are expected to attend, along with Oil World Executive Director Thomas Mielke, Godrej Director Dorab Mistry, Sunvin CEO Sandeep Bajoria

- S&P Platts Kingsman sugar conference in Miami, final day, with speakers from Bonsucro, ALESA, Indian Sugar Exim Corp., Central American Sugar Assoc., Avenzza

THURSDAY, SEPT. 27:

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- USDA hogs & pigs inventory for 3Q, 3pm

- USDA agriculture prices received for August, 3pm

- International Grains Council monthly report

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

- Globoil vegetable oil conference in Mumbai, 2nd day of 3

- EARNINGS: Cargill

FRIDAY, SEPT. 28:

- USDA grain stockpiles for 3Q, including corn, soy, wheat, barley, noon

- USDA wheat production report for September, noon

- Polish crop estimates

- FranceAgriMer weekly updates on French crop conditions

- Globoil vegetable oil conference in Mumbai, final day

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

The CFTC Commitment of Traders report showed some big moves over the 5—day trading period, most notably money managers selling a net 77,800 contracts of corn basis futures and options combined.

Record net short positions in soybean oil as follows:

· Traditional funds futures only -110,846

· Traditional funds futures and options combined -109,950

· Managed money funds futures only -69,818

· Managed money funds futures and options combined -77,774

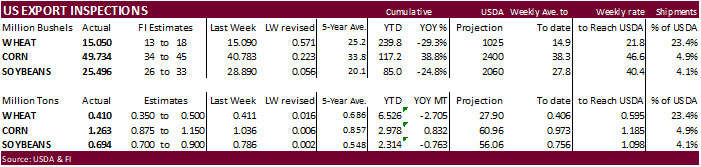

USDA inspections versus Reuters trade range

Wheat 409,592 versus 350000-500000 range

Corn 1,263,310 versus 850000-1150000 range

Soybeans 693,890 versus 550000-900000 range

· Argentina took another 30,296 tons of US soybeans

· China took 1,690 tons of corn

GRAINS INSPECTED AND/OR WEIGHED FOR EXPORT

REPORTED IN WEEK ENDING SEP 20, 2018

— METRIC TONS —

————————————————————————-

CURRENT PREVIOUS

———– WEEK ENDING ———- MARKET YEAR MARKET YEAR

GRAIN 09/20/2018 09/13/2018 09/21/2017 TO DATE TO DATE

BARLEY 0 343 0 3,547 14,122

CORN 1,263,310 1,035,928 779,971 2,977,759 2,145,906

FLAXSEED 0 0 0 170 3,623

MIXED 0 0 0 0 0

OATS 0 0 100 1,198 2,595

RYE 0 0 0 0 0

SORGHUM 3,161 1,326 130,214 5,997 249,121

SOYBEANS 693,890 786,268 1,036,653 2,313,803 3,076,382

SUNFLOWER 0 0 0 0 0

WHEAT 409,592 410,675 502,725 6,525,556 9,230,334

Total 2,369,953 2,234,540 2,449,663 11,828,030 14,722,083

————————————————————————-

CROP MARKETING YEARS BEGIN JUNE 1 FOR WHEAT, RYE, OATS, BARLEY AND

FLAXSEED; SEPTEMBER 1 FOR CORN, SORGHUM, SOYBEANS AND SUNFLOWER SEEDS.

INCLUDES WATERWAY SHIPMENTS TO CANADA.

Macros.

· Most of the US federal government could shut down at the end of this week unless Congress passes — and Trump signs — a short-term spending bill to keep $$ running.

