From: Terry Reilly

Sent: Wednesday, September 19, 2018 8:04:49 AM (UTC-06:00) Central Time (US & Canada)

Subject: FI Morning Grain Comments 09/19/18

PDF attached

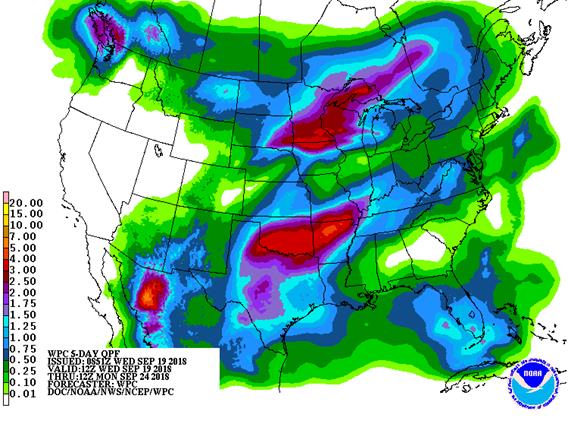

· The 6-10 day indicates a wetter outlook in the north central Midwest, and slightly drier in the northwestern Plains. Temps are cooler in the central Plains and western Midwest. The 11-15 day is slightly wetter in the northern Midwest, and drier in the southwestern Plains. Temps are cooler in the Plains and Midwest.

· Frost and freezes may eventually develop in the northern most Midwest and a part of the northern Plains in late September.

· HRW wheat country will see rain delaying plantings of winter wheat but the precipitation was welcome.

· Canada’s Prairies will be cool and wet this week, delaying harvesting efforts.

· Australia’s precipitation will remain limited this week.

· Russia’s Volga River Basin could see additional rain will fall this week.

· Europe will see limited rainfall through Thursday.

· Brazil will see good rain this week from Mato Grosso do Sul and Paraguay to southern Minas Gerais, Parana, Santa Catarina and Parana.

· Argentina will see a mixture of rain and sunshine.

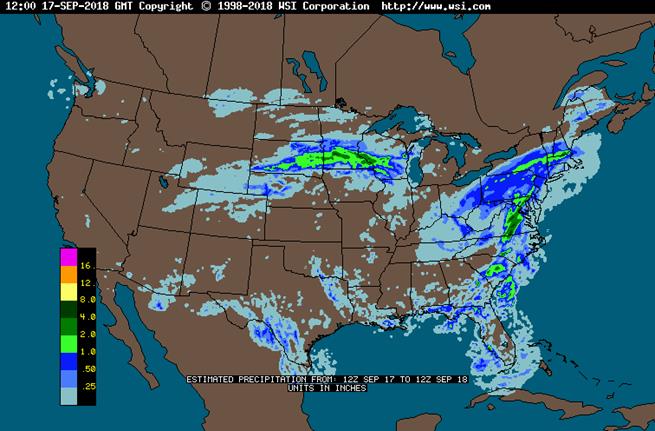

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Wed 25% cvg of up to 0.75”

and local amts to 1.35”;

wettest north

Tdy-Thu 80% cvg of 0.40-2.0”

and local amts to 3.50”

from east S.D. and NE

Neb. to central and

north Ia. and west Wisc.

with up to 0.65” and

local amts to 1.20”

elsewhere; far south

driest

Thu-Fri 70% cvg of up to 0.35”

and local amts to 0.80”

Fri-Sat 15% cvg of up to 0.75”

and local amts to 1.50”;

far south wettest

Sat-Sun 20% cvg of up to 0.50”

and local amts to 1.10”;

wettest south

Sun 20% cvg of up to 0.50”

and local amts to 1.10”;

NW and far SE wettest

Mon-Sep 25 85% cvg of up to 0.75” 85% cvg of up to 0.75”

and local amts to 1.75”; and local amts to 1.50”

far NW driest

Sep 26-27 Up to 20% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Sep 26-28 Up to 20% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Sep 28-29 60% cvg of up to 0.60”

and local amts to 1.25”

