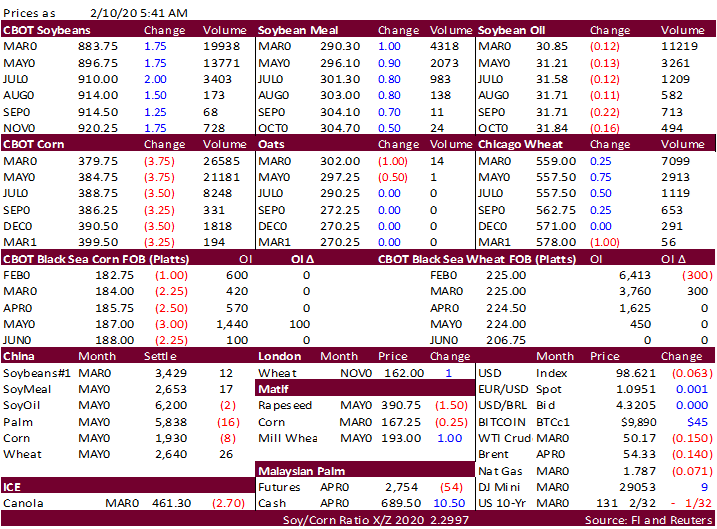

FW: FI Morning Grain Comments 02/10/20 Feb 10, 2020 From: Terry Reilly Sent: Monday, February 10, 2020 8:06:20 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 02/10/20 PDF attached Morning. USDA is due out with updated S&D’s on Tuesday. Soybeans turned lower after trading up six straight sessions overnight, while corn and wheat are on the defensive. Look for a choppy but slow trade today.