From: Terry Reilly

Sent: Tuesday, July 17, 2018 8:13:13 AM (UTC-06:00) Central Time (US & Canada)

Subject: FI Morning Grain Comments 07/17/18

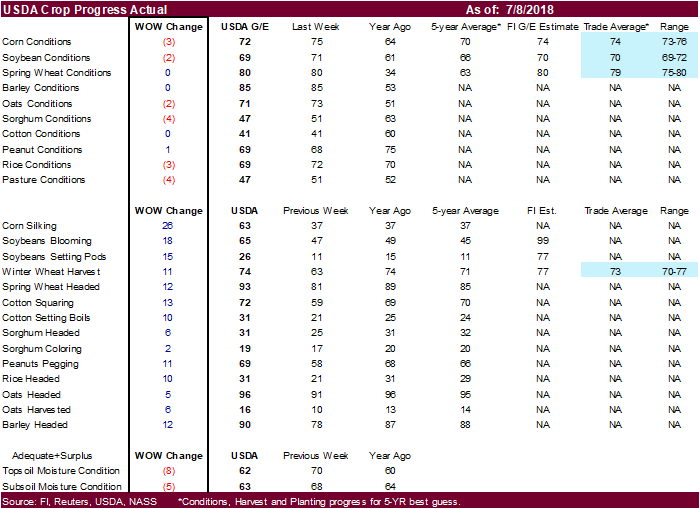

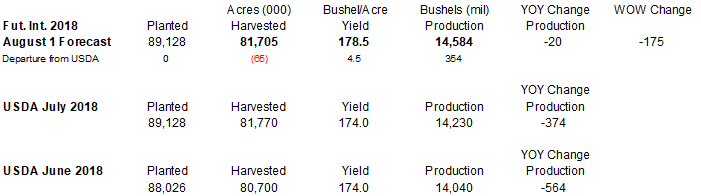

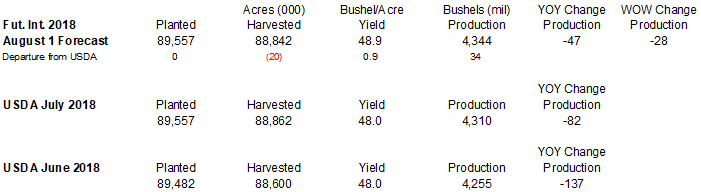

· Corn down 3. We dropped our US corn yield by 2.0 bu/ac and lowered production by 175 million.

· Soybeans down 2. We dropped our US soybean yield by 0.3 bu/ac and lowered production by 28 million.

· WW Harvest @ 74 vs. 63 LW

· Spring unchanged (good up 1 & exc. down 1)

· Subsoil moisture levels are now below a year ago

http://usda.mannlib.cornell.edu/usda/current/CropProg/CropProg-07-16-2018.pdf

· The U.S. Pacific northwest and northwestern U.S. Plains will be dry or mostly dry during the next ten days

· Net drying will continue across the southwestern Corn Belt and the southern Plains.

· The Delta and southeastern states will see a mix of rain and sunshine.

· The northwestern Plains will see an increase of net drying.

· We are hearing lack of corn tasseling across WI. Feedback is welcome.

· The Canada Prairies will see net drying across the southern crop areas. Western and northern Alberta will be wettest.

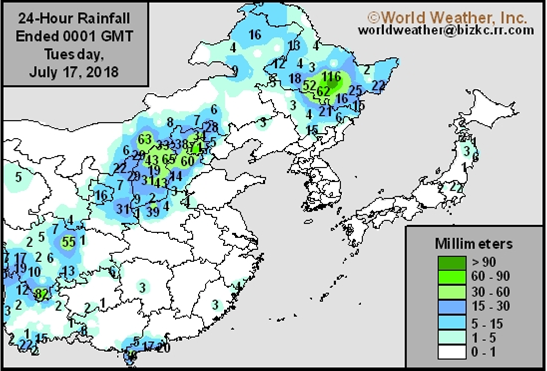

· East-central China will continue to see net drying this week but the Northeast Provinces will improve with rain.

· Frequent rain will fall from eastern Europe through the western CIS this week.

· Western Europe will trend wetter this week.