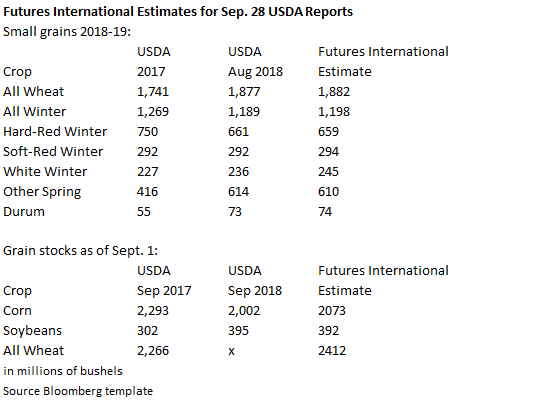

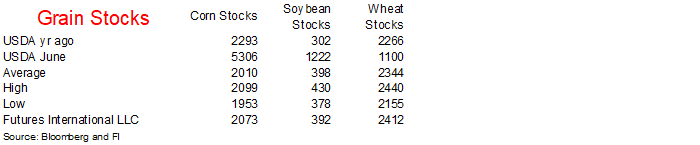

University of Illinois is at 2.020 billion bushels and 395 million bushels for US September 1 corn and soybean stocks. https://farmdocdaily.illinois.edu/2018/09/anticipating-september-1-stocks-corn-soybeans.html?utm_source=farmdoc+daily+and+Farm+Policy+News+Updates&utm_campaign=840750b5d5-EMAIL_CAMPAIGN_2018_09_04_04_03_COPY_01&utm_medium=email&utm_term=0_2caf2f9764-840750b5d5-173649469

Hubbs, T. "Anticipating September 1 Stocks for Corn and Soybeans." farmdoc daily (8):177, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, September 24, 2018.

Corn.

- Corn futures were lower after China cancelled trade talks with the US but rallied on corn/soybean spreading and higher wheat. Export inspections were above expectations.

- December corn hit its highest level since September 12 and on a rolling basis was at about a one-month high.

- Funds bought an estimated 12,000 corn contracts.

- Both interior corn and soybean basis fell at interior locations on Monday and firmed at river locations. Too much rain underpinned basis at Rivers were harvesting pressure pressured basis in the interior.

- US crude oil was higher. Brent crude traded to nearly a four-year high on Monday.

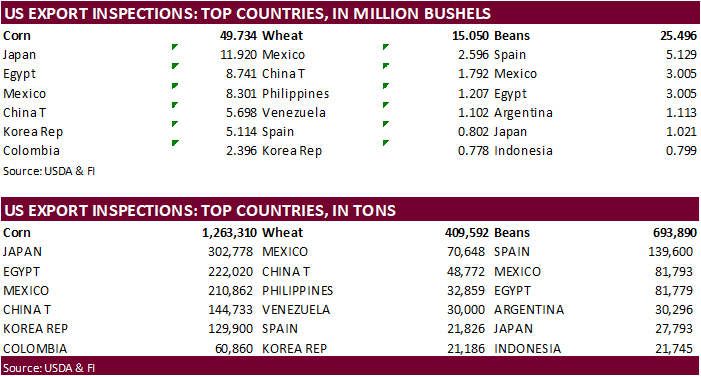

- USDA US corn export inspections as of September 20, 2018 were 1,263,310 tons, above a range of trade expectations, above 1,035,928 tons previous week and compares to 779,971 tons year ago. Major countries included Japan for 302,778 tons, Egypt for 222,020 tons, and Mexico for 210,862 tons.

· Traditional funds are now net short in corn.

· China imported 330,000 tons of corn in August, down 13.5 percent from a year ago.

· China imported 550,000 tons of barley in August, down 29 percent from a year ago.

· China imported 60,000 tons of corn in August, down 78.5 percent from 259,892 tons a year ago, and down from 220,000 tons imported in July.

- China reported more cases of African swine fever in Inner Mongolia.

- President Trump sometime over the next month is expected to announce year-round sales of E15 (ethanol), opening the June 1 to September 15 window in areas where smog is a problem.

