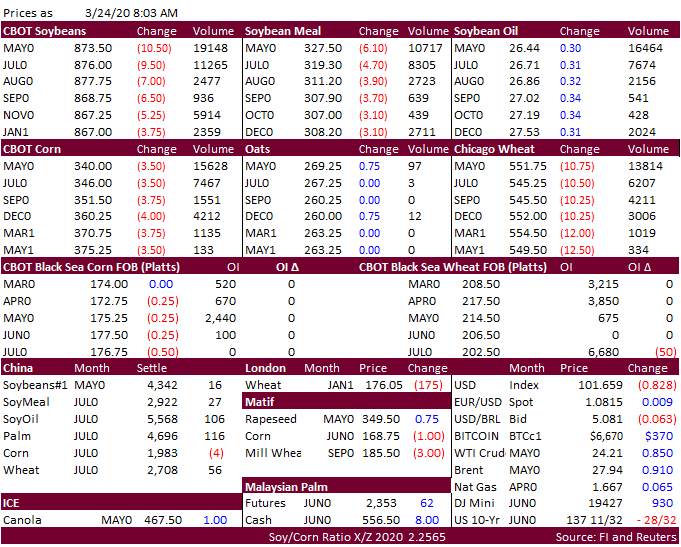

FW: FI Morning Grain Comments 03/24/20 Mar 24, 2020 From: Terry Reilly Sent: Tuesday, March 24, 2020 8:05:19 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 03/24/20 PDF attached Morning. US Feds are rolling out additional stimulus packages. Gold is up $99. US stocks are higher. WTI was more than $1.00 higher. Traders are waiting to see what Washington will do with the relief package.