From: Terry Reilly

Sent: Tuesday, July 24, 2018 8:12:47 AM (UTC-06:00) Central Time (US & Canada)

Subject: FI Morning Grain Comments 07/24/18

PDF attached

· The USDA crop progress report showed US corn conditions unchanged at 72 percent, one point above trade expectations.

· US soybean conditions increased unexpectedly by one point to 70 percent, 2 points above expectations.

· US spring wheat conditions decreased 1 point to 79 percent. The trade was looking for unchanged.

· US winter wheat harvesting progress increased 6 points to 80 percent, 3 points below average.

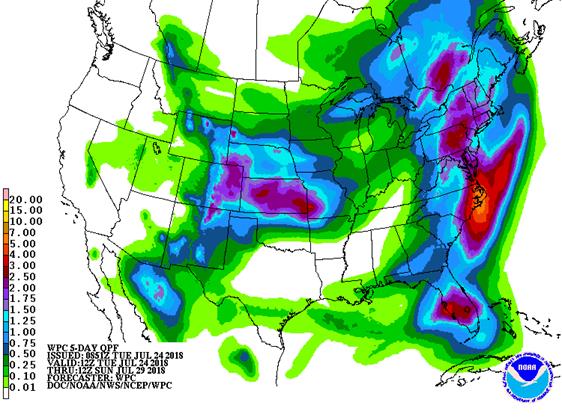

· The evening weather models increased rainfall bias western growing for week one and decreased rain for week 2.

· The morning forecast increased rainfall for the 6-10 day for the north central Midwest and 11-15 day is wetter for the southwestern Midwest and Delta.

· The ridge of high pressure is expected to stay centered over the southwestern United States throughout this week, and possible next week, creating a northwesterly flow aloft in the central U.S., Northern Plains and Corn Belt.

· It was hot across the US southwest over the weekend.

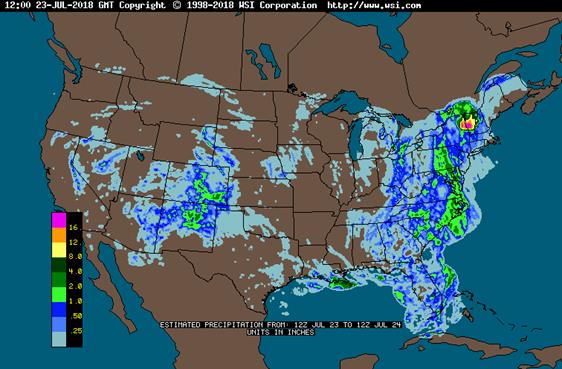

· Rainfall across the Midwest over the weekend was restricted to the ECB and western Dakotas. Dry or mostly dry weather occurred in much of Illinois, western Indiana, western Kentucky, western Tennessee and from much of Missouri through Iowa to western and southern Minnesota and the eastern Dakotas.

· The western Corn Belt will see net dry this week. The eastern Midwest will see rain.

· U.S. weather late this week through the weekend will be wettest from the central Plains into the lower Ohio River Valley and far northern Delta.

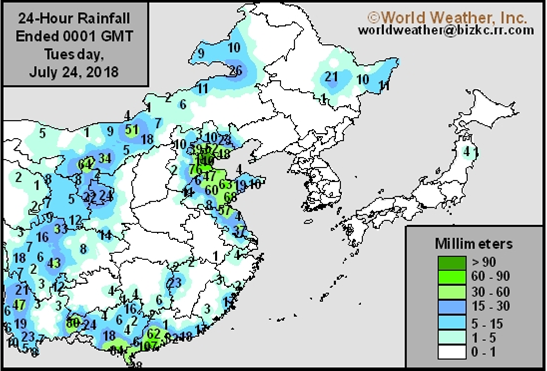

· China’s Hebei, Liaoning, Jilin and Heilongjiang may see too much rain this week, increasing flooding potential.

WORLD WEATHER AREAS OF GREATEST INTEREST THIS WEEK

· Western Luzon Island, Philippines continues to receive frequent heavy rain resulting in flooding

· Northern Vietnam will receive additional heavy rain this week as it is impacted by Tropical Storm Son-Tinh for the second time in a week

· Indonesia and Malaysia rainfall remains erratic and lighter than usual

· India’s Monsoon will take a short term break from mid-week this week into the end of next week

· Northern Europe dryness is not likely change much this workweek, but rain may increase during the weekend and next week

· Eastern Europe and the western CIS will see frequent rain maintaining concern over unharvested small grain quality