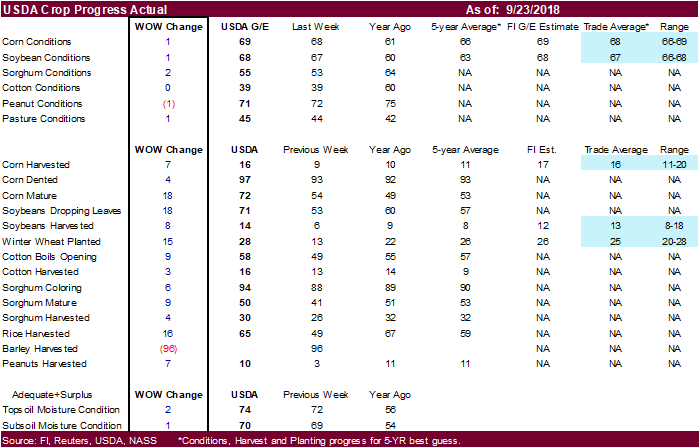

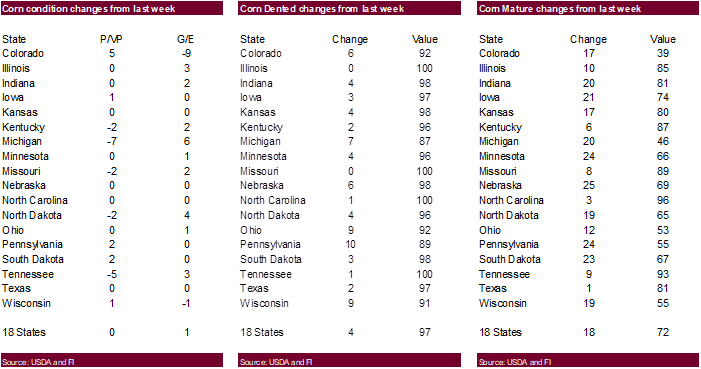

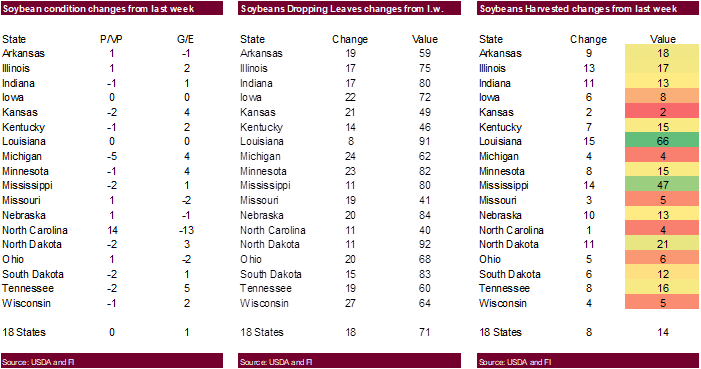

- USDA reported US corn harvesting progress at 16 percent, at a Reuters trade guess, up 7 points from the previous week and compares to 10 last year and 11 average.

- USDA reported US corn crop conditions at 69 percent, up 1 from the previous week (trade was looking for unchanged) and compares to 61 last year and 66 average.

- Our weighted crop index for US corn crop conditions ended up at 82.5 percent (82.5/100), up 0.2% from the previous week, above 80.8 a year ago and 82.0 a year ago. Using this index against a 10-year trend yield history against FI crop conditions as of or near October 1, the US yield could end up around 183.0 bushels per acre, up 0.5 bu/ac above the previous week (+8.5/bu above a 174.5 ten-year trend yield), 1.7 bushels above USDA and compares to 176.6 bushels a year ago, the current record. Using 81.620 million acres for the US corn harvested area, production could end up near 14.936 billion bushels, 110,000 bushels above USDA, assuming ratings remain unchanged from now until October 1.

· China will sell another 8 million tons of corn for the week ending September 28.

· China sold nearly 84 million tons of corn out of reserves this season.

· Soybeans were lower on ongoing US/China trade concerns. China said they will not come to the table until President Trump lays off the negative Tweets.

· There is talk of CBOT soybeans eroding below $8.00/bushel. Some people are looking for $7.50. We think $8.00 is a strong support area.

· Funds sold an estimated 6,000 soybean contracts, sold 3,000 soybean meal and bought 3,000 soybean oil.

- USDA US soybean export inspections as of September 20, 2018 were 693,890 tons, within a range of trade expectations, below 786,268 tons previous week and compares to 1,036,653 tons year ago. Major countries included Spain for 139,600 tons, Mexico for 81,793 tons, and Egypt for 81,779 tons.

· WTI crude oil was higher with the nearby over $72/barrel, highest level since early July.

· Some Argentina crush workers are back on strike for 24-hours in or near Rosario.

· China and Japan were on holiday.

