From: Terry Reilly

Sent: Tuesday, December 24, 2019 1:10:40 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 12/24/19

PDF attached

Happy Holidays!

CBOT will reopen Thursday morning.

CME Group Holiday Calendar

https://www.cmegroup.com/tools-information/holiday-calendar.html

From World Weather Inc.

MARKET WEATHER MENTALITY FOR CORN AND SOYBEANS:

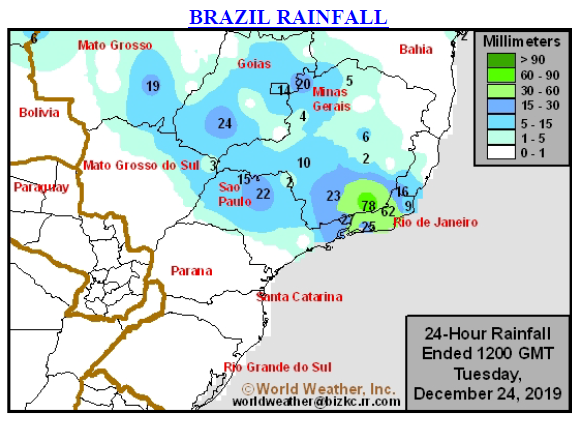

Brazil and Argentina weather will be favorable over the next two weeks, although the ridge of high pressure in southern Brazil will have to be monitored this week to make sure it is only going to prevail this workweek. If it stays too long there could be a negative impact on some crops.

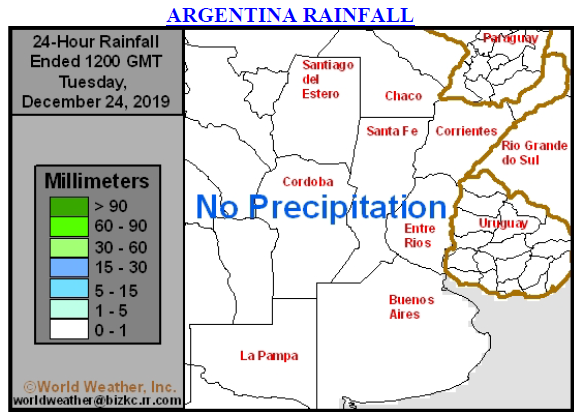

Argentina should see timely rainfall in most of the nation over the next two weeks, although there will still be areas of lighter than desired rainfall. Temperatures will be warm, but not excessively hot. Crops are still stressed in the southwest, despite some recent rain. More precipitation is needed in all central and southern crop areas.

South Africa rainfall will be erratic over the next ten days leaving some areas a little too dry while some beneficial crop and field conditions evolve in other areas.

Eastern Australia’s summer coarse grain and oilseed crops have been stressed in recent heat and dryness, but irrigated areas remain in the best shape. Rain later this week will likely be too close to the coast to benefit very many crops, but some eastern sorghum might benefit from a little rain this workweek. Temperatures will not be as oppressively hot this week in eastern crop areas.

Winter rapeseed conditions have not changed much in Europe central Asia of China, but some rain in each of these areas will either improve crop conditions later this week or in the spring when seasonal warming returns.

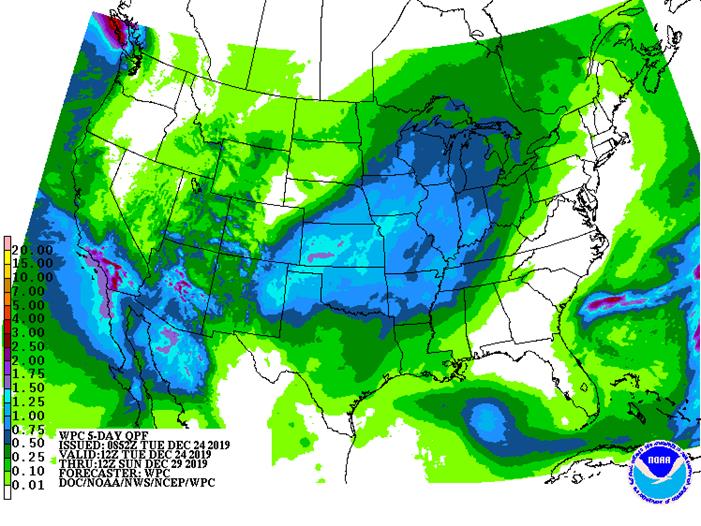

Late season harvest progress in the U.S. will only be able to advance slowly in the next couple of weeks. Warm temperatures and limited precipitation through mid-week this week will help some areas. Snow melt and muddy field conditions will not allow much progress, however.

Overall, weather today will likely support a mixed influence on market mentality.

MARKET WEATHER MENTALITY FOR WHEAT AND OTHER SMALL GRAINS:

Winter wheat conditions in the west-central and southwestern U.S. Plains may improve later this week if the southwestern U.S. storm comes into the Plains as advertised today. The region needs moisture for improved crop establishment in the spring.