· Interior eastern and some central China areas will be drying out this week while Tropical Storm Ampil produces heavy rain from central Shandong and Hebei to parts of the Northeast Provinces

· East-central Australia drought will remain unchanged, despite a few showers

· U.S. Midwest weather will be mild to cool, but net drying is still expected in the central and western Corn Belt through mid-week and in central and northwestern areas late this week into early next week

· Southern U.S. Plains livestock and crops will get relief from heat this week, but not much rain expected

· Key Texas crop areas will stay dry this week, but some rain will fall in West Texas

· SW Canada Prairies, northwestern U.S. Plains and U.S. Pacific Northwest will stay drier and warmer biased through the next week

Source: World Weather Inc. and FI

Source: World Weather Inc. and FI

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

-Tue 15-35% daily cvg of

up to 0.65” and locally

more each day;

wettest east

Tue-Wed 30% cvg of up to 0.40”

and local amts to 0.90”;

wettest NW

Wed-Thu 35% cvg of up to 0.20”

and locally more

Thu 15% cvg of up to 0.10”

and locally more;

wettest north

Fri 15% cvg of up to 0.30”

and locally more

Fri-Sun 60% cvg of up to 0.75”

and local amts to 1.50”

with a few 1.50-2.50”

bands in the south;

driest north

Sat-Jul 30 75% cvg of up to 0.75”

and local amts to 2.0”

Jul 30-31 5-20% daily cvg of up

to 0.20” and locally

more each day

Jul 31-Aug 1 5-20% daily cvg of up

to 0.20” and locally

more each day

Aug 1-3 60% cvg of up to 0.60”

and local amts to 1.20”

Aug 2-4 60% cvg of up to 0.60”

and local amts to 1.25”

Aug 4-6 55% cvg of up to 0.50”

and locally more

Aug 5-7 60% cvg of up to 0.60”

and locally more

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy-Fri Up to 15% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Tdy-Tue 50-75% daily cvg of

up to 0.75” and local

amts over 1.50” each

day; wettest NE;

driest west

Wed-Fri 65% cvg of up to 0.75”

and local amts to 1.50”;

driest west

Sat-Jul 30 80% cvg of up to 0.75”

and local amts over 2.0”;

far south driest

Sat 25% cvg of up to 0.40”

and locally more;

wettest NE

Sun-Jul 31 80% cvg of up to 0.75”

and local amts over 2.0”

Jul 31 30% cvg of up to 0.50”

and locally more;

wettest south

Aug 1-3 10-25% daily cvg of 20-40% daily cvg of

up to 0.35” and locally up to 0.70” and locally

more each day more each day

Aug 4-6 15-35% daily cvg of 30-50% daily cvg of

up to 0.50” and locally up to 0.75” and locally

more each day more each day

Source: World Weather Inc. and FI

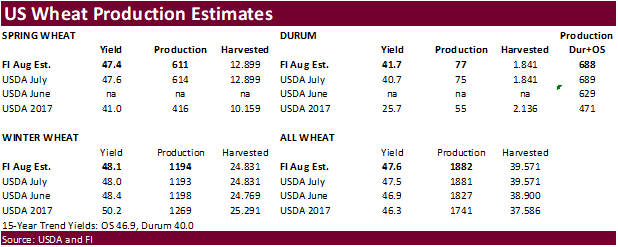

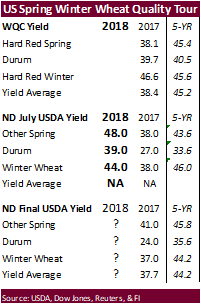

- Wheat Quality Council’s U.S. spring wheat crop tour begins in North Dakota, with final data expected Thursday

- Grain World crop tour in Canada hosted by FarmLink begins in Manitoba, Saskatchewan and Alberta, with final data for spring wheat, canola, durum and pulses expected Thursday

- Allendale holds webinar on weather outlook, 3pm ET (2pm CST)

- Datagro’s Global Agribusiness Forum in Sao Paulo, final day

WEDNESDAY, JULY 25:

- Costa Rica public holiday; Pakistan holds general election

- Cargo surveyors AmSpec, Intertek to release data on Malaysia’s July 1-25 palm oil exports, 11pm ET Tuesday (11am Kuala Lumpur Wednesday); SGS data for same period, 3am ET Wednesday (3pm local time Wednesday)

