From: Terry Reilly

Sent: Monday, August 20, 2018 9:18:31 AM (UTC-06:00) Central Time (US & Canada)

Subject: FI Morning Grain Comments 08/20/18

PDF attached

World Weather Inc. Highlights

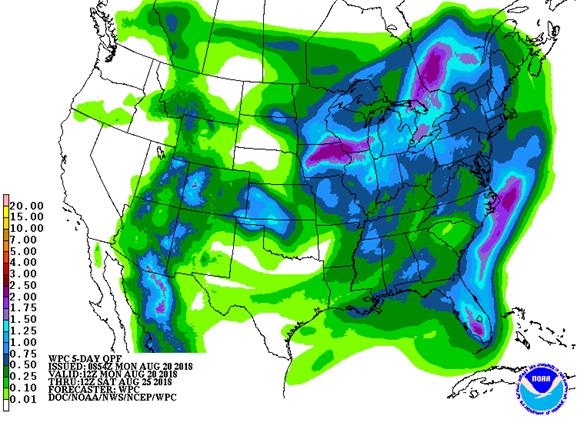

· U.S. bottom line remains good for late season coarse grain and oilseeds from the Midwest into the Delta and southeastern states. Drought is not likely to budge in the northern Plains or Canada’s Prairies and Texas long term dryness will remain in place. The environment is status quo which leaves late season crops in the northern Plains, Canada’s Prairies and the southern U.S. Plains at risk of production cuts, but goo yielding crops are likely from many other areas. Planting prospects for early season winter wheat planting in the Plains are very good, but rain is likely to decrease in September

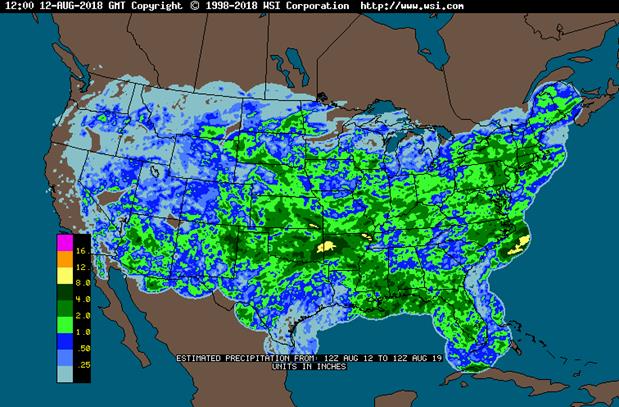

· Torrential rainfall occurred Sunday into this morning in east-central Nebraska and west-central into southwestern Iowa

· Rain totals of 3.00 to 7.72 inches occurred over several counties not far from Omaha, Nebraska

· Many surrounding areas of western Iowa and eastern Nebraska reported 1.00 to 2.50 inches of rain

· Rain also fell significantly over portions of the central Delta where 3.00 to 8.65 inches resulted through dawn today

· Flooding occurred in each of these heavy rainfall areas

· Eastern Australia’s rainfall potential for late this week has improved in both probability and quantity

· Eastern Queensland and northeastern New South Wales will receive significant rain to ease dryness, but western portions of these crop regions will remain quite dry

o Rainfall of 1.00 to 2.00 inches is possible from the Darling Downs region of northeastern New South Wales into interior far southeastern crop areas of Queensland

· Some locally greater amounts will also occur

· Western Australia’s rain potentials for next week are a little better than advertised Sunday

· Canada’s Prairies may receive some needed rain next week, but it comes too late for many areas and the precipitation is expected to be a little too light and erratic for the best results

· Frost and a few unconfirmed light freezes were reported from parts of crop country northeastern Alberta into northwestern Saskatchewan, Canada Sunday morning

· Some damage to immature canola and other crops "may" have occurred, but the impact should have been minimal

· Northeast China may be more significantly impacted from remnants of Typhoon Soulik Thursday into Saturday as the remnant low pressure center settles over the region

· Rainfall of 2.00 to more than 4.00 inches may impact a part of the region with locally greater amounts near the North Korea and Russia border

· Some of the same southern border areas are getting heavy rain from the remnants of Tropical Storm Rumbia today with some of that heavy rain beginning Sunday