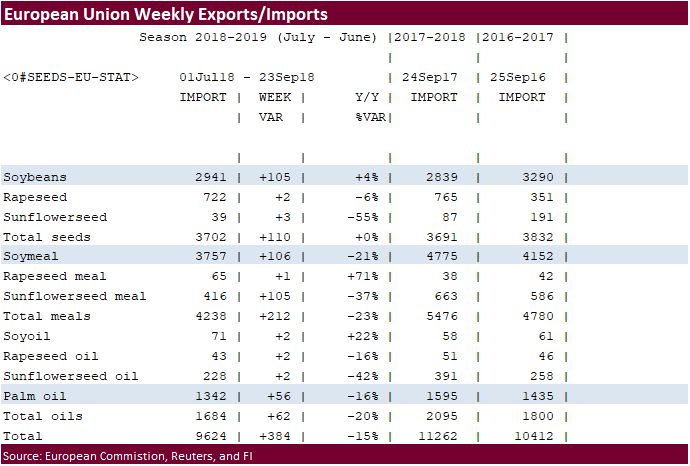

· The European Union reported soybean import licenses since July 1 at 2.941 million tons, above 2.839 million tons a year ago. European Union soybean meal import licenses are running at 3.757 million tons for 2018-19, below 4.775 million tons a year ago. EU palm oil import licenses are running at 1.342 million tons for 2018-19, down from 1.595 million tons a year ago.

· USDA reported US soybean harvesting progress at 14 percent, 1 point above a Reuters trade guess, and compares to 9 last year and 8 average.

· USDA reported US soybean crop conditions at 68 percent, up one point from the previous week (trade was looking for unchanged) and compares to 60 last year and 63 average.

· Our weighted crop index for US soybean crop conditions is running at 82.4 percent (82.4/100), 0.2 bu/ac above last week, above 80.5 a year ago and 81.4 average. Using this index against a 15-year trend yield history against FI crop conditions as of or near October 1, the US yield could end up near 53.3 bushels per acres (3.6/bu above the 49.7 fifteen-year trend yield), 0.5 bushel above USDA and compares to 49.1 bushels a year ago. Using 88.628-million-acre soybean harvested area, production could end up near 4.724 billion bushels, if ratings remain unchanged from now until October 1. Our production estimate is 31 bushels above USDA.

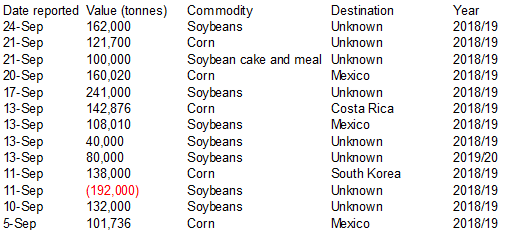

- Under the 24-hour reporting system, US private exporters reported the sale of 162,000 tons of soybeans for delivery to unknown destinations during the 2018-19 marketing year.

- Egypt’s GASC seeks at least 30,000 tons of soyoil and 10,000 tons of sunflower oil for arrival between Oct. 25 and Nov. 10,

- Results awaited: Iran seeks 30,000 tons of sunflower oil on September 24.

- China sold about 2.38 MMT of soybeans out of reserves this season.

· US wheat traded higher on spreading against soybeans, higher Russian wheat prices in comparison to the previous week, and another downgrade to the Australian wheat crop by one of the banks (National Bank of Australia to 18.1MMT; USDA @ 20.0). They are lowest we have seen.

- Chicago December wheat hit its highest level since September 12 and on a rolling basis was at about a one-month high.

- Funds bought 5,000 SRW wheat.

· EU wheat closed higher by 1.25 euros to 203.00 following Chicago but gains were limited with the euro trading at its highest level in about 3 months.

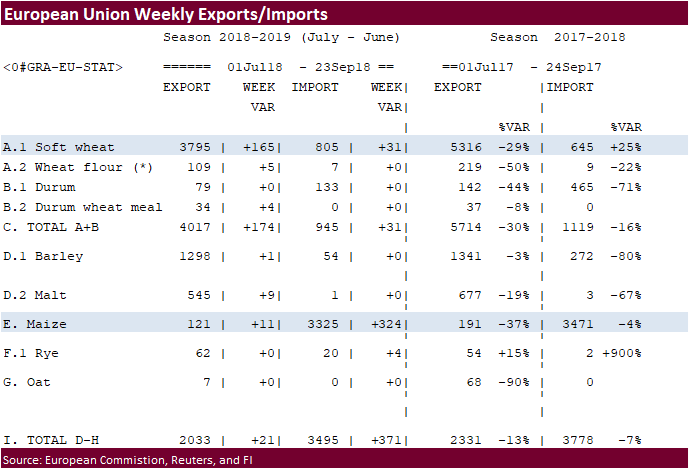

· The European Union granted export licenses for 165,000 tons of soft wheat imports, bringing cumulative 2018-19 soft wheat export commitments to 3.795 million tons, well down from 5.316 million tons committed at this time last year.