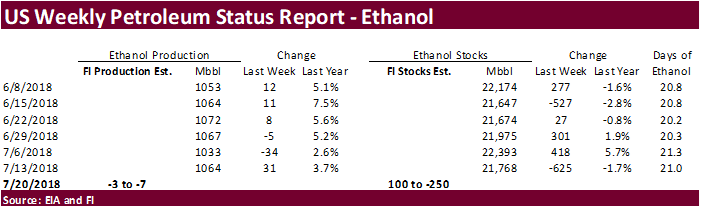

- EIA U.S. weekly ethanol inventories, output, 10:30am

- Allendale holds webinar on grains and oilseeds, 3pm ET (2pm CST)

- U.S. poultry slaughter June, 3pm

- Wheat Quality Council’s U.S. spring wheat crop tour, 2nd day

- Grain World crop tour in Canada, 2nd day

- EARNINGS: Coca-Cola

THURSDAY, JULY 26:

- Intl Grains Council monthly grains report, 8:30am ET (1:30pm London)

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- Allendale holds webinar on livestock outlook, 3pm ET (2pm CST)

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Wheat Quality Council’s U.S. spring wheat crop tour, 3rd day

- Grain World crop tour in Canada, final day

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

- World Trade Organization holds a General Council meeting that will last through July 27 to cover issues related to the U.S.-China trade conflict

- EARNINGS: Nestle SA, Anheuser-Busch Inbev, Diageo Plc

FRIDAY, JULY 27:

- Thailand, Peru public holidays

- G20 Agriculture ministers meet in Buenos Aires

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- FranceAgriMer weekly updates on French crop conditions

Source: Bloomberg and FI

· Soybeans down 599 to 402. (CIRM – Chicago)

· US stocks are higher, USD lower, WTI crude lower (turned lower around 8 am CT), and gold higher, at the time this was written.

· Philadelphia Fed Non-Manufacturing Regional Business Activity Index 44.3 In July VS 39.1 In June

· Philadelphia Fed Non-Manufacturing Firm-Level Business Activity Index 35.5 In July VS 40.7 In June

· Philadelphia Fed Non-Manufacturing New Orders Index 31.5 In July VS 35.5 In June

· Philadelphia Fed Non-Manufacturing Full-Time Employment Index 29.5 In July VS 19.9 In June

· Philadelphia Fed Wage And Benefit Cost Index 47.5 In July VS 51.1 In June

Corn.

- Corn is lower and trading higher over the past six sessions. US weather is a touch wetter for the WCB for the first week of the forecast and production prospects improved for the EU and Russia, according to two recent reports. MARS increased its EU corn yield estimate on Monday.

· UAC estimated the 2018 Russian corn crop at 11.2 million tons, up from 10.1 million previously, and compares to 10.8 last year. Exports are seen at 4.6MMT tons vs 3.7 previously. Some of the increase in exports could go to China, in our opinion.

- Baltic Dry Index was 56 points higher to 1,771, or 3.3%.

· US producer selling is slow.

· Flooding across China prompted the government to notify local agencies to ensure current supplies are protected and report prices on a daily basis.

- We picked up that Canada has been selling corn to the EU for OND and April/May shipment.

- EU animal unit producers are expected to use a little more corn this season due to rising feed wheat prices.

- The U.S. Department of Agriculture’s monthly cold storage report showed total pork inventories for June at 560.0 million pounds, down nearly 64 million from May – the second largest-ever withdrawal for the month (Reuters).

· The USDA crop progress report showed US corn conditions unchanged at 72 percent, one point above trade expectations.

· Conditions in CO, MI, NC, and OH declined from the previous week.

· 81 percent of the corn crop is silking.

· Our corn crop year weighted index increased 0.2% to 83.4, 3.1 percent above year ago and 1.0% above a 5-year average.

· We increased our US corn yield to 179.0 bushels per acre from 178.5 last week, which increased US corn production by 41 million bushels to 14.625 billion bushels, 21 million above last year and 395 million above USDA’s July estimate of 14.230 billion.

· Brazil will soon raise import quotas for US pork.

· China sold about 55.6 million tons of corn out of reserves this season.

Soybean complex.

· The soybean complex is lower on lack of bullish news and a slight improvement to US weather. US crop conditions increased on a national basis per USDA’s week update.

· President Trump plans to visit Dubuque, IA on Thursday. We may learn more if more agriculture groups are turning up the pressure to resolve the trade dispute.

· A Bloomberg article noted some Chinese crushers in the north suspended crushing due to high soybean meal inventories.

· China September soybean futures decreased 6 yuan per ton or 0.2%, September meal was down 18 or 0.6%, China soybean oil down 24 (0.4%) and China September palm down 26 (0.6%).

· September China cash crush margins were last running at 41 cents/bu, down from 45 previous session, and compares to 46 cents last week and 71 cents a year ago.