· Ridge building in North America next week has been slightly reduced in amplitude today, but warmer temperatures are still predicted

· Additional beneficial rain fell in northwestern India Sunday further improving soil and crop conditions

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy 70% cvg of up to 0.75”

and local amts over 2.0”;

east-central Neb. to

south-central Mn.

wettest; far NW driest

Tdy-Tue 90% cvg of up to 0.75”

and local amts over 1.75”;

driest west

Tue 15% cvg of up to 0.20”

and locally more;

wettest NE

Wed Mostly dry with a few

insignificant showers

Wed-Thu 5-20% daily cvg of up

to 0.25” and locally

more each day

Thu-Fri 75% cvg of up to 0.75”

and local amts to 1.75”;

north and far south

wettest

Fri-Sat 50% cvg of up to 0.50”

and local amts to 1.10”;

driest south

Sat-Sun 45% cvg of up to 0.75”

and local amts to 1.50”;

driest SW

Sun-Aug 28 75% cvg of up to 0.75”

and local amts to 1.50”;

driest south

Aug 27-28 30% cvg of up to 0.65”

and locally more;

wettest north

Aug 29 15% cvg of up to 0.25”

and locally more

Aug 29-31 65% cvg of up to 0.75”

and local amts to 1.50”

Aug 30-Sep 1 60% cvg of up to 0.60”

and locally more

Sep 1-3 10-25% daily cvg of

up to 0.30” and locally

more each day

Sep 2-3 10-25% daily cvg of

up to 0.30” and locally

more each day

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy 90-100% cvg of up to 0.75”

and local amts to 1.75”

Tdy-Tue 80% cvg of up to 0.75”

and local amts to 2.0”;

driest SE

Tue-Sun Up to 20% daily cvg of

up to 0.25” and locally

more each day; some

days may be dry

Wed-Thu 5-20% daily cvg of up

to 0.30” and locally

more each day

Fri-Sun 15-35% daily cvg of

up to 0.70” and locally

more each day; west

and south wettest

Aug 27-30 10-25% daily cvg of 10-25% daily cvg of

up to 0.30” and locally up to 0.35” and locally

more each day more each day

Aug 31-Sep 3 5-20% daily cvg of up 10-25% daily cvg of

to 0.30” and locally up to 0.35” and locally

more each day more each day

Source: World Weather and FI

Bloomberg weekly agenda

- Argentina, Egypt on holiday

- Intertek, AmSpec release respective data on Malaysia’s Aug. 1-20 palm oil exports, 11pm ET Sunday (11am Kuala Lumpur Monday)

- SGS data for same period, 3am ET Monday (3pm Kuala Lumpur Monday)

- EU weekly grain, oilseed import and export data, 10am ET (3pm London)

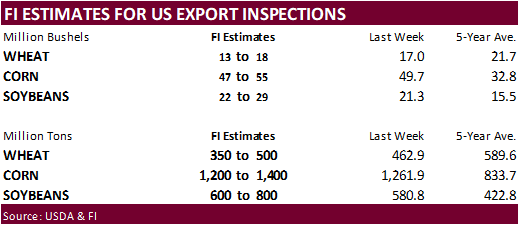

- USDA weekly corn, soybean, wheat export inspections, 11am

- USDA milk production data for July, 3pm

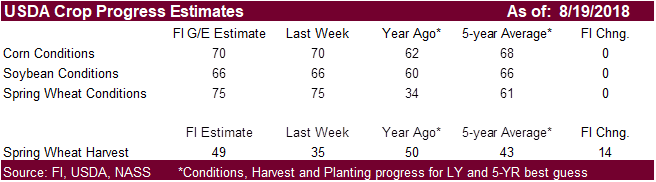

- USDA weekly crop progress report, 4pm

- ProFarmer U.S. soy/corn crop tour, Day 1

- Ivory Coast weekly cocoa arrivals

- Most active period of Atlantic hurricane season begins, and peaks around Sept. 10

TUESDAY, AUG. 21:

- Egypt on Eid Al-Adha holiday

- Brazilian agency Conab’s 2nd estimate for 2018-19 sugarcane crop

- New Zealand dairy auction on Global Dairy Trade online market starts ~7am ET (~noon London, ~11pm Wellington)