Sep 29-30 60% cvg of up to 0.40”

and local amts to 1.0”

Sep 30-Oct 2 65% cvg of up to 0.70”

and locally more

Oct 1-3 70% cvg of up to 0.70”

and locally more

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

Tdy-Thu Up to 20% daily cvg of

up to 0.30” and locally

more each day; some

days may be dry

Wed Mostly dry with a few

insignificant showers

Thu-Sun 5-20% daily cvg of up

to 0.30” and locally

more each day

Fri-Sat 50% cvg of up to 0.65”

and local amts to 1.30”;

wettest north

Sun-Sep 25 80% cvg of up to 0.75”

and local amts to 1.50”

Mon-Sep 26 80% cvg of up to 0.75”

and local amts to 1.75”

Sep 26-28 5-20% daily cvg of up

to 0.30” and locally

more each day

Sep 27-29 15-35% daily cvg of

up to 0.50” and locally

more each day

Sep 29-Oct 2 Up to 20% daily cvg of

up to 0.25” and locally

more each day

Sep 30-Oct 2 5-20% daily cvg of up

to 0.30” and locally

more each day

Source: World Weather and FI

WEDNESDAY, SEPT. 19:

- EIA U.S. weekly ethanol inventories, output, 10:30am

- USDA milk production data for August, 3pm

- Malaysian Palm Oil Council (MPOC) holds Intl Palm Oil Sustainability Conference in Kota Kinabalu, Malaysia, Sept. 19-20; Executives from FAO, Nestle, Olam, Sime Darby, MPOB expected to attend

- INTL FCStone holds agribusiness conference in Sao Paulo, with Finance Minister Eduardo Guardia and BRF CEO Pedro Parente due to speak

THURSDAY, SEPT. 20:

- Intertek and AmSpec release their respective data on Malaysia’s Sept. 1-20 palm oil exports, 11pm ET Wednesday (11am Kuala Lumpur Thursday)

- SGS data for same period, 3am ET Thursday (3pm Kuala Lumpur Thursday)

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- USDA red meat production for August, 3pm

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

- Intl Palm Oil Sustainability Conference in Kota Kinabalu, final day

FRIDAY, SEPT. 21:

- Ghana public holiday

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

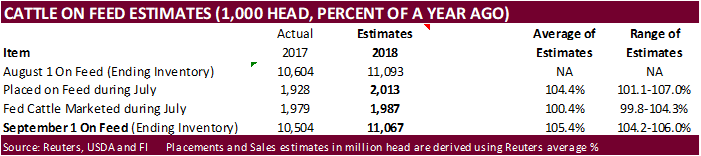

- USDA cattle-on-feed report for August, 3pm

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

Registrations

- Chicago wheat down 125 to 545 (various Cargill locations)

- Corn down 6 to 1426 (CBG Utica)

- Soybeans down 69 to 389, Cofco Chicago

US area estimates:

Informa reportedly put out the following US area in million acres:

· 2019 corn 93.0 vs. 89.10 in 2018 (USDA Sep 89.129)

· 2019 soybeans 82.3 vs. 88.97 in 2018 (USDA Sep 89.557)

· 2019 winter wheat 34.1 vs. 32.3 in 2018 (USDA Aug 32.7)

· 2019 all wheat 50.1 vs. 47.6 in 2018 (USDA Aug 47.8)

Statistics Canada Canadian crop production estimates based on satellite and agroclimatic data, not the farm survey.

· Canada 2018 all-wheat output seen +3.5 pct. to 31.02 mln tons vs 29.98 mln tons in 2017

· Canada 2018 durum wheat output seen +15.0 pct to 5.71 mln tons vs 4.96 mln tons in 2017

· Canada 2018 oats output seen -9.4 pct to 3.38 mln tons vs 3.73 mln tons in 2017

· Canada 2018 barley output seen +4.3 pct to 8.23 mln tons vs 7.89 mln tons in 2017

· Canada 2018 canola output seen -1.5 pct to 21.00 mln tons vs 21.33 mln tons in 2017

Macros.