Additional rain in the Midwest later this week will maintain wet field conditions in soft red wheat production areas. Crop conditions will not change much, although rising soil temperatures may reduce winter hardiness as this week moves along especially in the south.

Argentina wheat harvesting will advance relatively well for a while as rainfall continues erratic and light. Last week’s rain briefly disrupted harvest progress, but might have been good for the most immature crops

Turkey and Syria will receive some needed rain this week improving their establishment potential. Most other areas in the Middle East have seen a good mix of weather this season.

Winter crops in Eastern Europe and the western CIS will not be vulnerable to any winterkill this week as temperatures remain well above average. Snow cover remains minimal

North Africa wheat is rated favorably, but more rain is needed in southwestern Morocco, Tunisia and some interior eastern Algeria locations.

Recent rain in Spain and Portugal has improved winter crop prospects for early spring crop development in February. Additional rain would be welcome.

Overall, weather today will likely produce a slightly bearish bias to market mentality..

Source: World Weather Inc. and FI

Source: World Weather Inc. and FI

Source: World Weather Inc. and FI

- Unica cane crush, sugar production

- U.S. poultry slaughter, 3pm

WEDNESDAY, Dec. 25:

- Christmas Day

THURSDAY, Dec. 26:

- Boxing Day

- AmSpec releases Malaysia’s Dec. 1-25 palm oil export data, 10pm Monday (11am Kuala Lumpur); SGS data due at 3pm KL

FRIDAY, Dec. 27:

- USDA weekly crop net-export sales for corn, soybeans, wheat, 8:30am

- EIA U.S. weekly ethanol inventories, production, 11am

- U.S. agricultural prices paid, received, 3pm

- ICE Futures Europe weekly commitments of traders report on coffee, cocoa, sugar positions ~1:30pm (~6:30pm London)

SATURDAY, Dec. 28:

- Nothing major scheduled

SUNDAY, Dec. 29:

- Nothing major scheduled

MONDAY, Dec. 30:

- USDA weekly corn, soybean, wheat export inspections, 11am

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

TUESDAY DECEMBER 31

- AmSpec releases Malaysia’s Dec. 1-31 palm oil export data, 10pm Monday (11am Kuala Lumpur); SGS data due at 3pm KL

WEDNESDAY, Jan. 1:

- Nothing major scheduled

THURSDAY, Jan. 2:

- Australia commodity index

- USDA Soybean crush, DDGS production, corn for ethanol, 3pm

FRIDAY, Jan. 3:

- USDA weekly crop net-export sales for corn, soybeans, wheat, 8:30am

- EIA U.S. weekly ethanol inventories, production, 11am

- ICE Futures Europe weekly commitments of traders report on coffee, cocoa, sugar positions ~1:30pm (~6:30pm London)

Source: Bloomberg and FI

· Philadelphia Fed Non-Manufacturing Regional Business Activity Index 13.4 In Dec Vs 20.7 In Nov

· Fed Wage And Benefit Cost Index 45.3 In Dec Vs 36.7 In Nov

· NY Fed Accepts All Of $24.80 Bln In Bids At Overnight Repo Operation

Corn

· Despite the USDA reporting a large US hog and pig population as of December 1, CBOT corn futures traded lower. The reversal in soybeans did little to support corn.

· Funds sold an estimated net 4,000 corn contracts on the session.

· China approved DDGS imports from Bulgaria.

· AKIpress News Agency noted 1,000 tons of Kazakh corns was exported via train in containers to China, first shipment by train in history, a move that represents logistical improvement and opens the door for agriculture trade between both countries. China’s appetite for corn has increased in recent years and they no long rely solely on SA, Ukraine and US corn.

· The Baltic Dry Index fell to a 6-month low to 1,090 points, down roughly 14 percent for this year.

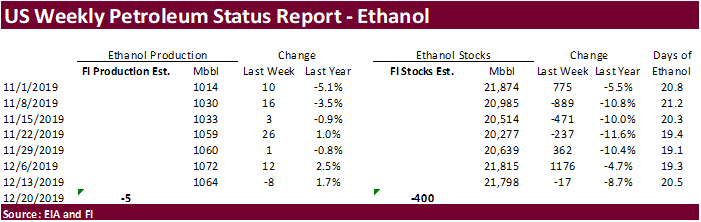

· A Bloomberg poll looks for weekly US ethanol production to be unchanged at 1.064 million barrels from the previous week and stocks to increase 70,000 barrels to 21.877 million.

- South Korea’s MFG bought 66,000 tons of optional origin corn at around $209.74 a ton c&f for arrival in South Korea around April 1, 2020.

- India’s NAFED seeks 100,000 tons of corn from Ukraine on December 3 with offers valid until December 24 for shipment between Jan. 10 and Jan. 31.

Soybean complex.

· The soon expiring January CBOT soybean contract traded at a fresh 6-week high after opening lower. March soybean failed to test its 6-week high. Follow through support from slow US producer selling was noted. Soybean meal and oil were turned higher as well. Egypt is in for vegetable oils. CBOT March soybean oil is back near its contract high.

