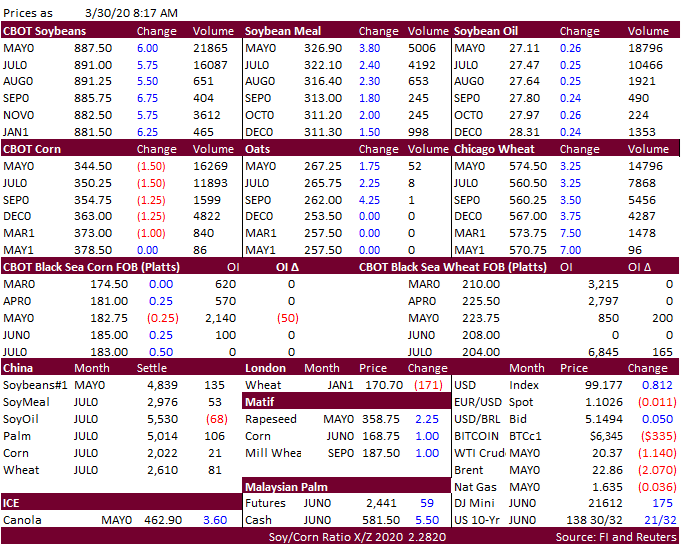

FW: FI Morning Grain Comments 03/20/20 Mar 30, 2020 From: Terry Reilly Sent: Monday, March 30, 2020 8:18:38 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 03/20/20 PDF attached Morning. China cut rates for loans to banks. EU bond buying was active. US traders will be watching the bond markets this week. USD is higher and US stocks are higher. VIX remains above 60. Brent crude hit a 17-year low. Russian wheat export prices surged $10/ton to $217/ton fob-SovEcon. China soybean crush margins are higher from Friday. Vietnam bought corn from Ukraine late last week.