· Rotterdam vegetable oils were unchanged to lower and SA soybean meal mixed, as of early morning CT time.

· October Malaysian palm was 17 lower at MYR2152, and cash down $2.50 at $562.50/ton.

· Offshore values were leading soybean oil 4 points higher and meal $2.10/short ton lower.

· US soybean conditions increased unexpectedly by one point to 70 percent, 2 points above expectations.

· Conditions declined for MI and OH, and increased for AR, IL, LA, MO, NE, ND, and SD.

· On a weighted basis our US soybean index increased 0.5% to 82.8, 3.5 percent above last year and 1.3 percent above a 5-year average.

· We increased our soybean yield by 0.5/bu per acre to 49.2 bushels. Our production estimate is 4.371 billion bushels, 27 million above the previous week and 61 million above USDA’s 4.310 billion projection.

· Brazil’s Abiove increased its Brazil soybean production to 118.7 million tons for 2017-18 from 118.4 million in May. Soybean exports for this season were seen at 73.5 million tons, up from 72.1 million tons in May. Soybean crushing was seen at 43.6 million tons versus 43.6 million previously.

· Consultancy Corteva Agriscience estimated the soybean area in 2018-19 could increase 3 to 5 percent. That translates up to 37 million hectares (91.4 million acres), according to Reuters, using the current 35.15 million for 2017-18.

- China sold 2,377 tons of rapeseed oil out of auction at an average price of 6,000 yuan per ton ($883.30/ton), 4 percent of the total offered.

- South Korea seeks 1,500 tons of non-GMO soybeans on July 25 for September-December delivery.

- Iran seeks 30,000 tons of sunflower oil on September 24.

- Iran seeks 30,000 tons of soybean oil on August 1.

· China sold 972,370 tons of soybeans out of reserves so far, this season.

· US wheat futures are taking a breather after rallying late last week. The lower close in nearby Chicago yesterday could be triggering some additional profit taking.

· December Paris wheat futures was last 2.00 euros lower at 192.75 euros. The contract was recently at a three-year high.

· UAC estimated the 2018 Ukraine wheat crop at 24.8 million tons, down from 25.5 million previously, and compares to 26.1 last year. Exports are seen at 15.5MMT tons vs 16.0 previously and compare to 17.2 last year.

· France is gearing up to ship 93,750 tons of wheat to Algeria and 74,600 tons of barley to China.

· US spring wheat conditions decreased 1 point to 79 percent, highest level for this time of year since 2010. The trade was looking for unchanged.

· Our spring wheat weighted rating did not change much from the previous week. A drop in the MT ratings was partially offset by an increase in ND. There was no change to our spring and durum wheat production estimates from the previous week.

· US winter wheat harvesting progress increased 6 points to 80 percent, 3 points below average.

- The Wheat Quality Council’s U.S. spring wheat crop begins today in North Dakota. Results are due out Thursday.

Export Developments.

· Egypt is in for wheat for September 1-10 shipment and the lowest offer is $217.95/ton for 60k Russian origin. Russia, Romania and Ukraine wheat were offered this week.

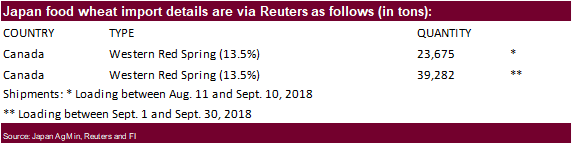

· Japan bought 62,957 tons of food wheat, all from Canada. Original details of tender as follows.

· Jordan passed on 120,000 tons of barley for Sep-Nov shipment.

· Jordan seeks 120,000 tons of wheat on July 26.

- China sold 28,742 tons of 2013 wheat out of auction at an average price of 2223 yuan per tons ($326.24/ton), 2 percent of what was offered.

- Bangladesh seeks 50,000 tons of optional origin milling wheat on July 25 for shipment within 40 days of contract signing.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on July 25 for arrival by December 28.

· Iraq seeks 50,000 tons of US, Canadian, and/or Australian wheat on July 29, valid until August 2.

- Results awaited: Bahrain Flour Mills seeks 17,000 tons of semi-hard wheat and 8,000 tons of hard wheat, on July 24, valid until July 25, for shipment in late Aug/early Sept. Origins include Australia, Baltics, & Canada.

Rice/Other

- China sold 76,086 tons of rice out of auction at an average price of 2375 yuan per tons, 4 percent of what was offered.

- Results awaited: Thailand seeks to sell 120,000 tons of raw sugar on July 18.

· Results awaited: Mauritius seeks 6,000 tons of white rice for Sep 1-Nov 30 shipment.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.