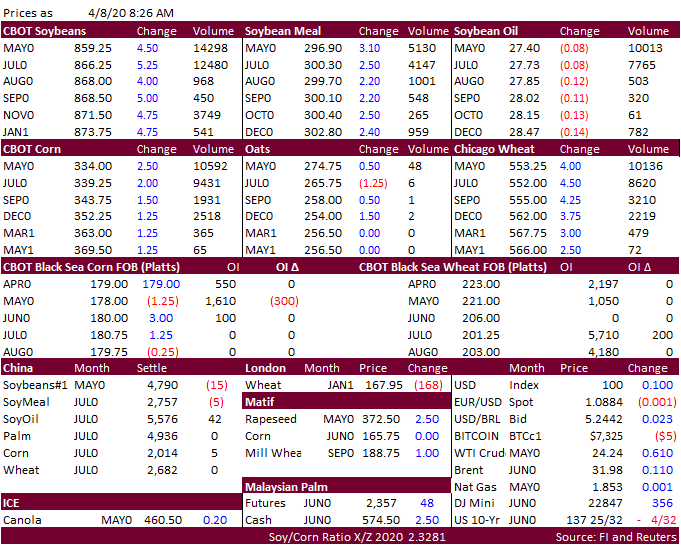

FW: FI Morning Grain Comments 04/08/20 Apr 8, 2020 From: Terry Reilly Sent: Wednesday, April 08, 2020 8:27:39 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 04/08/20 PDF attached Morning. USD is higher. Sinograin is releasing 500,00 tons of soybeans to Cofco from state reserves. SK bought more corn.