· US stocks are lower, USD lower, WTI crude mixed, and gold higher, at the time this was written.

· US Housing Starts Aug: 1.282M (est 1.235M, prevR 1.174M)

– US House Starts Change MM Aug: 9.2% (prevR -0.3%)

· US Building Permits Aug: 1.229M (est 1.310M, prev 1.303M)

US Building Permits Change MM Aug: -5.7% (prev 0.9%)

Informa reportedly put out the following US area in million acres:

· 2019 corn 93.0 vs. 89.10 in 2018 (USDA Sep 89.129)

· 2019 soybeans 82.3 vs. 88.97 in 2018 (USDA Sep 89.557)

· 2019 winter wheat 34.1 vs. 32.3 in 2018 (USDA Aug 32.7)

· 2019 all wheat 50.1 vs. 47.6 in 2018 (USDA Aug 47.8)

Corn.

- Corn futures are higher following wheat and soybeans.

- On Tuesday prompt FOB offers were down 2 cents at 43 cents over Dec. CIF corn bids for September barges were bid 4 cents lower at 28 over the Dec.

- Baltic Dry Index was down 17 points or 1.3% to 1373.

· China’s sow herd fell in August by 4.8 percent from August 2017, according to the Ministry of Agriculture and Rural Affairs. Poor pig prices and outbreaks of African swine fever were noted. Sow herd declined by 1.1 percent from the prior month. China’s hog herd fell in August by 2.4 percent from a year earlier and by 0.3 percent from July.

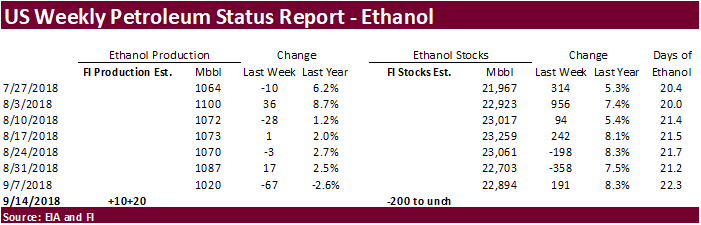

· A Bloomberg survey calls for US ethanol production to increased 10,000 barrels per day to 1.03 million from 1.020 million last week, and stocks to increase to 22.919 million from 22.894 million last week.

· South Korea’s KOCOPIA bought about 60,000 tons of optional origin corn, likely to be sourced from the United States, at $202.12 a ton c&f for arrival around Jan. 10, 2019.

· South Korea’s KFA bought about 63,000 tons of optional origin corn at $200.95 a ton c&f for arrival around Feb. 28, 2019.

· China will sell another 8 million tons of corn later this week.

· China sold about 80 million tons of corn out of reserves this season.

Soybean complex.

· Soybeans are seeing a light technical rebound this morning after trading near a 10-year low on Thursday. Look for US harvesting pressure, good SA weather and US/China trade conflict to limit gains.

· Soybean oil is lower after Malaysian palm fell out of bed.

· US Gulf soybeans weakened on Tuesday. Spot soybean export premiums fell 5 cents, at about 10 cents over futures. Soybean barges for Sep. were bid at a 10 under the CBOT November, 5 cents weaker than Monday.

· Argentina lawyers drafted two articles for the Budget Law 2019 that may grant power to the Executive arm of the government the right to raise export taxes on agriculture commodities up to 33 percent.

· Coceral lowered its estimate of EU rapeseed production to 19.4 million tons from 21.0 million in June.

· Malaysia November palm oil fell to a 2-month low. November settled 41MYR lower and leading soybean oil 11 points lower. Malaysian cash palm oil was down $8.75.

· Many 40 lot block trades occurred in 2019 months overnight.

· Rotterdam oils were lower and SA soybean meal when imported into Rotterdam mixed.