Source: World Weather Inc. and FI

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Tue 5-15% daily cvg of up

to 0.30” and locally

more each day;

wettest south

Tue-Wed Mostly dry with a few

insignificant showers

Wed-Fri 80% cvg of up to 0.75”

and local amts to 1.50”

with a few bands of

1.50-3.0”; far SE and

far NW driest

Thu-Sat 85% cvg of up to 0.75”

and local amts to 2.0”

Sat Mostly dry with a few

insignificant showers

Sun 20% cvg of up to 0.25”

and locally more;

wettest east

Sun-Jul 24 60% cvg of up to 0.60”

and local amts to 1.30”

Jul 23-25 60% cvg of up to 0.50”

and local amts to 1.10”

Jul 25 15% cvg of up to 0.20”

and locally more

Jul 26 15% cvg of up to 0.20”

and locally more

Jul 26-27 55% cvg of up to 0.70”

and locally more

Jul 27-29 65% cvg of up to 0.75”

and locally more

Jul 28-30 40% cvg of up to 0.60”

and locally more

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy-Wed 75% cvg of up to 0.70” 85% cvg of up to 0.75”

and local amts to 1.50”; and local amts to 1.50”

far north and far south with a few bands of

driest 1.50-3.0”; wettest

south

Thu 20% cvg of up to 0.75”

and local amts to 1.50”;

wettest SE

Thu-Fri 40% cvg of up to 0.50”

and local amts to 1.30”;

wettest north

Fri-Sat 75% cvg of up to 0.75”

and local amts to 1.75”;

driest west

Sat-Jul 23 Up to 15% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Sun-Jul 23 10-25% daily cvg of

up to 0.35” and locally

more each day; Va.

and Carolinas wettest

Jul 24-25 40% cvg of up to 0.50” 60% cvg of up to 0.75”

and local amts to 1.10” and local amts to 1.50”

Jul 26-27 10-25% daily cvg of

up to 0.30” and locally

more each day

Jul 26-28 15-35% daily cvg of

up to 0.60” and locally

more each day

Jul 28-30 50% cvg of up to 0.60”

and locally more

Jul 29-31 60% cvg of up to 0.75”

and locally more

Source: World Weather Inc. and FI

Source: World Weather Inc. and FI

TUESDAY, JULY 17:

- New Zealand dairy auction on Global Dairy Trade online market starts ~7am ET (~noon London, ~11pm Wellington)

WEDNESDAY, JULY 18:

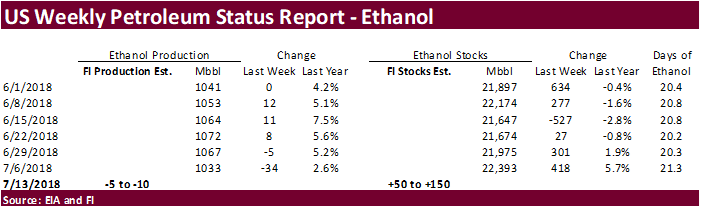

- EIA U.S. weekly ethanol inventories, output, 10:30am

THURSDAY, JULY 19:

- Nicaragua on holiday

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- USDA red meat production for June, 3pm

- National Confectioners Association North America 2Q cocoa grind, ~4pm

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, JULY 20:

- Colombia on holiday

- Cocoa Association of Asia is set to release 2Q cocoa grind data

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- USDA milk production for June, 3pm

- USDA cattle on feed for June, 3pm

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- FranceAgriMer weekly updates on French crop conditions

Source: Bloomberg and FI

· Rice down 71 to 214

· US stocks are lower, USD higher, WTI crude unchanged to higher, and gold higher, at the time this was written.

· Canadian Manufacturing Sales (M/M) May: 1.4% (est 0.4%; prev R -1.1%)

Corn.

- Corn prices are higher after USDA reported a drop in US G/E conditions.

- Baltic Dry Index was 26 points higher to 1,721, or 1.5%.

- USDA US corn export inspections as of July 12, 2018 were 1,217,233 tons, within a range of trade expectations, below 1,467,222 tons previous week and compares to 1,122,852 tons year ago. Major countries included Mexico for 265,167 tons, Japan for 254,101 tons, and Peru for 126,646 tons.

- USDA corn conditions fell 3 points to 72, 2 points below the trade average.

· We dropped our US corn yield by 2.0 bu/ac to 178.5 and lowered production by 175 million.

· Planalytics increased their yield to 176.2 bu/ac from 174.0.

· Subsoil moisture levels are now below a year ago

· China sold about 52-53 million tons of corn out of reserves this season.

Soybean complex.

· Soybean prices continue to rebound after nearly hitting a decade low. USDA lowered US G/E soybean conditions which is supportive.

· The soybean export prices for Brazil premium US widened to $68/ton as of early Monday for August shipment, leading some to think another $3-$5/ton move will attract China to buy US soybeans. Brazil producers have been reserved sellers of soybeans as of recent, but there is growing fear that the premium will disappear if the US and China settled the trade disputes. Meanwhile, Oil World shortened their timetable when SA supplies dry up to around the end of August.

· Brazil is on track to export nearly 11 million tons of soybeans in July. FH July shipments reached 5.3MMT versus 3.38MMT a year ago.