· Funds bought an estimated 3,000 soybeans, bought 1,000 soybean meal and bought 2,000 soybean oil.

· The Jan/Mar spread was last 8.25, March premium. There were no changes in soybean registrations, but the 110 soybeans came out of Chicago yesterday now have been related to the 22 barges making their way to the Gulf as we were told Chicago is the cheapest origin. Looking at soybean basis at crush plants, they are up at several locations from the previous week. This tells us the producers are getting friendly soybeans, perhaps on the US/China trade deal announcement, and we don’t see them selling until the beginning of 2020 anyway. US producers also have more incentive to sell the July contract with current cost of carry. We think the Jan/Mar soybean spread may narrow to 7.00-7.25 cents.

· Traders will be monitoring the high-pressure ridge over Brazil this week as it could yield beneficial rainfall for Argentina, if the ridge drifts into Argentina during the weekend and next week.

- Egypt’s GASC seeks 30,000 tons of soyoil and 10,000 tons of sunflower oil on December 30 for arrival on Feb. 5-20. They are in for local vegetable oils as well.

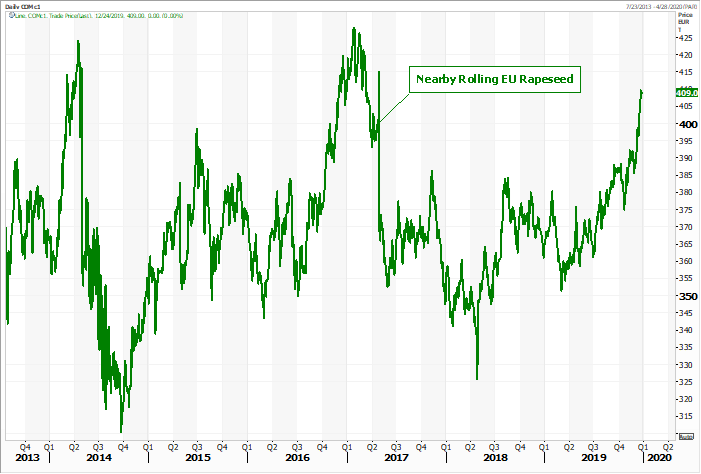

EU Rapeseed

Source: Refiniv and FI

- CBOT March soybeans are seen in a $9.00-$9.60 range

- March soybean meal $295-$315 range

- March soybean oil 33.00-36.00 range

- Upside on oil share is seen at 36.5 percent (lowered half percent)

Wheat

· After a two-sided trade on Monday, US wheat futures appreciated on technical buying and a smaller than expected Russian wheat crop. Morocco will lower its import duty on soft wheat early January.

· Funds bought an estimated net 1,000 wheat on the session.

· March Paris wheat futures settled up 0.25 euro or 0.3% at 187.25 euros a ton.

· Reuters: Russian state-controlled grain trader United Grain Company (UGC) has drafted a new strategy aimed at increasing its own grain purchases and trade to 8 million tons a year by 2024, Russian daily the Kommersant reported on Monday.

· Russia’s government reported the wheat crop for 2019-20 at 74.3 million tons, below the Deputy Prime Minister’s previous statement of around 75 million tons.

· A winter storm is expected in the U.S. central and southwestern Plains late this week and into the weekend. Heavy snow is expected from Colorado to Nebraska.

· China’s Shanghai Futures Exchange will loosen trading position limits on product contracts next year to encourage trading.

Export Developments.

- Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF) in an SBS import tender on December 25 seeks 120,000 tons of feed wheat and 200,000 tons of feed barley for arrival in Japan by March 12.

- Mauritius seeks 95,000 tons of optional origin wheat flour on Jan. 10, 2020, for shipment between July 1, 2020, and June 20, 2021.

· Syria seeks 200,000 tons of soft wheat from Russia on January 20, 2020. They are in for 150,000 tons of wheat from Russia on December 18.

Rice/Other

Details of the tender are as follows:

TONNES(M/T) GRAIN TYPE ARRIVAL/PORT

3,000 Milled Long April 30, 2020/Busan

17,000 Milled Medium June 30, 2020/Busan

22,222 Brown Medium June 30, 2020/Busan

- Syria seeks 45,000 tons of white rice on Jan. 6, 2020. (Reuters) Short grain white rice of third or fourth class was sought. No specific country of origin was specified in the tender, traders said. Some 25,000 tons was sought for supply 90 days after confirmation of the order and 20,000 tons 180 days after supply of the first consignment. The rice was sought packed in bags and offers should be submitted in euros. A previous tender from the agency for 45,000 tons of rice with similar conditions had closed on Nov. 13.

Updated 12/17/19

· CBOT Chicago March wheat is seen in a $5.30-$5.80 range

· CBOT KC March wheat is seen in a $4.60-$4.85 range

· MN March wheat is seen in a $5.25-$5.55 range

· We like KC wheat over Chicago wheat.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.