· IKAR reported 12.5 percent Russian wheat up $3.00/ton to $220/ton.

- USDA US all-wheat export inspections as of September 20, 2018 were 409,592 tons, within a range of trade expectations, below 410,675 tons previous week and compares to 502,725 tons year ago. Major countries included Mexico for 70,648 tons, China T for 48,772 tons, and Philippines for 32,859 tons.

· China imported 140,000 tons of wheat in August, down 52 percent from a year ago.

· India monsoon rains are starting to wind down.

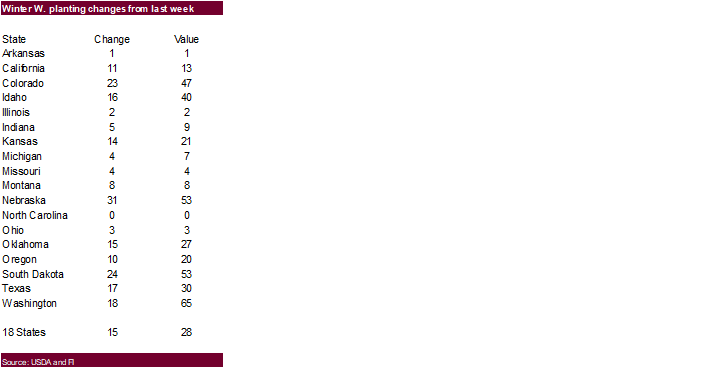

· USDA reported US winter wheat planting at 28 percent, up 15 points from the previous week, 3 points above a trade average and compares to 22 last year and 26 average.

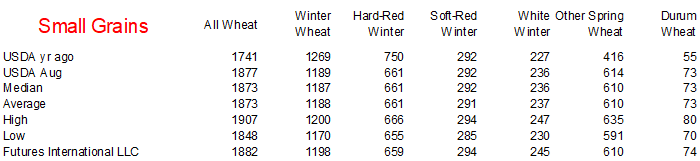

Our 2019 US wheat planting estimates in million acres:

· Winter Wheat 33.625

· HRW 24.000

· SRW 6.050

· HRS 13.100

· Winter White 3.575

· Spring White 0.600

· Durum 2.100

· All-Wheat 49.425

- UAE seeks 60,000 tons of wheat on September 24 for Oct/Nov shipment.

- Bahrain seeks 25,000 tons of wheat on October 2 for Nov shipment.

- Canadian wheat is the lowest offer in Iraq’s import tender. Lowest was $337/ton. Offers valid until September 27. Iraq needs wheat for four after Turkey restricted flour shipments.

- Results awaited: Ethiopia seeks 200,000 tons of milling wheat for shipment two months after contract signing. Ethiopia got offers from 7 firms. Lowest offer was for 100,000 tons at $272.05/ton, c&f.

· Results awaited: Turkey seeks a total of 252,000 tons of red milling wheat for October 2-22 loading. It closes on September 22. The depreciation of the lira sent importers seeking Turkish wheat flour, causing them to restrict exports. But countries like Iraq that heavily depend on flour from Turkey may have to import from other countries.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on September 26 for arrival by late February.

- Jordan seeks 120,000 tons of feed barley, optional origin, on September 26.

- Jordan seeks 120,000 tons of feed wheat, optional origin, on September 27.

- Iraq seeks 50,000 tons of wheat on September 23, with offers valid until September 27. Iraq needs wheat for four after Turkey restricted flour shipments.

- Morocco seeks 336,364 tons of US durum wheat on September 28 for arrival by December 31.

Rice/Other

· The Philippines are increasing rice imports by securing 500,000 tons on top of 250,000 they previously had planned to buy.

· Mauritius seeks 9,000 tons of rice for delivery between Nov. 15, 2018, and March 31, 2019, set to close is Sept. 27.

· Iraq seeks 30,000 tons of rice optional origin on October 1, valid until October 7.

· Iraq seeks 30,000 tons of rice from India on October 9 for LH October / FH November shipment.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.