- ProFarmer U.S. crop tour, Day 2

WEDNESDAY, AUG. 22:

- India, Singapore, Malaysia, Indonesia, Egypt on holiday

- Agritel presser on French wheat harvest 2018 season, 3am ET (9am Paris)

- DBV outlook on German crop outlook

- ProFarmer U.S. crop tour, Day 3

- EIA U.S. weekly ethanol inventories, output, 10:30am

- USDA cold-storage report for July, 3pm

THURSDAY, AUG. 23:

- China’s General Administration of Customs releases July agricultural commodity trade data (final), including imports of palm oil, wheat, cotton and corn, 2:30am ET (2:30pm Beijing)

- Intl Grains Council’s monthly market forecasts, 8:30am ET (1:30pm London)

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- USDA red meat production for July, 3pm

- Brazilian research foundation Fundecitrus releases report on greening incidence on oranges; Brazil is top producer, exporter

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

- ProFarmer U.S. crop tour, Day 4

- U.S. is set to impose 25% tariffs on additional $16b in Chinese imports; China said it will retaliate

- EARNINGS: Sanderson Farms, Hormel Foods

FRIDAY, AUG. 24:

- ProFarmer issues final yield estimates after crop tour, 2pm

- USDA cattle-on-feed report for July, 3pm

- Unica bi-weekly report on Brazil Center-South sugar output

- Salvadoran coffee council’s El Salvador July export data

- Nicaragua’s coffee council releases July export data

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- No changes

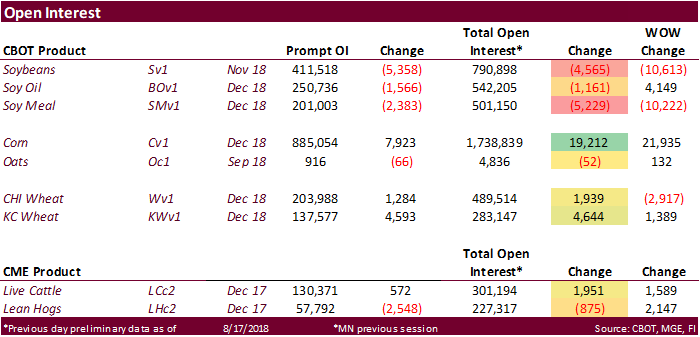

· Traditional funds for the futures and options position only bought about 24,400 contracts more corn than previous thought and bought more than expected soybeans and Chicago wheat than expected, for the week ending 8/17.

· The managed money fund position in soybeans oil was a record short 97,124 contracts for futures only, and record net short 96,687 contracts for futures and options combined.

· For traditional funds futures only, the net short position in soybean oil was reported near record.

· Funds backed off their net long position in wheat.

· Money managers bought meal and sold soybeans and oil. They added long positions to KC wheat.

· Index funds were quiet last week, but they did unwind 5,100 Chicago wheat contracts.

· US stocks are higher, USD higher, WTI crude higher, and gold higher, at the time this was written.

Corn.

- Corn is lower following wheat and soybean/corn spreading.

