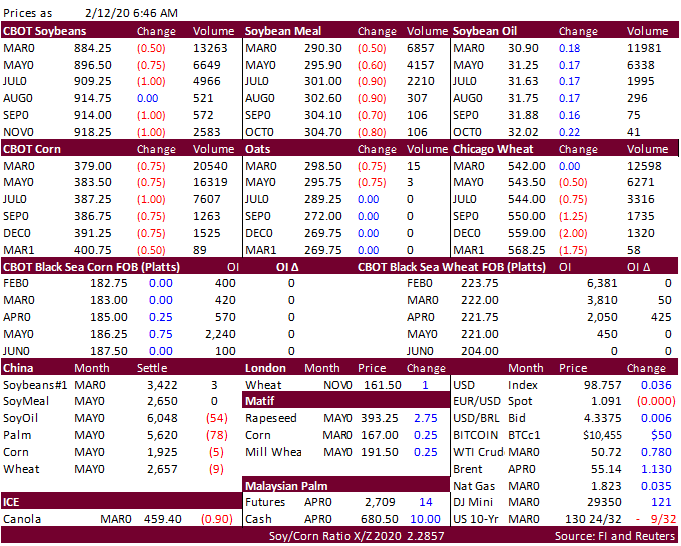

FW: FI Morning Grain Comments 02/12/20 Feb 12, 2020 From: Terry Reilly Sent: Wednesday, February 12, 2020 8:21:26 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 02/12/20 PDF attached Morning. Global tenders increased especially in soybean meal and corn. The pace of the coronavirus spread is slowing but deaths continue to rise. China officials are asking local crushers to resume operations, if they have not already.