· Offshore values were suggesting a higher lead for US soybean meal by $2.00 and were flat for soybean oil.

· U of I: 2019 Crop Budgets Suggest Dismal Corn and Soybean Returns

- China sold about 2.38 MMT of soybeans out of reserves this season.

- Iran seeks 30,000 tons of sunflower oil on September 24.

Wheat

· US wheat is higher on follow through buying from an increase in global demand and Australian production woes.

· Coceral lowered its outlook for EU soft wheat production to 129.9 million tons from 138.8 million in June. Corn production was pegged at 58.9 million tons from 60.3 million previously and barley production at 57.4 million tons from 60.8 million.

· Traders noted Russia is in for cold and wet weather, threatening Russian spring wheat

· Kazakhstan collected 11.2 million tons of grain as of September 18, 2018 compared with 12.6 million tons harvested a year earlier, 59% of the total area under crop. Harvesting delays was noted. The AgMin has a 20-million-ton crop and exports at 9 million tons. In 2017 Kazakhstan harvested 21.9 million tons of grain in net weight.

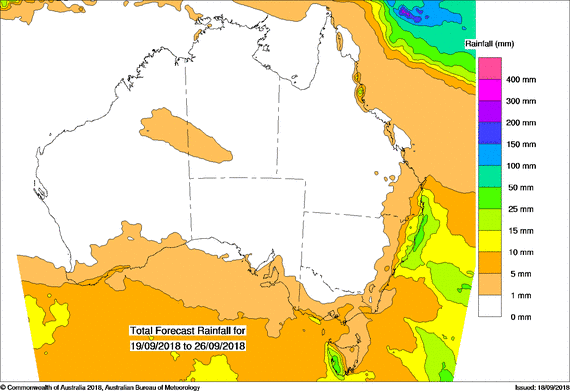

Australian 8-day precipitation forecast.

· Yesterday Egypt’s GASC bought 180,000 tons of wheat for shipment over Nov. 1-10 and another 295,000 tons for Nov. 11-20 shipment. One cargo was of Ukrainian origin and rest Russian.

· Turkey seeks a total of 252,000 tons of red milling wheat for October 2-22 loading. It closes on September 22. The depreciation of the lira sent importers seeking Turkish wheat flour, causing them to restrict exports. But countries like Iraq that heavily depend on flour from Turkey may have to import from other countries.

- Syria bought about 200,000 tons of Russian wheat at $224.50 per ton c&f for shipment between Oct. 15 and Dec. 15. Syria is planning to import around 1.5 million tons of mostly Russian wheat this year.

- Jordan passed on 120,000 tons of feed wheat, optional origin. 2 offers were presented.

· China sold 3,000 tons of imported 2013 wheat at auction from state reserves at an average price of 2,160 yuan ($315.31) per ton, 0.3 percent of total wheat available at the auction.

- Japan in a SBS import tender passed 120,000 tons of feed wheat and 200,000 tons of barley for arrival by late February.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on September 26 for arrival by late February.

· Japan seeks 149,586 tons of wheat on Thursday.

- Jordan seeks 120,000 tons of feed barley, optional origin, on September 26.

- Results awaited: Ethiopia seeks 200,000 tons of milling wheat for shipment two months after contract signing. Ethiopia got offers from 7 firms. Lowest offer was for 100,000 tons at $272.05/ton, c&f.

- Results awaited: Algeria seeks 75,000 tons of feed barley on Wednesday for November shipment.

- Iraq seeks 50,000 tons of wheat on September 23, with offers valid until September 27. Iraq needs wheat for four after Turkey restricted flour shipments.

- Morocco seeks 336,364 tons of US durum wheat on September 28 for arrival by December 31.

Rice/Other

· China sold 92,988 tons of 2013 rice at auction from state reserves at average price of 3,060 yuan ($446.12) per ton, 100 percent of total rice available for the auction.

· Iraq seeks 30,000 tons of rice from India on October 9 for LH October / FH November shipment.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.