- News is light and US weather is mostly favorable

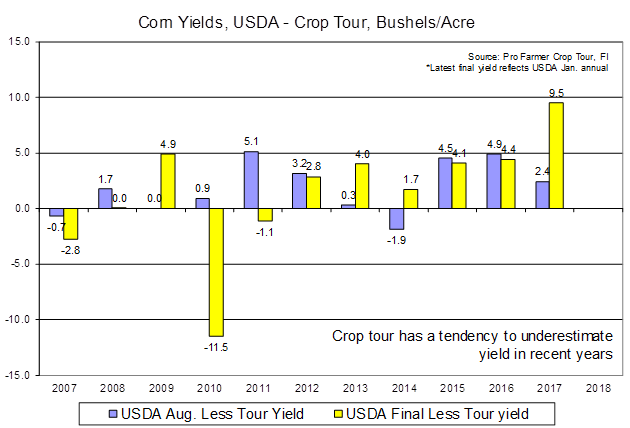

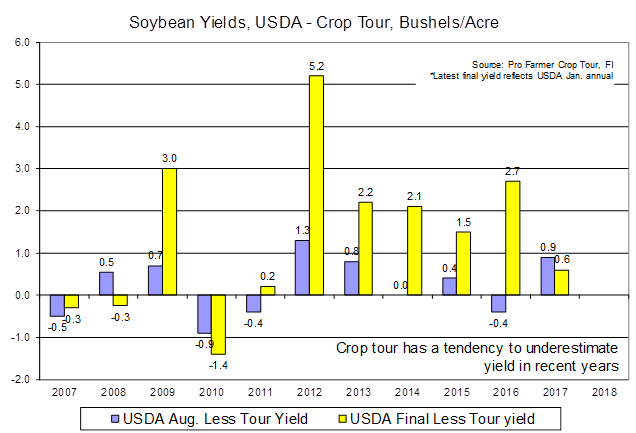

- Today is the start of the annual US ProFarmer Crop Tour. Results will be out Friday, August 24.

- Baltic Dry Index increased 0.2 percent to 1727 points.

· China reported its third outbreak of African Swine Fever over the weekend with 615 hogs infected in Jiangsu’s Lianyungang. As of early Monday, 88 were confirmed dead.

- Hot and dry weather in Ukraine was thought to lower late planted corn production prospects this season, and impact 2019 winter plantings. Corn harvesting is about to go into full swing. After rains fell mid-season, the AgMin increased its corn production estimate to record 28.5 million tons from 27.3 million tons previously.

· Agriculture and Agri-Food Canada (AAFC) raised the Canada barley crop to 8.5 million tons for 2018 from 8.0 million tons previously. USDA is at 8.8 million tons, up from 7.9MMT million in 2017.

- Argentina’s corn harvest is 94 percent complete, according to the BA Grains Exchange, versus 89 percent last week and 85 percent average. Production was left unchanged at 31 million tons.

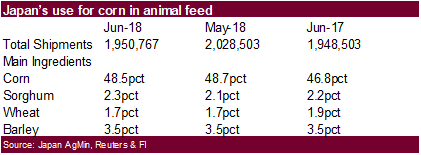

- Japan’s use of corn in animal feed declined in June from May but was slightly above a year ago.

· China sold about 63.7 million tons of corn out of reserves this season. Another 4 million tons will be offered late this week.

Soybean complex.

· Soybeans are higher but a downturn in soybean meal pulled back gains. Follow through buying was noted after the Friday WSJ report that China wanted to resolve trade disputes by the time President Trump and Chinese leader Xi Jinping meet in November. The talks scheduled next week (Aug 22-23) may include some insight on how both countries will approach resolving the dispute.

· Soybean oil is higher on unwinding of meal/oil spreads.

- Argentina is closed today for holiday.

· Agriculture and Agri-Food Canada (AAFC) estimated the Canada canola crop at 20.335 million tons for 2018, up from 19.150 million tons projected in July. Oil World is using 21.7MMT. USDA is at 21.1MMT versus 21.5 million in 2017.

- A Cofco official recently told a Chinese newspaper that they recently made inquiries on canola, cottonseed and sunflower seed meals with countries including India, Canada, and Ukraine to fill the US soybean gap. It was noted in the article that the price drop in pork has lowered soybean meal demand since May by 400,000 tons per month. China’s reserves of imported soybeans are ample now.

- Xinhua News noted China bought over 36 million tons of soybeans from South America during the May-August period and more buying will continue through November.

- A third US cargo of US soybeans sailed to China post 25 percent additional import tariff left east China’s port of Nantong near Shanghai but unloaded less than 50 percent of its load. Reuters said its headed for Australia.

· China cash margins were last 89 cents/bu on our analysis, compared to 97 cents late last week, and 96 cents last year.

· China’s growing problem with African Swine Fever is impacting domestic pork consumption and lowering the amount of available animal units, although by a fraction, but fundamentally scaring traders enough that it sent China soybean meal futures lower on Monday.

· China reported its third outbreak of African Swine Fever over the weekend with 615 hogs infected in Jiangsu’s Lianyungang. As of early Monday, 88 were confirmed dead.

· China’s soybean complex traded mixed. Soybeans were off 1.6%, soybean meal down 1.4%, while soybean oil was higher by 0.2% and palm increased 0.7%.