· US domestic demand for soybeans is very good. Exports are hanging in there as lower prices are attracting traditional and non-traditional buyers. At $8.50 basis the November, look for importing countries other than China to take advantage.

· It’s starting to get a little too dry across SE Asian palm growing regions.

· China September soybean futures increased 23 yuan per ton or 0.7%, September meal was up 36 or 1.2%, China soybean oil up 28 (0.5%) and China September palm up 40 (0.9%).

· September China cash crush margins were last running at 40 cents, up from 36 previous session, and compares to 39 cents last week and 78 a year ago.

· Rotterdam vegetable oils were unchanged to lower and SA soybean meal when delivered into Rotterdam higher as of early morning CT time.

· September Malaysian palm was 2 lower at MYR2171 and cash unchanged at $558.75/ton.

· Offshore values were leading soybean oil 26 points higher and meal $0.50/short ton lower.

- USDA US soybean export inspections as of July 12, 2018 were 635,429 tons, within a range of trade expectations, below 668,014 tons previous week and compares to 299,639 tons year ago. Major countries included Mexico for 130,161 tons, Indonesia for 81,417 tons, and China T for 81,396 tons. 2.0 million bushels or nearly 55,000 tons of soybeans were inspected for China.

- USDA soybean conditions fell 2 points to 69, 1 point below the trade average.

· We dropped our US soybean yield by 0.3 bu/ac to 48.9 and lowered production by 28 million.

· Planalytics increased their yield to 49.5 bu/ac from 49.0.

· Subsoil moisture levels are now below a year ago.

- China sold 54,706 of rapeseed oil out of 61,000 tons offered at an average price of 6077 yuan per ton, or $908.60/ton, 87 percent of the total.

· China sold 832,302 tons of soybeans out of reserves so far, this season.

- The CCC seeks 12,500 tons of soybean meal for Honduras, opened until July 18, for early October shipment.

- Results awaited: Iran seeks 30,000 tons of sunflower oil on July 10.

- Results awaited: Iran seeks 30,000 tons of palm olein oils on July 10.

- Iran seeks 30,000 tons of soybean oil on August 1.

- South Korea seeks 1,500 tons of non-GMO soybeans on July 25 for September-December delivery.

· US wheat futures are higher following soybeans and ongoing global crop concerns, despite weather improving for some major exporting regions.

· Australia will see another round of net drying in eastern Australia, threatening crop establishment.

· Rain prospects increase this week for Rain in western Russia, Belarus, Poland and western Ukraine. Dry and warm weather for the northwestern US Plains, PNW, and Canadian southern Prairies are threatening yields.

· Manitoba, Canada, crop report said hot temps have advanced crops but the province would benefit from a good rain. They are also monitoring diseases and insect activity.

- December Paris wheat was up 0.75 euros to 186.75 euros during early US trading hours.

- USDA US all-wheat export inspections as of July 12, 2018 were 469,523 tons, above a range of trade expectations, above 268,221 tons previous week and compares to 594,705 tons year ago. Major countries included Philippines for 122,313 tons, Japan for 117,357 tons, and Mexico for 72,739 tons.

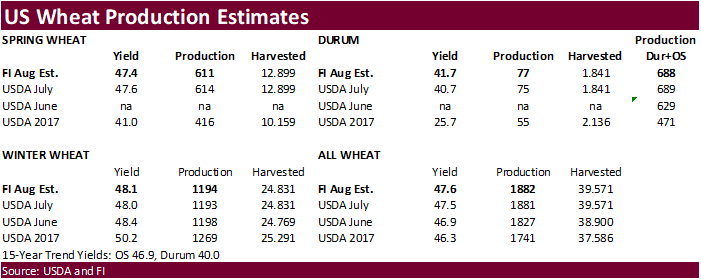

- USDA spring wheat conditions were unchanged at 80, 1 point above the trade average.

- USDA winter wheat harvest advanced 11 points to 74 percent, one point above the trade average.

· Jordan passed on 120,000 tons of barley for Oct/Nov shipment.

- China sold 954 tons of imported wheat from state reserves at auction at an average price of 2350 yuan/per ton or $352.05/ton, 0.05 percent of what was offered.

- Japan seeks 57,914 tons of US food wheat on Thursday for September loading.

· Yesterday Saudi Arabia bought 625,000 (595,000 tons sought) of wheat at an average $256.57/ton C&F.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on July 18 for arrival by December 28.

· Jordan seeks 120,000 tons of wheat on July 19 for Oct-Nov shipment.

- Bangladesh seeks 50,000 tons of optional origin milling wheat on July 25 for shipment within 40 days of contract signing.

Rice/Other

· Results awaited: Mauritius seeks 6,000 tons of white rice for Sep 1-Nov 30 shipment.

- Thailand seeks to sell 120,000 tons of raw sugar on July 18.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.