· Offshore values were suggesting a higher lead for US soybean meal by $1.90 and higher lead for soybean oil by 15 points.

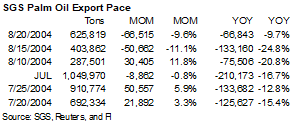

· Cargo surveyor SGS reported Aug 1-20 Malaysian palm exports at 625,819, down 66,515 tons or 10% from the same period a month ago and down 66,843 tons from the same period a year ago (10% decrease).

· AmSpec reported palm exports at 609,098 tons, down 10.6 percent from the previous period last month.

· October Malaysian palm was higher overnight by 17 ringgits and leading SBO 15 points higher. Cash was $3.75/ton higher.

· Rotterdam meal was lower and vegetable oils mixed.

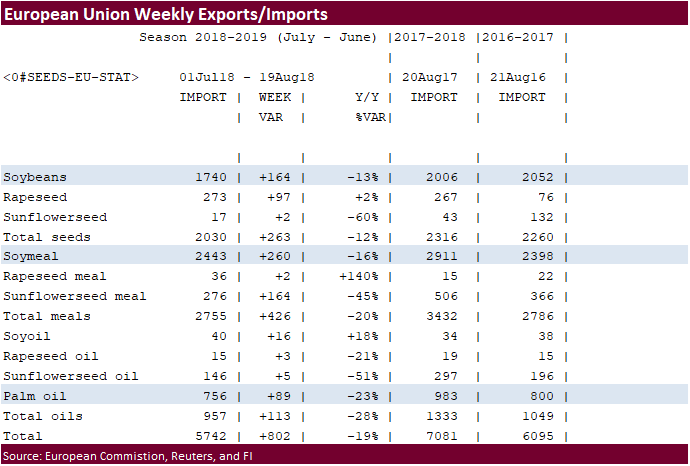

· EU granted 1.740 million tons of soybean imports so far this season starting July 1, down 13 percent from 2.006 million tons at this time last year. Traders were looking for a large increase in EU soybean imports this summer as China snapped up many of SA’s available supplies.

- Iran seeks 30,000 tons of sunflower oil on September 24.

· Wheat futures are lower on technical setbacks after rallying Friday on news Russia may consider capping wheat exports.

· Russia harvested 69.4 million tons of grain with an average yield of 3.12 tons per hectare from 48 percent of the harvesting area (AgMin). It had harvested 70.8 million tons with an average yield of 3.98 tons on the same date a year earlier.

· Russia plans to sell 2 million tons of grain from stocks during 2018-19. As of Aug. 17, Russia held 3.7 million tons of grain in stockpiles.

· Bulgaria harvested 5.3 million tons of wheat from 98.3 percent of the sown area by Aug. 20, below 5.7 million tons harvested a year earlier (AgMin).

· The Swedish Board of Agriculture estimated total cereal production 29 percent lower year-on-year at 4.2 million tons in 2018.

· Agriculture and Agri-Food Canada (AAFC) estimated the Canada wheat crop at 30.300 million tons for 2018, down from 31.1 million tons projected in July. USDA is at 32.5 million tons, up from 30.0 million in 2017.

· EU December wheat was 2.00 euros lower at 212.75 euros, at the time this was written.

· The European Union granted export licenses for 78,000 tons of soft wheat imports, bringing cumulative 2018-19 soft wheat export commitments to 1.340 million tons, well down from 2.343 million tons committed at this time last year.

Export Developments.

· China sold 4,055 tons of 2013 imported wheat at 2,350 yuan per ton ($341.87/ton), 0.24 percent of what was offered.

· Jordan seeks 120,000 tons of hard milling wheat on Aug 29 for Nov/Dec shipment.

· Jordan seeks 120,000 tons of feed barley on August 28.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on August 22 for arrival by January 31.

· China sold 28,948 tons of rice at 2,610 yuan per ton ($379.69/ton), 3.29 percent of what was offered.

· Thailand to sell 120k tons of raw sugar on Aug. 22.

· Egypt’s AgMin said they have enough sugar reserves for 7.5 months.

· Results awaited: Egypt’s ESIIC seeks 100,000 tons (150k previously) of raw sugar for shipment within the first half of September and two 50,000-ton shipments from September 15-Oct 15.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.